The Future of Private Equity: AI, India & Exit Momentum Reshape Global Investment in 2025

The global private equity landscape in 2025 is a story of contrasts. On positive side we se record-breaking megadeals alongside cautious, selective deployment; surging interest in AI infrastructure. Against those, a backdrop of geopolitical uncertainty; and glimmers of hope in exit markets while fundraising hits decade lows.

According to KPMG’s comprehensive Pulse of Private Equity Q3’25 report, the industry is navigating a complex transition. Technological disruption and a reconfiguration of global capital flows are the key drivers.

This deep dive unpacks the key themes from the report offering actionable insights for GPs, LPs, and portfolio companies.

Global Snapshot: Megadeals Buoy Value Amid Cautious Volume

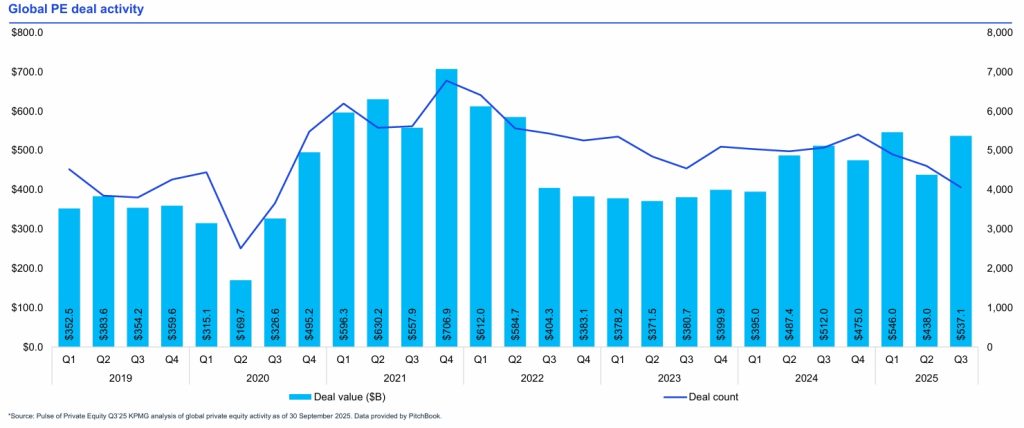

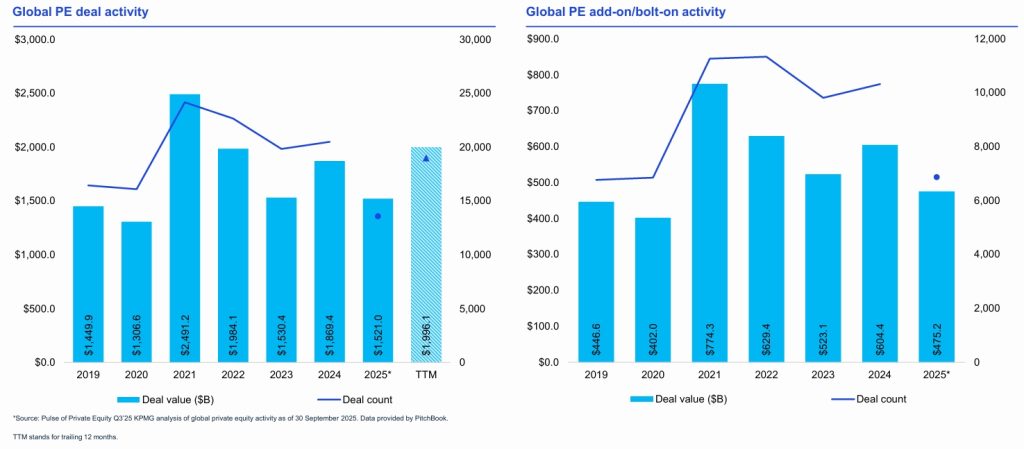

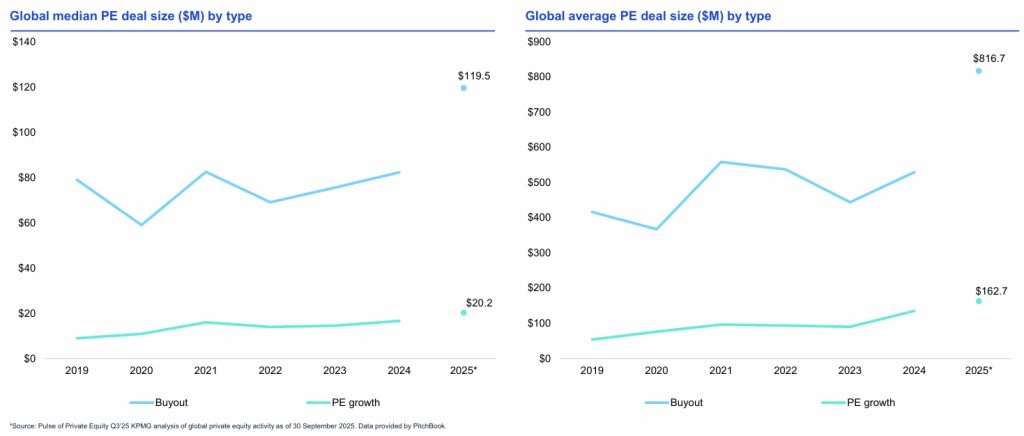

The headline numbers reveal a resilient market. Global PE investment reached $1.5 trillion in the first three quarters of 2025, with Q3 alone contributing $537 billion. This strength, however, is heavily concentrated. The quarter saw just 4,062 deals—a significant drop from 5,070 in Q3 2024—highlighting a market focused on quality over quantity.

