AI’s Unstoppable Surge and IPO Rebound: A Deep Dive into Q3 2025’s Venture Capital Landscape

The winds of change are blowing through the global venture capital landscape, and they carry the unmistakable scent of optimism. After navigating years of macroeconomic uncertainty and a sluggish exit environment, a palpable sense of renewed confidence emerged in the third quarter of 2025. Venture Capital firms Report a dominant force in 2025: artificial intelligence.

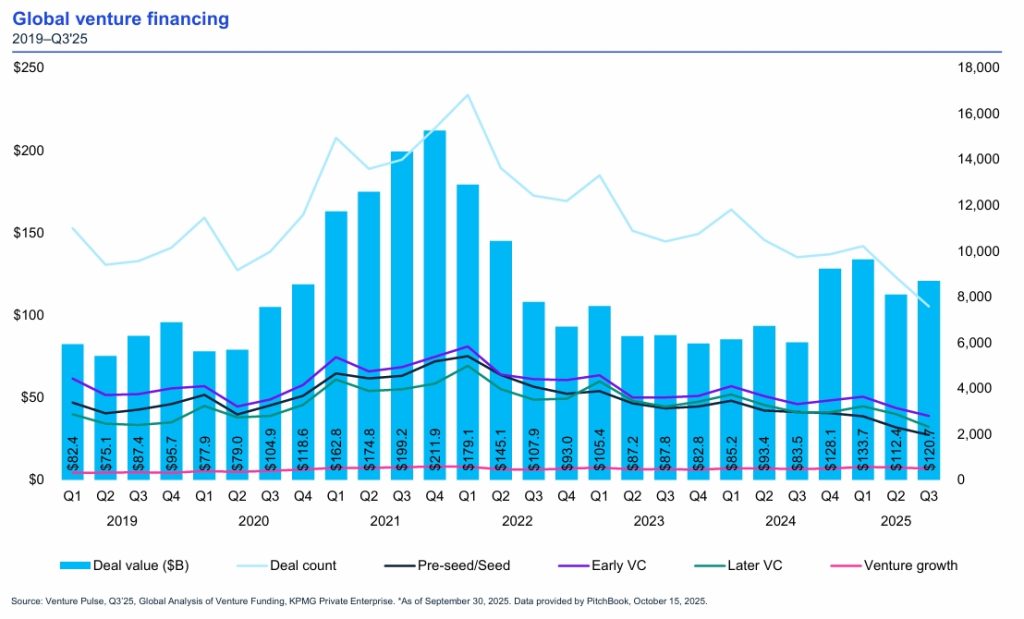

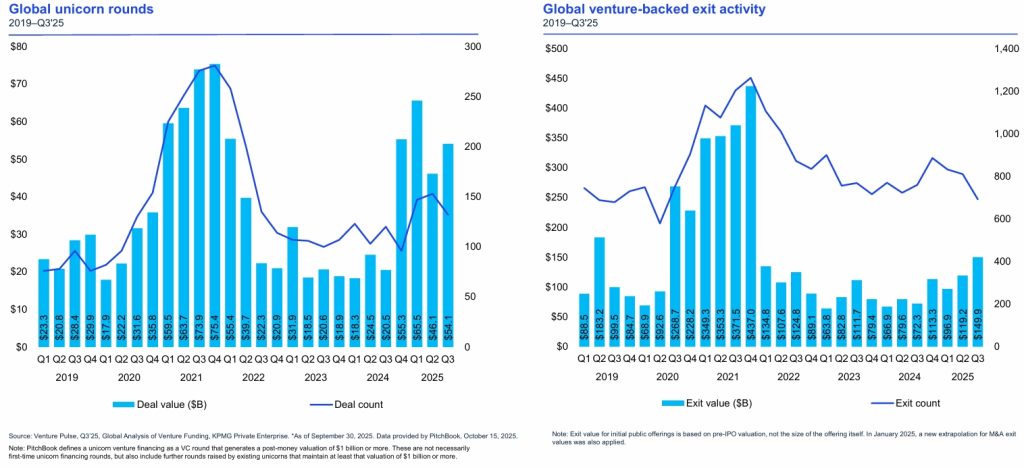

KPMG’s latest Venture Pulse report for Q3 2025 reveals a world where AI isn’t just a sector. AI is the central engine powering investment decisions, fueling historic funding rounds, and reopening long-shut doors for startup exits. With global VC investment climbing to $120.7 billion across 7,579 deals, this quarter wasn’t just about growth; it was about a strategic, concentrated bet on the technologies reshaping our collective future.