The “Megadeal Effect” was unmistakable. A handful of massive public-to-private transactions in the US, including Electronic Arts ($56.4B), Air Lease ($28.2B), and Dayforce ($12.4B), single-handedly buoyed regional and global totals.

This trend underscores a critical insight: there remains a massive reservoir of dry powder chasing high-conviction, top-tier assets, even as broader market uncertainty keeps mid-market volume suppressed.

Regional Breakdown:

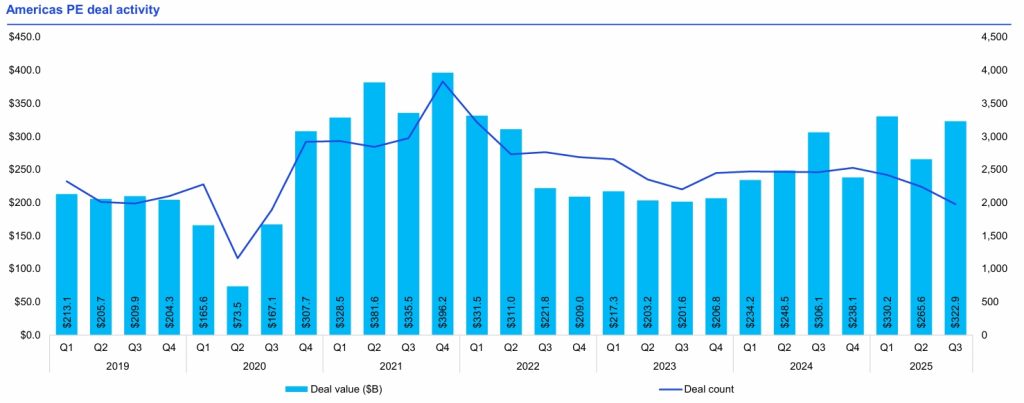

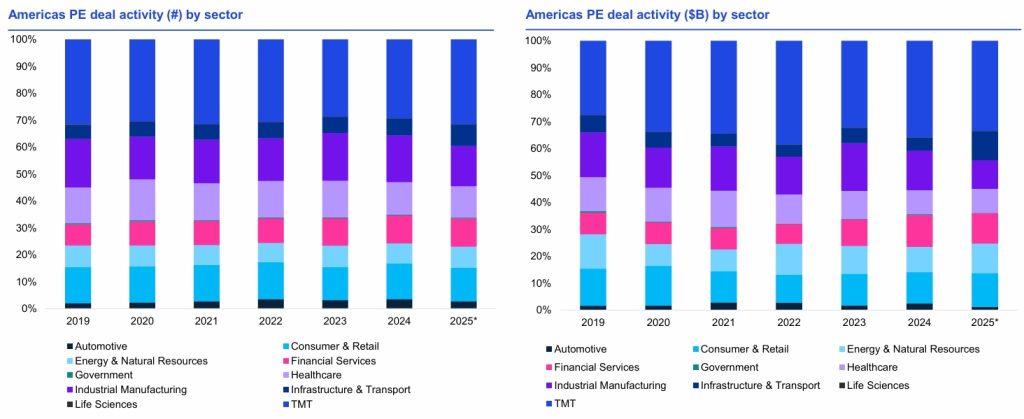

- Americas: Dominated the quarter with $322.9B (60% of global total), overwhelmingly led by the US ($300.2B).

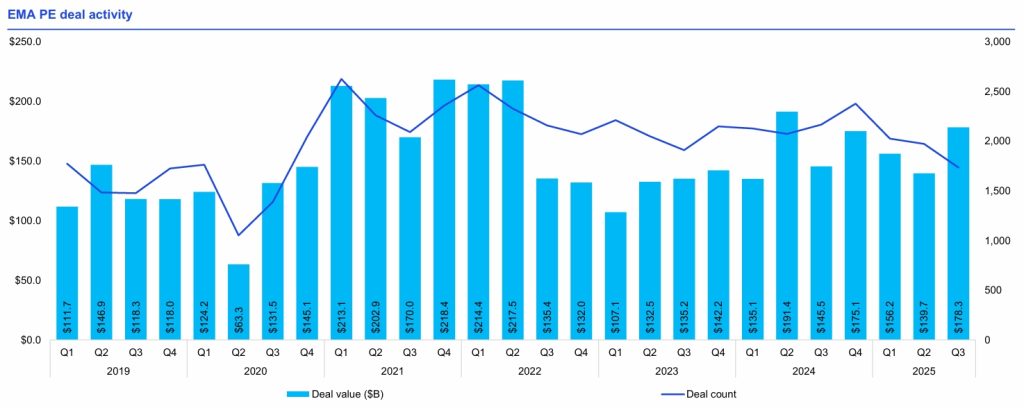

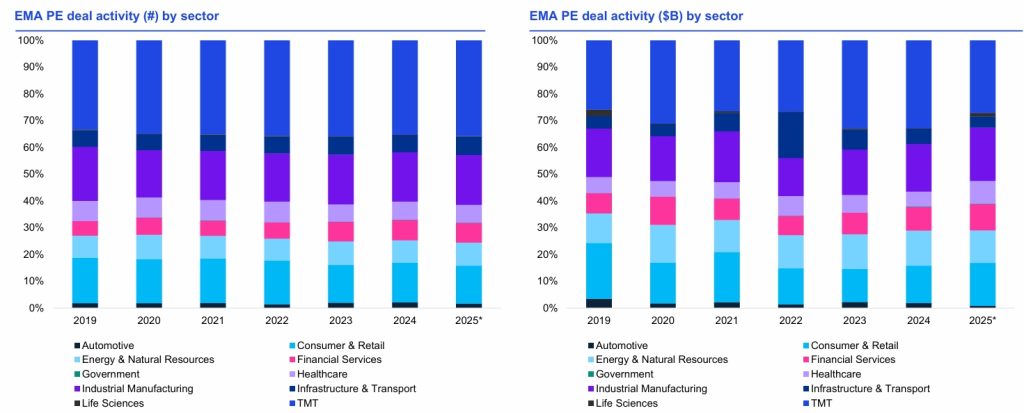

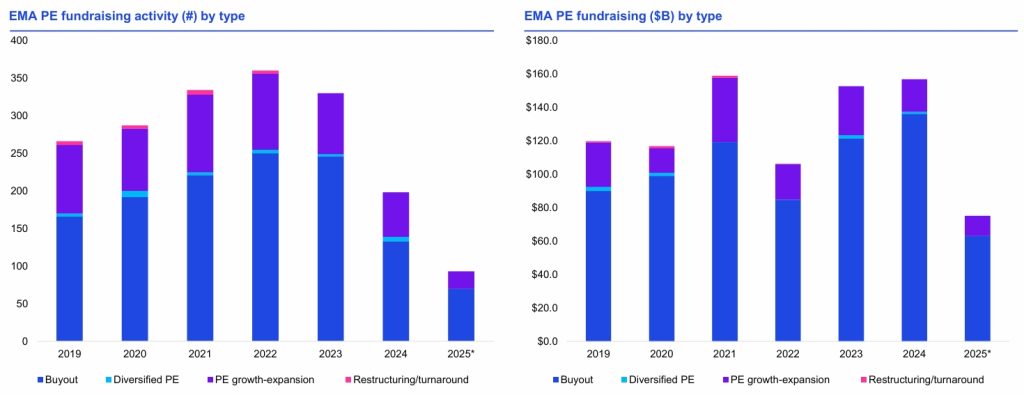

- EMA (Europe, Middle East, Africa): A distant second at $178.3B, with notable large deals in the UK and Germany.