This deep dive explores the key trends from KPMG’s latest Venture Pulse report. We’ll look at where the money went, which regions thrived, and what comes next.

Venture Capital Report 2025: AI Is Where the Money Flowing

If Q3 2025 had a headline, it would be written in AI. The sector’s gravitational pull on venture capital is now so strong it’s distorting the entire market.

The Era of the Billion-Dollar Bet

The quarter was bookended by funding rounds of a scale previously reserved for public markets. In a stunning display of conviction, investors poured unprecedented sums into foundational AI model companies:

- Anthropic (US): Raised a colossal $13 billion.

- xAI (US): Secured $10 billion.

- Mistral AI (France): Landed $1.5 billion, proving Europe’s capacity to compete at the highest level.

- Reflection AI (US): Joined the “$1B+ club” with its own landmark round.

This wasn’t merely a US phenomenon. From Canada’s Cohere ($600M) to China’s MiniMax AI ($300M), the race to build and own the underlying infrastructure of the AI era is global. This “capex-heavy cycle,” reflects a harsh reality. Building competitive AI requires immense capital for computational power and a war for scarce, elite talent.

Beyond the Models: The Application Layer Booms

While headlines focus on model builders, the real story of diversification is in the application layer. VC investment flooded into AI-driven solutions across every vertical:

- Enterprise & Productivity: Databricks ($1B) for data/AI infrastructure, Grammarly ($1.3B), Cognition AI ($500M) for coding, and Ramp ($514M) for fintech expense management.

- Industry-Specific AI: Startups applying AI to legal research (Blue J, Canada – $122M), mining exploration, agriculture, and customer service secured significant growth capital.

- Global Spread: Sweden’s Lovable ($200M) for AI-enhanced development tools and various European healthcare AI applications show the technology’s pervasive reach.

AI is now a “must-have” rather than a “nice-to-have”. For startups, lacking an AI-driven component or narrative is becoming a significant disadvantage in the funding race. For investors, the focus has bifurcated into backing the potential platform winners and identifying the teams that can best apply this transformative technology to real-world problems.

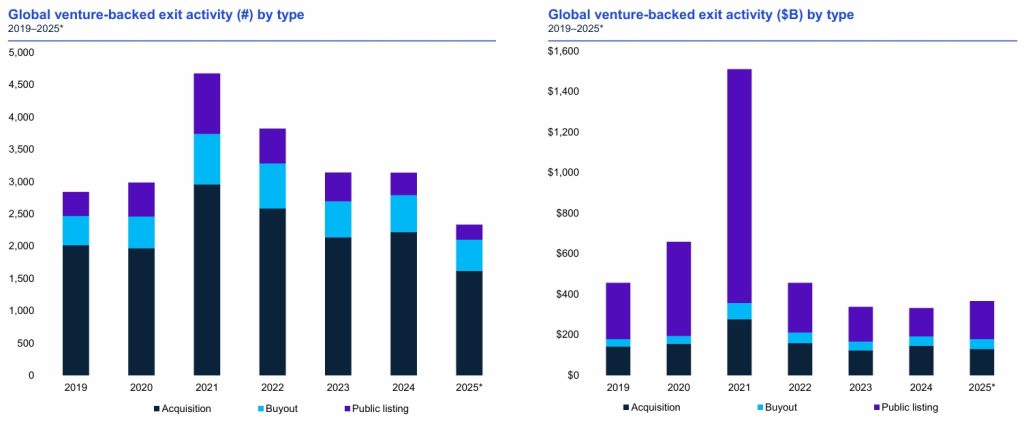

Venture Capital Report 2025: IPO Exits Make a Powerful Comeback

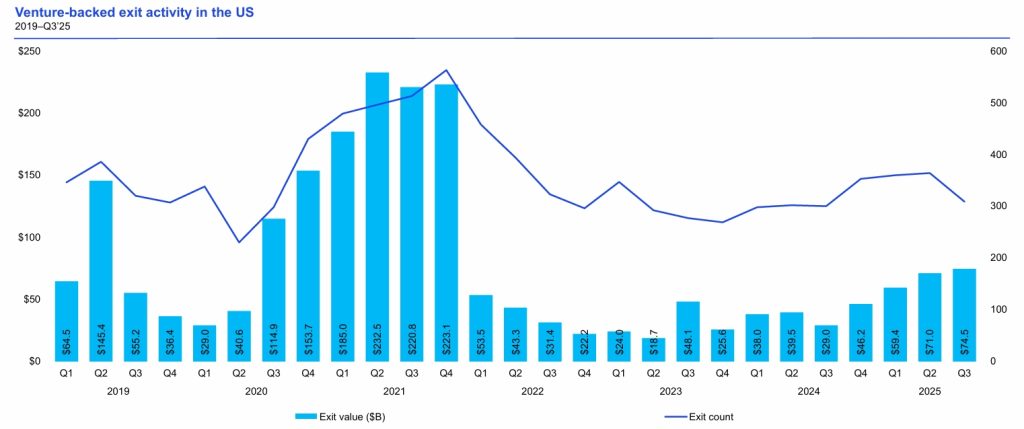

Perhaps the most significant psychological shift in Q3 was the revitalization of the initial public offering (IPO) market, particularly in the United States. After a prolonged drought, the exit window creaked open, then swung wide with a series of high-profile, successful listings.

Successful Debuts Restore Confidence

- Figma: The collaborative design giant raised $1.2 billion, seeing its shares soar 250% on its first trading day.

- Bullish: The digital asset exchange’s $1.1 billion NYSE IPO defied crypto skepticism, with shares up 84% on debut.

- Klarna: The Swedish fintech’s long-anticipated $1.3 billion US listing, with a 15% first-day pop, symbolized the return of cross-border investor appetite for growth stories.

“The cautious optimism we saw last quarter has shifted to genuine optimism”. These successful exits provided the validation the market craved, proving that public investors are once again willing to award premium valuations to innovative, high-growth technology companies.

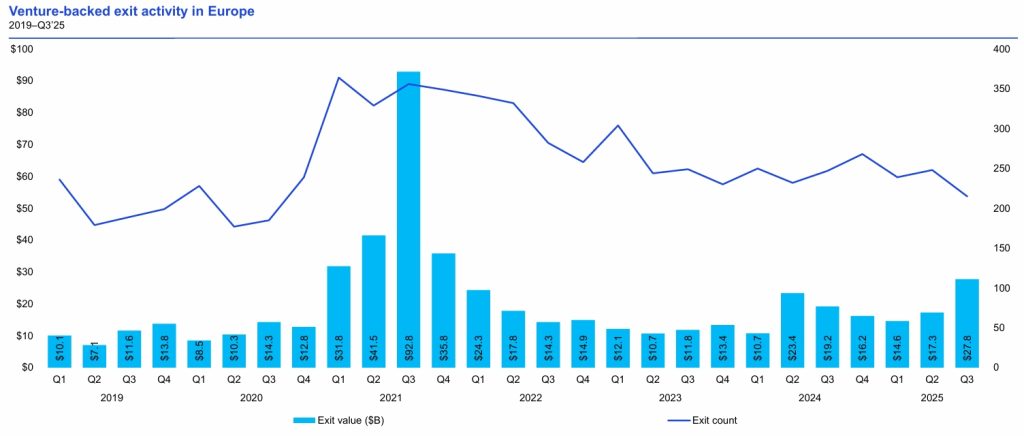

Ripple Effects Across the Globe

The IPO revival wasn’t confined to the Americas:

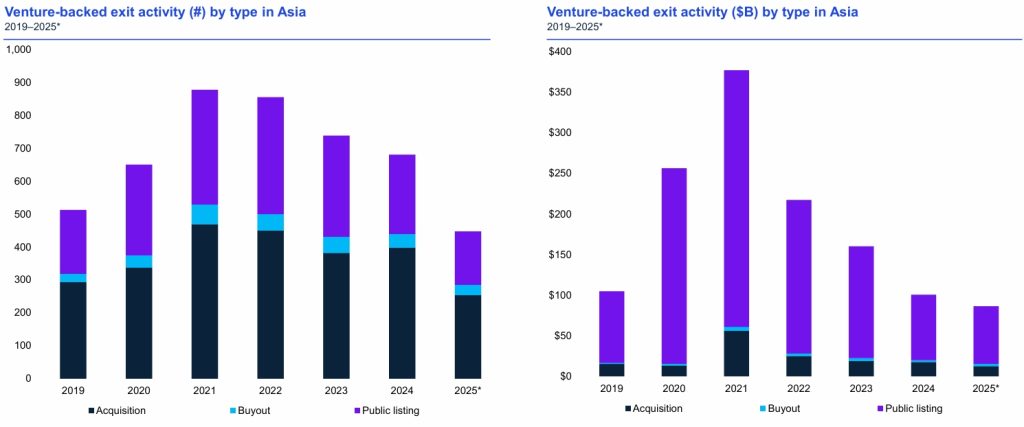

- Asia: Hong Kong’s market saw a rebound. Total exit value for the region already surpassing all of 2024 by the end of Q3. India experienced a banner quarter for exit value, reaching a seven-year high.

- Europe: The successful Klarna listing, while in the US, provided a crucial exit pathway for a European scale-up, bolstering regional confidence.

This resurgence in public market liquidity is crucial. It offers VCs a path to return capital to their investors (LPs), which in turn recycles back into new funds and new investments. It also provides mature startups with a viable alternative to trade sales or endless private rounds, creating a healthier, more diversified ecosystem.

Regional Deep Dive: A Tale of Diverging Fortunes

Venture Capital Report 2025 noticed while AI was the universal theme, its impact and the broader VC landscape varied dramatically by region.

The Americas: The Undisputed Powerhouse

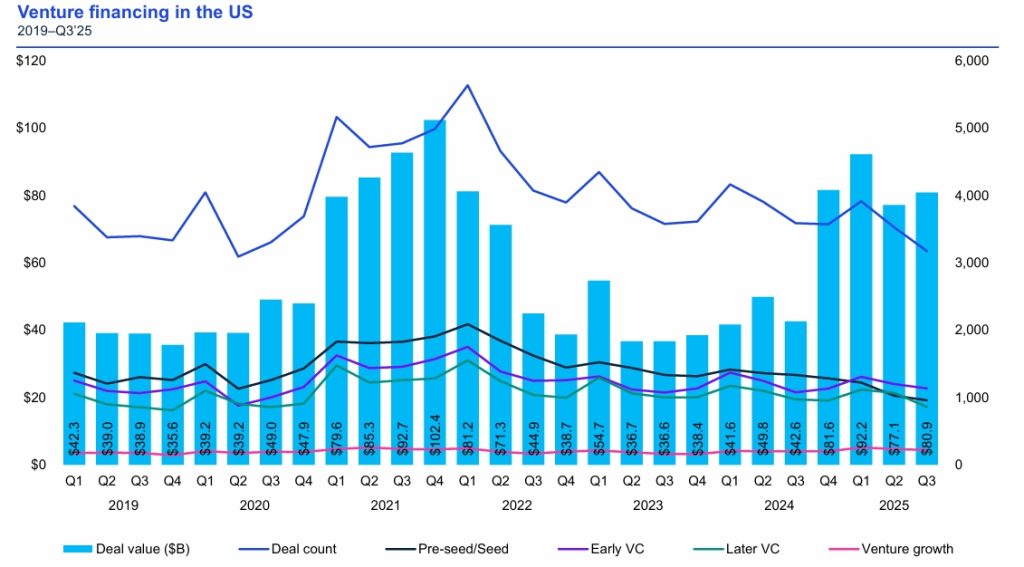

The Americas, driven overwhelmingly by the United States, accounted for the lion’s share of global investment ($85.1B). The US market showcased a potent mix of AI frenzy and exit optimism.