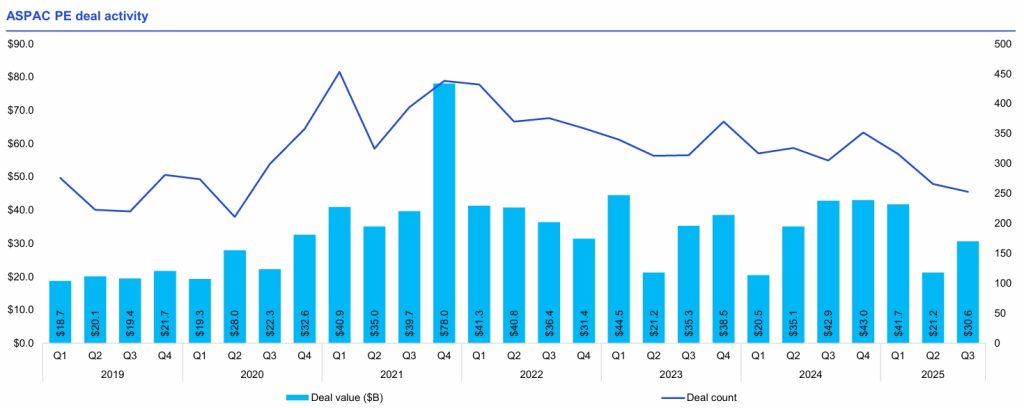

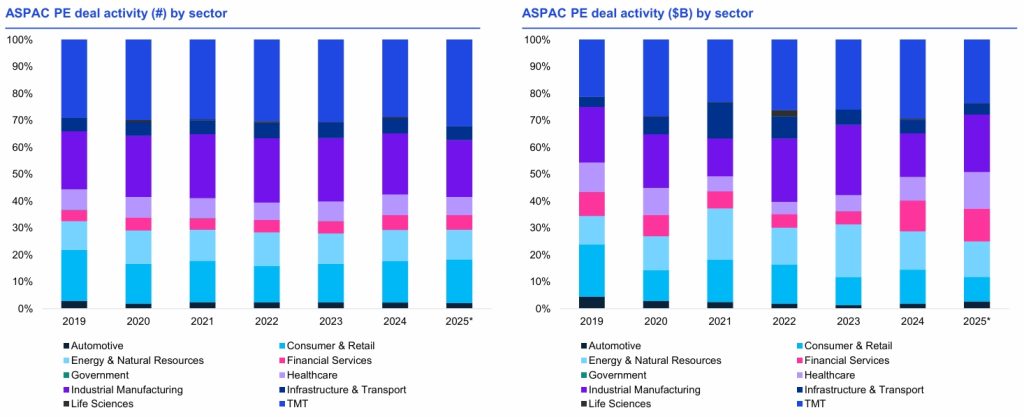

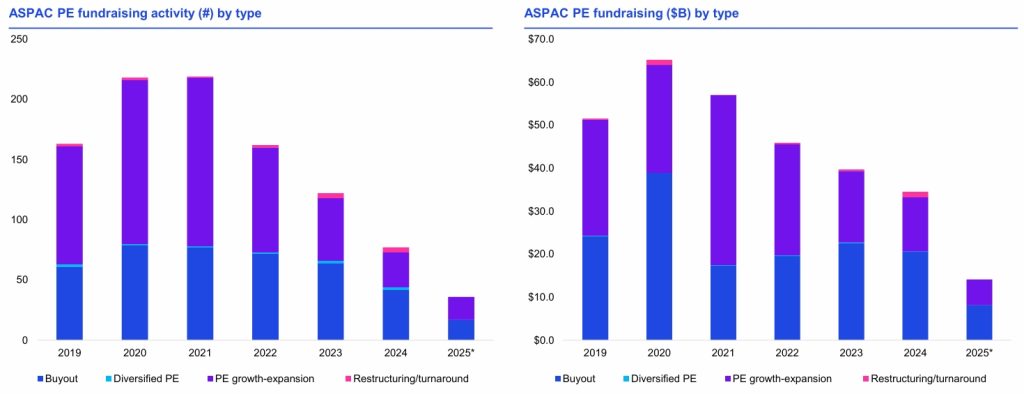

- ASPAC (Asia Pacific): Remained soft at $30.6B, grappling with persistent geopolitical and trade tensions, particularly affecting China.

Top 5 Trends Redefining Private Equity in 2025

1. The AI Infrastructure Gold Rush

If one theme dominates the sectoral conversation, it’s artificial intelligence. PE investment in Infrastructure & Transport hit a three-year high of $126.3B by Q3’25, already surpassing full-year 2023 and 2024 totals. This isn’t just about broadband or roads; it’s a direct bet on the AI ecosystem.

“The rapid growth in investment has largely been powered by AI; PE investors have rapidly increased their focus on infrastructure plays in the AI space, in addition to in the energy sector to power future AI developments,”

The play is twofold:

- Direct AI Infrastructure: Data centers, fiber networks, and specialized computing facilities.

- Enabling Energy Infrastructure: The massive power demand required to run AI models is driving parallel investments in energy generation and grid stability.

This trend is cross-regional and is poised to command an increasing share of capital allocation for years to come.

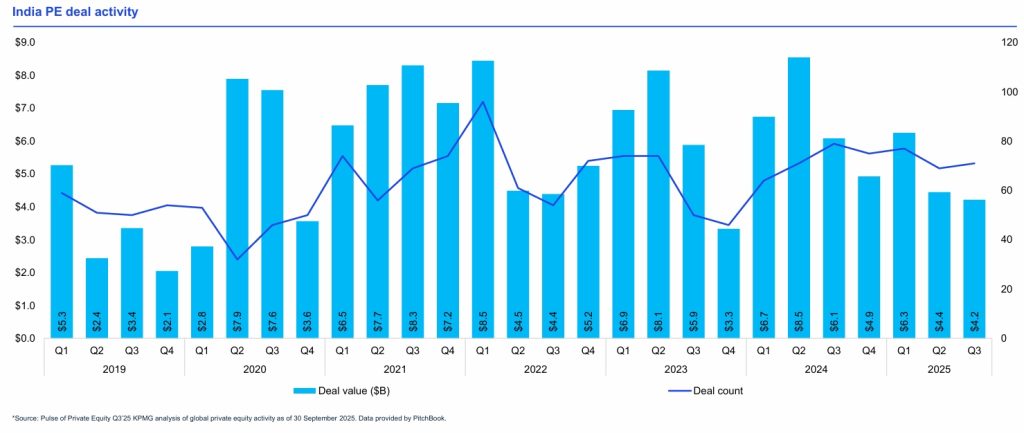

2. India: The Maturing Giant Amid Short-Term Softness

Despite lower investment in India but KPMG spotlight on its potential. While $14.9B investment by Q3 in India is potentially the lowest since 2019—the long-term thesis remains powerfully intact.