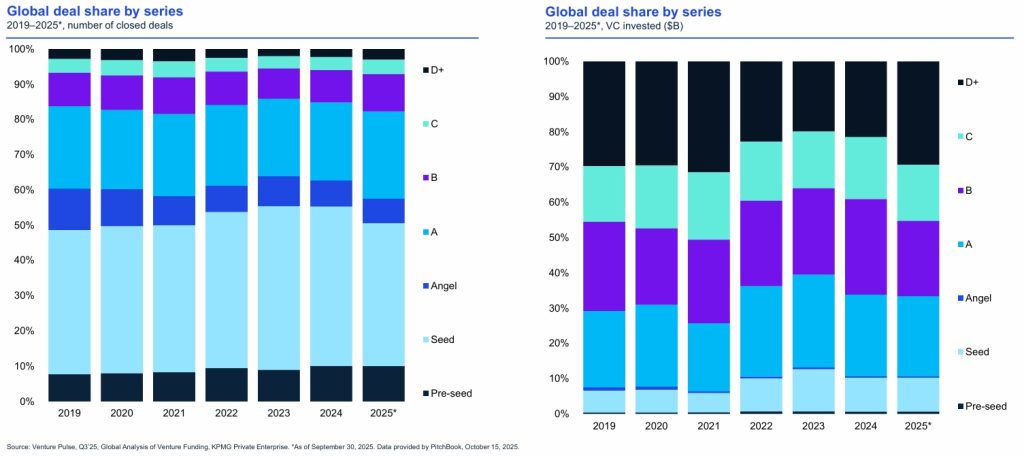

- Deal Dynamics: While overall deal volume dipped to a multi-year low—indicating continued investor selectivity—median deal sizes rose. This points to a “flight to quality,” with capital concentrating on proven leaders and those with clear paths to profitability.

- Beyond the US: Canada shone, led by Cohere’s round. Brazil saw VC investment surge to its highest level since 2022, led by fintech. While Mexico’s market paused, awaiting clarity on US tariff negotiations.

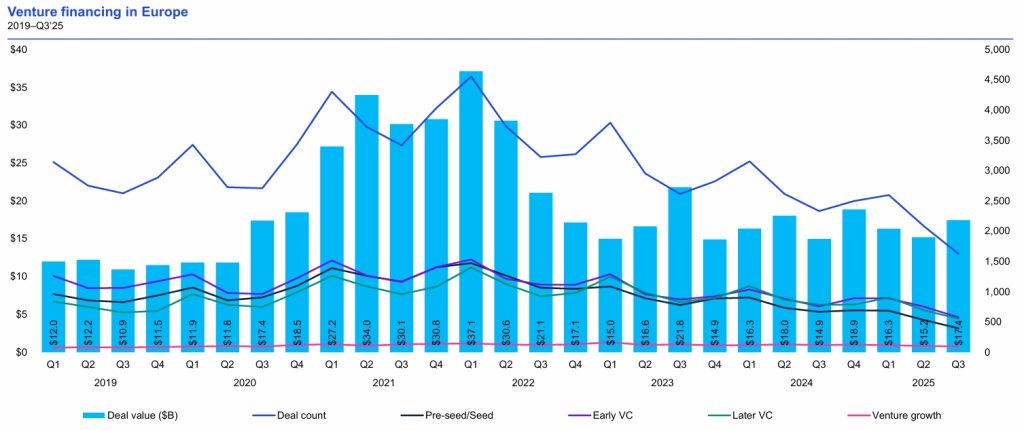

Europe: Steady, Selective, and Strategic

European VC investment held steady at $17.5 billion. It characterized not by a flood of deals but by a handful of strategic mega-rounds (Mistral, Nscale) that underscore the region’s deep-tech strengths.

- Investor Temperament: “bullish overall sentiment… is being met with a measured and diligent investment process.” Due diligence is longer, and the bar for funding is higher, focusing on profitability and clear unit economics.

- Sector Standouts: Alongside AI, defensetech, quantum computing (e.g., Finland’s IQM at $320M), and cleantech attracted significant interest, the latter driven by the EU’s unwavering commitment to energy transition.

- Government’s Role: There is a marked increase in government focus on funding critical infrastructure (like semiconductors) to ensure strategic autonomy, directly influencing VC flows.

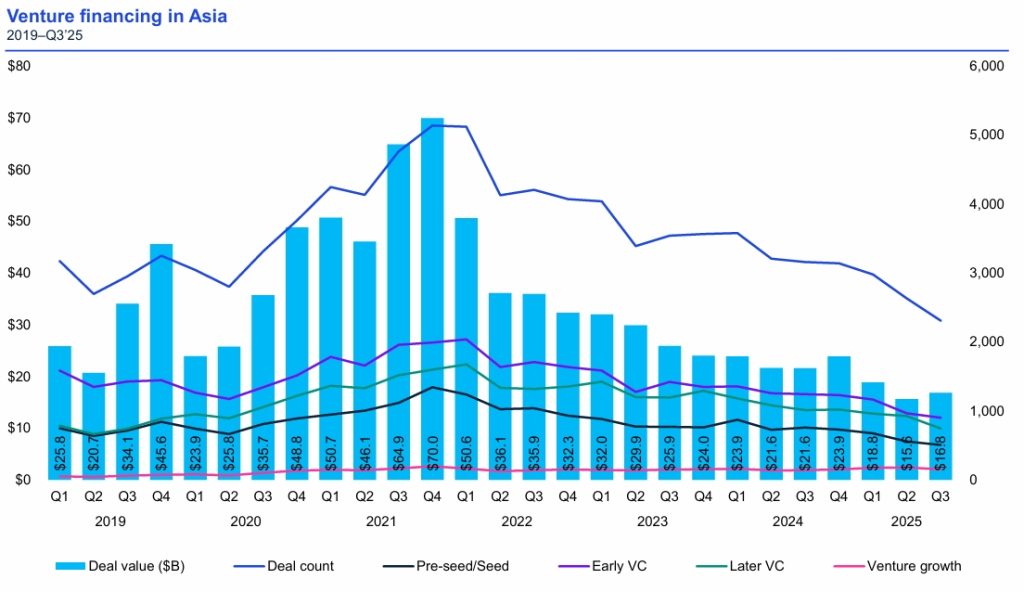

Asia: Muted Activity Amidst Glimmers of Hope

Asia’s VC environment remained relatively soft ($16.8B), constrained by geopolitical tensions and China’s slow economic recovery.

- China’s Shift: The era of chasing unicorns may be waning. Investors are spreading risk across a broader portfolio of AI and deep-tech startups, with notable raises in AI infrastructure (GLP, Runhui) and defensetech (Galactic Energy, Xpeng Aeroht).

- Bright Spots: Japan emerged as a steady hub for AI and deep-tech, heavily supported by corporate venture capital (CVC). India’s strong underlying macros suggest a rebound is imminent once trade uncertainties subside.

- Exit Strength: Despite softer investment, Asia’s IPO activity, led by Hong Kong, showed remarkable vigor, offering a crucial liquidity path.

Africa: The Emerging Frontier

For the first time, Venture Pulse highlights Africa, a region on the cusp of a VC awakening.

- Fintech Leads: As the most mature sector, fintech—especially payments—has birthed all of Africa’s unicorns to date (OPay, Wave, Moniepoint).

- Diversification Begins: Investor interest is expanding into agritech, climatetech, and healthcare, with a focus on innovative, often AI-enabled solutions.

- Evolving Capital Pool: A fascinating trend is the rise of family offices, created by successful African entrepreneurs, which are now becoming active local investors. Blended finance and DFI participation are also growing.

Critical Cross-Cutting Trends Shaping the Future

1. The Resurgence of Hardware and “Hard Tech”

Driven by the needs of the AI revolution and geopolitical tensions, VC is rediscovering hardware.

- AI Infrastructure: Investment is flowing into semiconductors, data centers, and robotics—the physical backbone required to run AI.

- Strategic Autonomy: In Europe and Asia, government policies aimed at reducing reliance on foreign-made critical components are incentivizing investment in domestic hardware capabilities.

- Defensetech’s Rise: With global tensions high, dual-use technologies (with commercial and military applications) saw major rounds from the US to China. Sectors like electric VTOL aircraft, aerospace, and advanced manufacturing are the pioneers.

2. The “Flight to Quality” and Profitability Imperative

As Venture Capital Report 2025 revealed, outside the AI mega-deals, a stricter investment discipline prevails.

- Path to Profitability: Without a clear path to profitability and strong cash flows, “you won’t get a capital market exit.” This is making early-stage fundraising tougher for pre-revenue, burn-heavy models.

- VC as Capacity Builder: Especially in emerging markets like Africa, investors are taking a more active role in helping portfolio companies build operational capacity to ensure sustainable growth.

3. The Evolving Exit Toolkit

While IPOs grabbed headlines, the exit ecosystem is diversifying.