Why the optimism?

- Strong Macro Fundamentals: The world’s fastest-growing major economy, favorable demographics, and rising domestic consumption.

- Evolving GP Role: Global PE investors are acting as “business builders,” not just financial engineers. They are setting up local offices, taking majority stakes, and actively driving operational value through consolidation, platform building, and synergies within global portfolios.

- Growing Fund Sizes: The ecosystem is maturing. India-focused funds now routinely exceeding $1 billion, signaling LP confidence and larger, more sophisticated deal potential.

- Robust IPO Market: India’s strong public markets offer a viable and attractive exit path, yielding strong multiples compared to other jurisdictions.

The dip is attributed primarily to US tariff policy uncertainties, which have made scenario modeling difficult. The expectation is for a swift rebound as clarity emerges. Potentially it leads to increased competition and valuation pressure for top-quality assets.

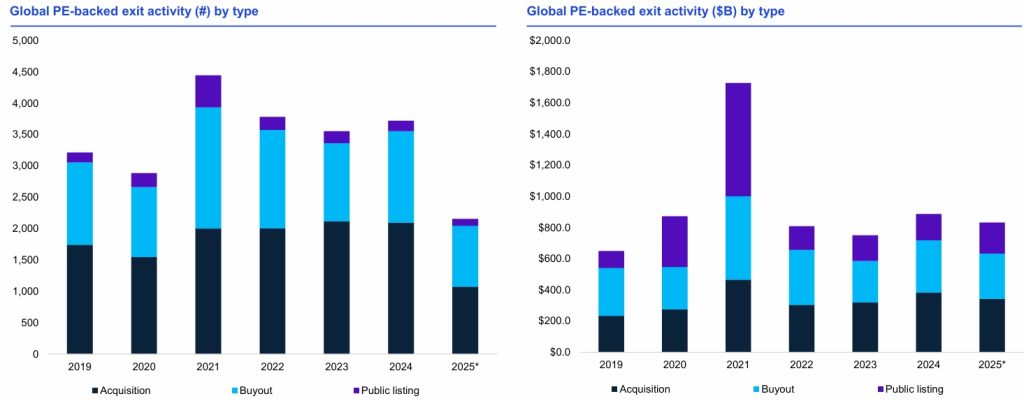

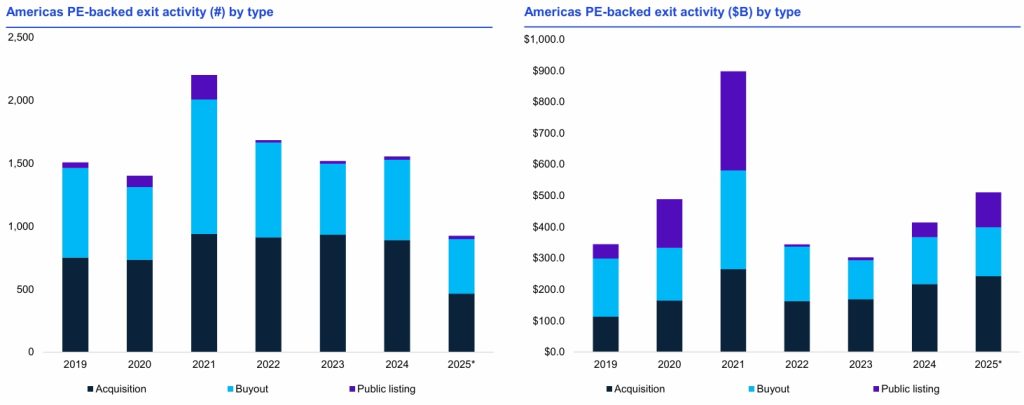

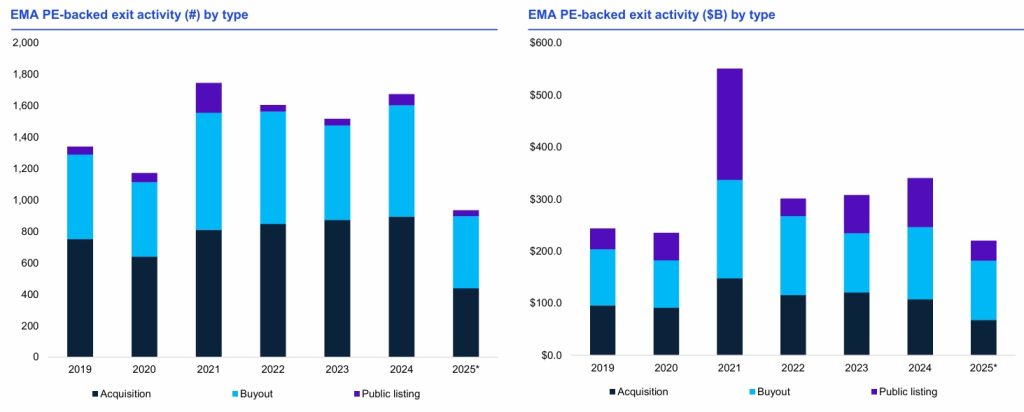

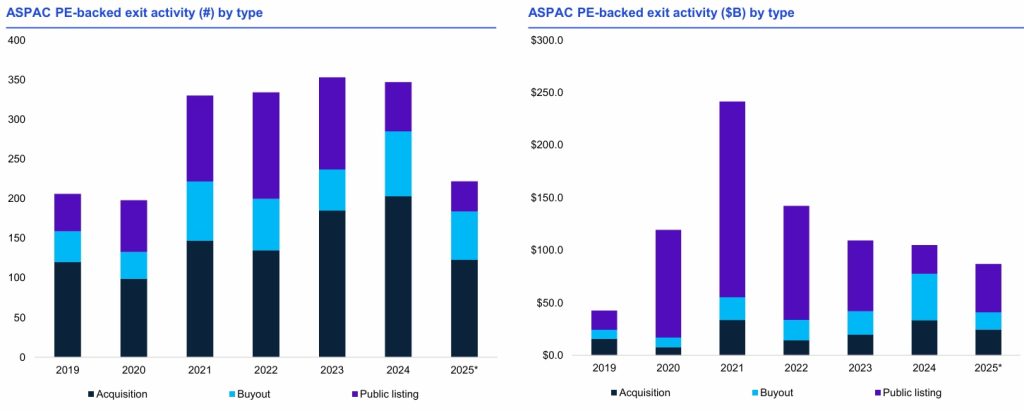

3. The Elusive Exit: Green Shoots Amid a Logjam

The exit overhang remains the industry’s most pressing challenge. While global exit value reached $832B by Q3—on pace for the second-best year since 2021—the volume of exits is at a decade-low of just 2,155. This indicates capital remains “stuck” in the system.

Signs of hope are emerging:

- IPO Markets Reopening: Particularly in the US and Asia, public listings are providing a crucial exit valve. US IPO exit value in Q3 ($111.7B) was already more than double the full-year 2024 total.

- Secondary Market Robustness: Continuation vehicles and secondary fund transactions have become a permanent fixture, providing liquidity solutions in a constrained environment.

- Sectoral Strength: Exits in Energy & Industrials and TMT are driving a disproportionate share of total value.

However, as Andrew Thompson, Asia Pacific Head of PE at KPMG, notes, the exit problem is acute in regions like Asia where:

“secondary markets are not really well developed… and local IPO markets are not uniformly developed for PE-backed companies.”

4. Geopolitical Recalibration & Geographic Diversification

Geopolitical tensions and trade policy uncertainty are no longer background noise; they are central to investment committees’ decision-making. This is evident in the slowdown in China and muted activity in Latin America and parts of Europe.

In response, a theme of “geographic diversification” is gaining steam.

Gavin Geminder, Global Head of PE at KPMG International, observes:

“We’re seeing a polarization of how business gets done in the new world order… If you want to sell into domestic markets, you better have domestic assets, and you’d better also diversify your supply base.”

This is driving two behaviors:

- Cross-Border Deals: Remain strong as firms seek resilient assets and market access globally.

- Onshoring/Supply Chain Diversification: PE firms are actively building portfolio company operations closer to key end markets to de-risk geopolitical exposure.