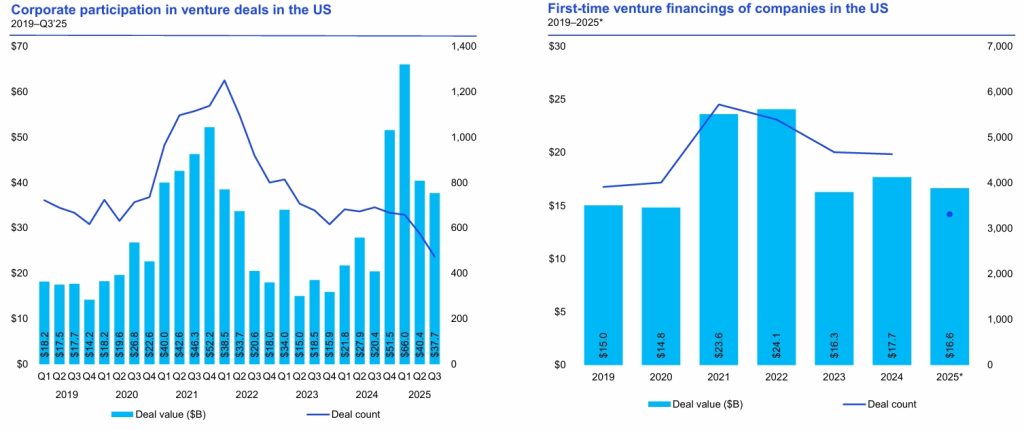

- M&A Gains Momentum: In the US, M&A activity reached a four-year high. Corporates seeking innovation and—crucially—acqui-hires for top AI talent are key drivers. In Japan and Europe, M&A is increasingly seen as a more reliable exit route than the IPO for many companies.

- Secondary Market Stability: A robust secondary market for private shares persists, providing liquidity for investors and employees in companies not yet ready or willing to go public.

Venture Capital Report 2025: What to Watch in Q4 2025 and Beyond

The momentum from Q3 sets the stage for an intriguing close to the year.

- AI’s Dominance Continues: Investment in AI models, infrastructure, and applications will remain the #1 theme globally. Watch for increased activity at the intersection of AI and robotics, energy, and biotechnology.

- IPO Pipeline Fills: With the US window open, a queue of mature startups is expected to test the public markets in Q4 and into 2026. The performance of these new listings will be critical in sustaining the cycle.

- Geopolitics as a Market Driver: Trade agreements (or disputes), tariff policies, and elections will have an outsized impact, particularly on cross-border investment flows into regions like Asia, Mexico, and Europe.

- Regional Specialization Deepens: Expect the US to dominate foundational AI; Europe to lead in quantum, cleantech, and deep-tech applications; Asia to focus on AI hardware and manufacturing integration; and Africa to solidify its fintech lead while branching out.

Conclusion: A Maturing Market in the Age of AI

The Venture Capital Report 2025 paints a picture of a global venture market entering a new, more mature phase. The euphoric “growth at all costs” mentality of the 2021 peak has been replaced by a more calculated, yet profoundly optimistic, stance.

The optimism is fueled by a tangible technological revolution (AI) and renewed exit opportunities. The calculation comes from a sharper focus on fundamentals, profitability, and strategic sectors that align with both economic and geopolitical realities.

For entrepreneurs, the message is to align with these powerful currents. For investors, the challenge is to balance the irresistible pull of AI with disciplined portfolio construction. One thing is certain: the decisions made in this era of AI-driven transformation will define the winners and losers for the next decade. The venture pulse is strong, and its rhythm is increasingly dictated by the beat of artificial intelligence.

🔗 Links for More:

Download the full KPMG Venture Pulse Q3’25 report from KPMG website or from NeoForm LinkedIn page.

📌 About NeoForm:

At NeoForm Business Partners, we help innovative startups, venture capital firms and their portfolio companies navigate complexity, build value, and achieve extraordinary results.

Visit our blog for more insights on M&A, venture capital, private equity, technology trends.

🔗 Related Readings:

- Bain Technology Report 2025: AI is Dividing Leaders

- Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment

- McKinsey Technology Trends 2025: What Is Crucial to Align Your Business

- EY Global IPO Trends Q2 2025: Navigating Volatility, Seizing Opportunity

- M&A Market in 2025: Is a Rebound on the Horizon? Insights from BCG Report

Interested in navigating this complex venture landscape for your startup or fund? Explore NEO Services or contact our partners to learn how our expertise can provide tailored guidance for high-growth businesses at every stage.