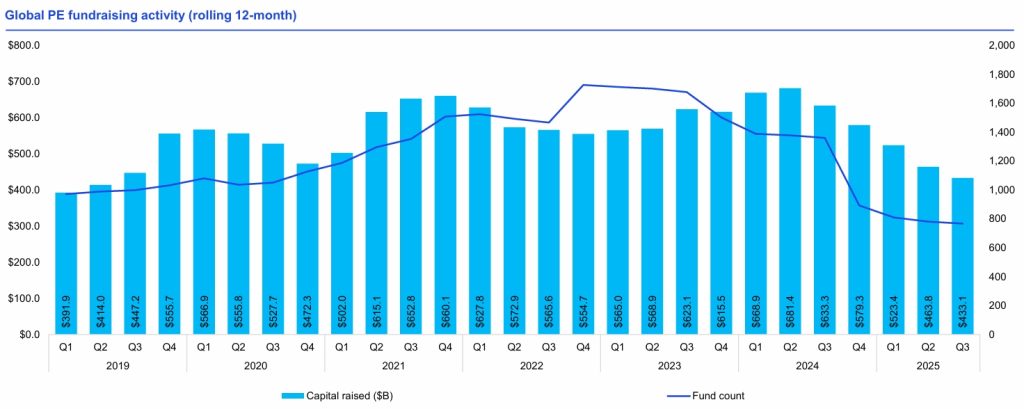

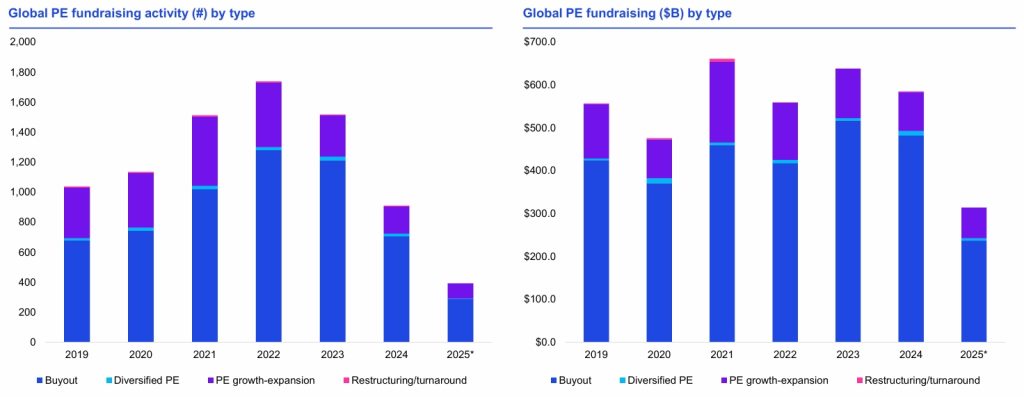

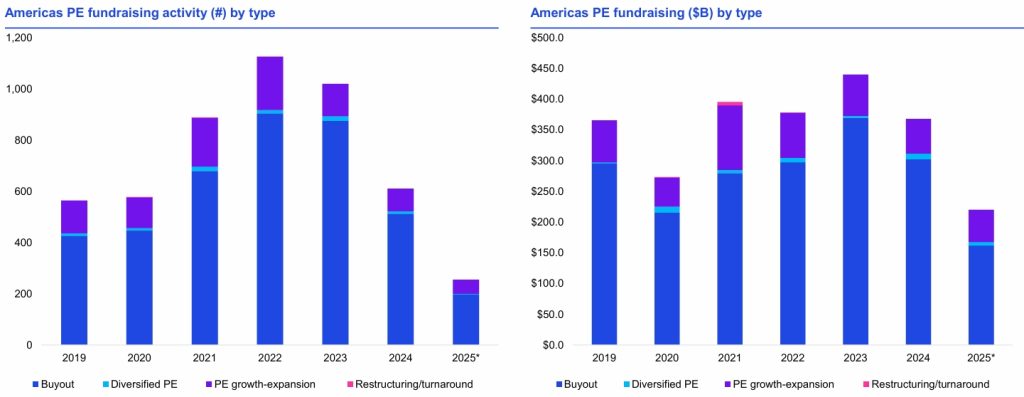

5. Fundraising Winter & The Concentration of Capital

Global fundraising activity is experiencing a pronounced slowdown. Only $314.1B was raised across 393 new funds in the first three quarters of 2025—the slowest pace in a decade. LPs are overwhelmingly cautious.

The capital that is being raised is heavily concentrated:

- 75% of funds closed in 2025 were $1B+ in size.

- Large, established buyout funds are capturing the lion’s share of commitments, while smaller or emerging managers face a vastly more challenging environment.

- The abundance of dry powder (estimated at over $2.5 trillion globally) further reduces the urgency for LPs to commit new capital.

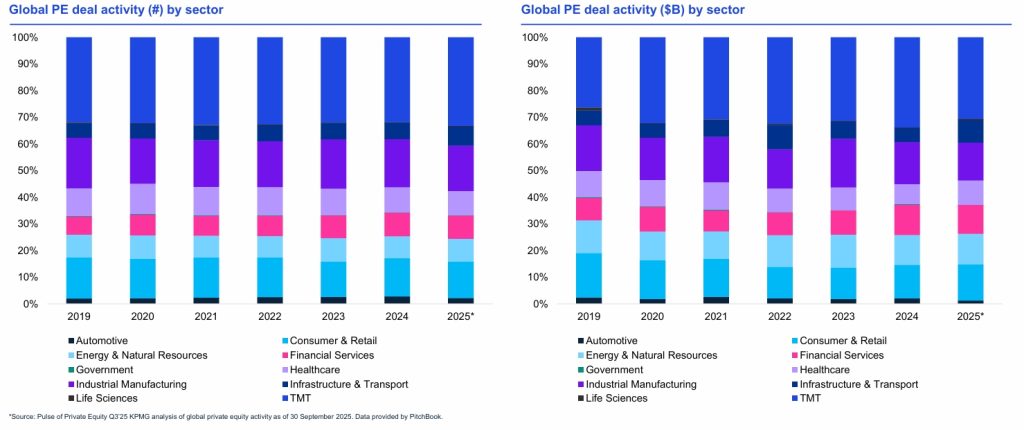

Sector Deep Dive: Where Is Capital Flowing?

Beyond AI infrastructure, several sectors show remarkable resilience or strategic importance:

- TMT: Remains the largest sector by value ($469B YTD), but the focus is shifting within tech towards SaaS, AI-enabling software, and cybersecurity.

- Healthcare: Demonstrates consistent strength, particularly in the EMA region ($42.5B YTD, already surpassing 2023/24 totals). Assets are seen as defensive, with predictable cash flows and insulation from trade tariffs.

- Financial Services: A perennial favorite, especially fragmented subsectors like insurance brokerage in Europe, where buy-and-build consolidation strategies are actively deployed.

- Consumer & Retail: Surprisingly robust in the US and India, driven by premium brands, omnichannel strategies, and grocery/logistics plays conducive to consolidation.

Regional Outlook: Divergent Paths

- Americas (US): Will continue to dominate, driven by megadeals, a reopening IPO market, and heavy investment in AI and energy infrastructure. Canada shows signs of optimism with government alignment on infrastructure spending.

- EMA: Cautious optimism returns as macroeconomic conditions (inflation, interest rates) stabilize. Healthcare and financial services lead, with a growing focus on public-to-private opportunities for undervalued assets. The IPO window, however, remains largely shut outside of India.

- ASPAC: Recovery hinges on geopolitical stability. Australia and Japan show relative strength, while China’s market continues to struggle. South Korea is flagged as a market to watch for the future, potentially mirroring Japan’s PE boom.

Strategic Implications for Investors

- Operational Value Creation is Non-Negotiable. The era of financial engineering is over. As Tilman Ost, EMA Head of PE at KPMG, states, “PE investors need to do way more with their assets these days.” Success demands hands-on operational improvement, technology integration (especially AI for efficiency), and strategic repositioning.

- Scenario Planning for Geopolitics. Investment theses must now include robust geopolitical and trade policy scenario analysis. Building optionality and supply chain resilience into portfolio companies is a key value-creation lever.

- Patience and Partnership on Exits. GPs must cultivate a wider range of exit options, including continuation vehicles, secondaries, and strategic sales, while closely monitoring IPO windows in supportive jurisdictions like the US and India.

- Focus on Core Strengths. In a competitive, concentrated fundraising market, GPs must clearly articulate a defensible and proven strategy—whether by sector, geography, or operational expertise—to attract scarce LP capital.

Conclusion: A Market in Transition

The KPMG Q3 2025 report paints a picture of a global private equity market at an inflection point. Powerful, long-term forces—the AI revolution, the rise of India, and geopolitical fragmentation—are reshaping capital allocation priorities. While short-term caution prevails, evidenced by low deal volume and fundraising, the substantial dry powder and renewed exit activity signal underlying health and preparedness for the next cycle.

The winners will be those who can navigate the complexity: leveraging technology, building resilient and diversified portfolios, and executing on deep operational value creation. The “easy money” era is past; the era of the strategic, value-building investor is in full swing.

🔗 Links for More:

For a deeper analysis of the data and regional insights, download the full KPMG Pulse of Private Equity Q3’25 report from KPMG website or from NeoForm LinkedIn page.

📌 About NeoForm:

At NeoForm Business Partners, we help private equity firms and their portfolio companies navigate complexity, build value, and achieve extraordinary results.

Visit our blog for more insights on M&A, private equity, private debt and private markets.

🔗 Related Readings:

- Midyear Private Equity Report 2025 by Bain

- McKinsey Global Private Markets Report 2025

- Global Private Markets Report 2025: Private Equity Emerging from the Fog

- Private Equity Market Trends in 2025: A Year of Recovery and Strategic Shifts

- The Future of Investing: Private Markets and Credit in 2025

Need tailored solutions? Explore NEO Services or contact our partners to learn how our expertise can help you to elevate and execute your private equity strategies.

4 Comments

Venture Capital Report 2025 Q3: KPMG Insights - NeoForm Business Partners

[…] Private Equity 2025: AI, India & Exit Momentum Reshape Global Inve… […]

Global Banking Review 2025: McKinsey Insights on Winning Strategies - NeoForm Business Partners

[…] Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment […]

Evergreen Private Equity Strategies - NeoForm Business Partners

[…] Private Equity 2025: AI, India & Exit Momentum Reshape&n… […]

How Private Markets Are Redefining Corporate & Investment Banking - BCG 2025 - NeoForm Business Partners

[…] Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment […]