Global IPO Trends Q2 2025: How Leading Companies Are Shaping Uncertainty into Opportunity

The global market for Initial Public Offerings (IPOs) in the first half of 2025 is a tale of divergence, resilience, and strategic recalibration. According to the comprehensive EY Global IPO Trends Q2 2025 Report, the landscape is no longer uniform. While some regions and sectors press pause, others are experiencing a stunning resurgence, rewriting the rules of global capital flow.

At NeoForm, we understand that an IPO is more than a transaction; it’s a transformational event that demands impeccable preparation and strategic foresight. This deep dive into the latest data will equip you with the insights needed to navigate this complex environment, whether you’re a founder, investor, or executive contemplating the public markets.

Global IPO Trends H1 2025 Summary: A World of Contrasts

The headline figures reveal a market in transition. Globally, 539 IPOs raised $61.4 billion in H1 2025. While the number of deals saw a slight decrease (-4% year-over-year), total capital raised surged by an impressive 17%, indicating a trend towards larger, more substantial offerings.

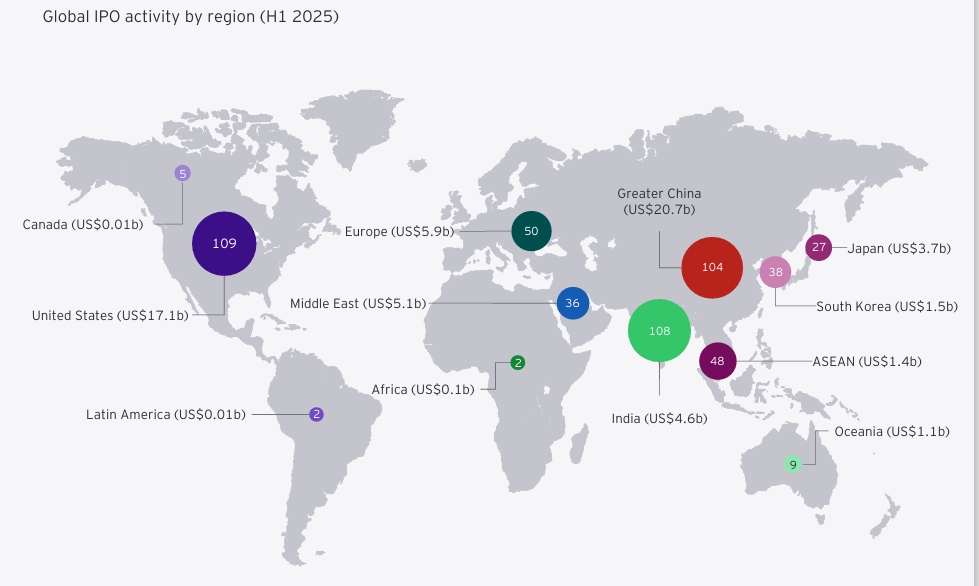

The most dramatic story is one of geographical realignment. Greater China has staged a remarkable comeback, capturing a staggering one-third of all global IPO proceeds—a massive leap from just 12% a year ago. This surge, fueled by mega-listings in Hong Kong, stands in stark contrast to Europe, whose share of the global IPO pie shrunk from 27% in H1 2024 to just 10% in H1 2025.

This shift underscores a world grappling with policy uncertainty, whipsawing market volatility, and geopolitical tensions. The CBOE Volatility Index (VIX) ranged five times wider than in the same period last year, compelling companies to stay private longer, pursue smaller listings, or radically rethink their exit strategies.

Global IPO Trends: A Regional Deep Dive

The global IPO landscape is fragmented, with clear winners and regions facing headwinds.

The Americas: US Momentum vs. Canadian and Latin American Caution

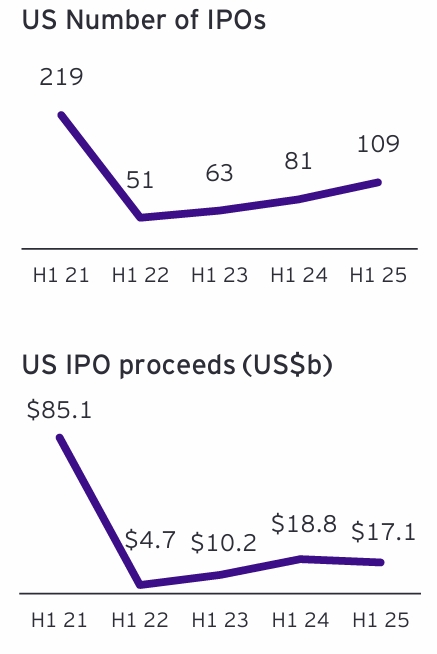

- United States: The US market demonstrated robust health, leading in deal count with 109 IPOs—its strongest first-half performance since the 2021 peak. While proceeds saw a slight decline (-9% to $17.1B), the market’s depth is undeniable. A strong finish to Q2, with nine significant IPOs in June, signals renewed optimism.

- Canada & Latin America: Activity remained subdued. Canada saw only five small IPOs, while Brazil marked its fourth consecutive year without a single listing, with issuers opting for follow-on offerings instead amidst persistent macroeconomic challenges.

Asia-Pacific: The Engine of Global Growth

- Greater China: The standout story of 2025. The region launched 104 deals raising $20.7B, a 33% increase in volume and a monumental 218% surge in proceeds. Hong Kong was the star, seeing a sevenfold increase in proceeds to become the world’s leading exchange by capital raised, driven by massive listings like Contemporary Amperex Technology ($5.3B).

- India: Despite a 30% drop in volume to 108 IPOs, proceeds held steady at $4.6B, reflecting a market focused on larger, higher-quality offerings. A strong pipeline suggests a potential rebound in H2.

- Japan & South Korea: Japan saw fewer deals but a 270% jump in proceeds, thanks to the landmark $3B listing of JX Advanced Metals. South Korea recorded its second-highest H1 deal count in 22 years, with 38 IPOs raising $1.5B.

- ASEAN: The region faced headwinds, with listings declining -27% YOY. Malaysia was a bright spot, hitting a 20-year high in deal count, while Indonesia and Thailand saw significant slowdowns.

EMEIA: A Tale of Two Halves

- Europe: Activity declined sharply, with deal volume down -15% and proceeds falling -58% to $5.9B. Investor selectivity intensified, prioritizing profitability and resilience. Sweden was a rare exception, delivering the region’s only mega-IPO.

- Middle East: Showed resilience with 36 IPOs (up 24%), raising $5.1B (up 31%). The Kingdom of Saudi Arabia (KSA) dominated regional activity, accounting for 25 of these listings.

- Africa: Activity was minimal but showed growth from a tiny base, with two IPOs raising $0.1B.

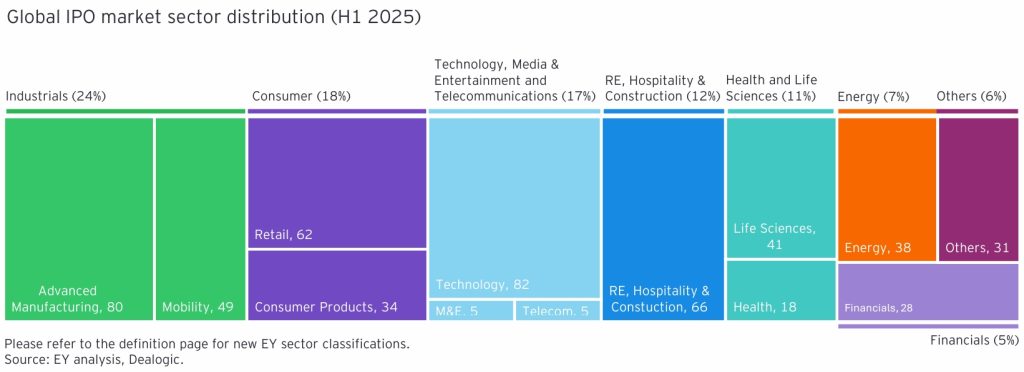

Sector Spotlight: Where is the Capital Flowing?

Geopolitics and national strategic priorities are powerfully shaping the sectoral global IPO trends.

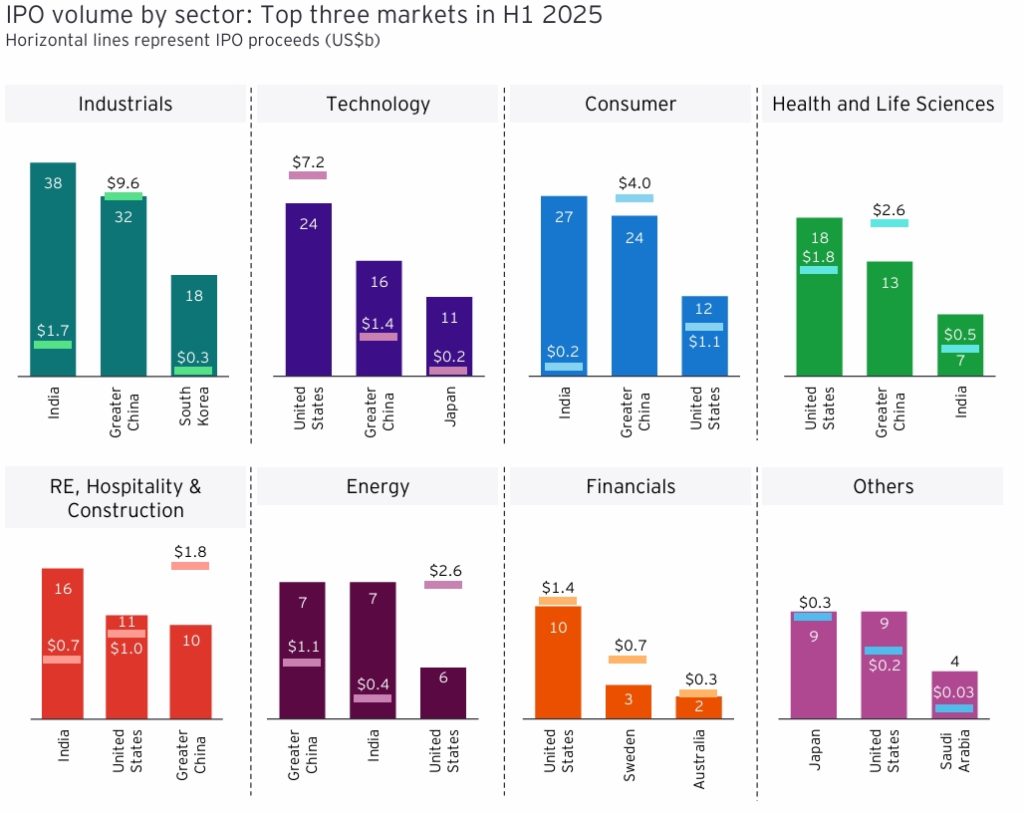

1. Industrials Take the Lead

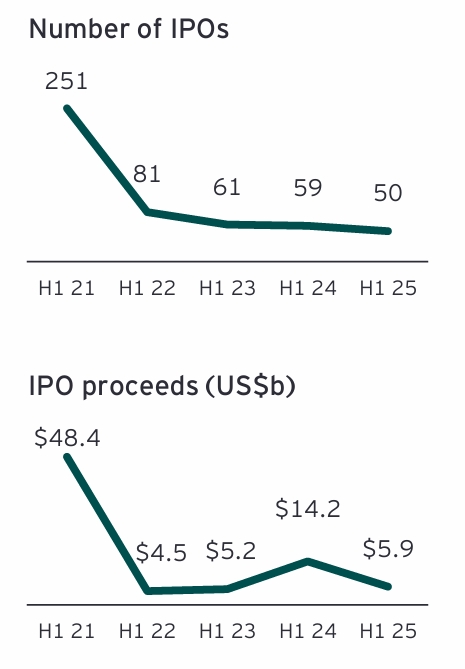

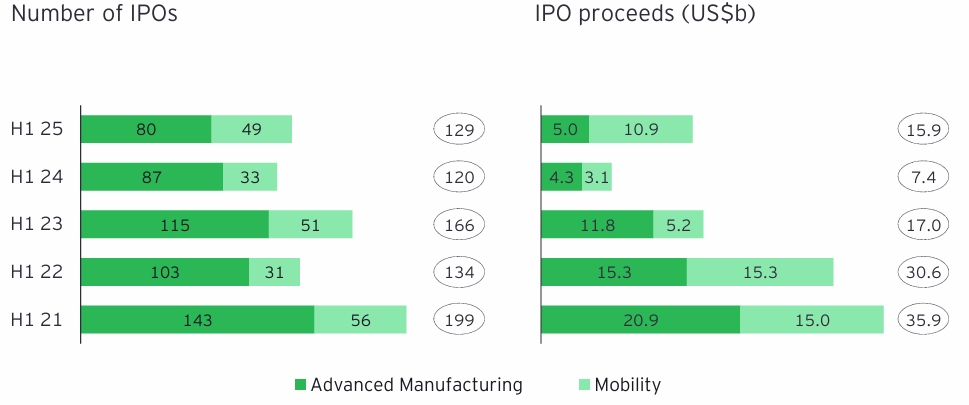

The Industrials sector was the undisputed leader in H1 2025, dominating in issuance, capital raised, and growth. 129 IPOs raised $15.9B—a 114% increase in proceeds year-over-year.

- Driving Force: The Mobility subsector, particularly electric vehicle (EV) battery and auto parts manufacturers, especially in Greater China and India. This is a direct result of global supply chain reconfiguration, “reshoring,” and government infrastructure spending.

- Key Trend: Companies are expanding local production capacity to mitigate tariff risks and capitalize on booming domestic EV demand.

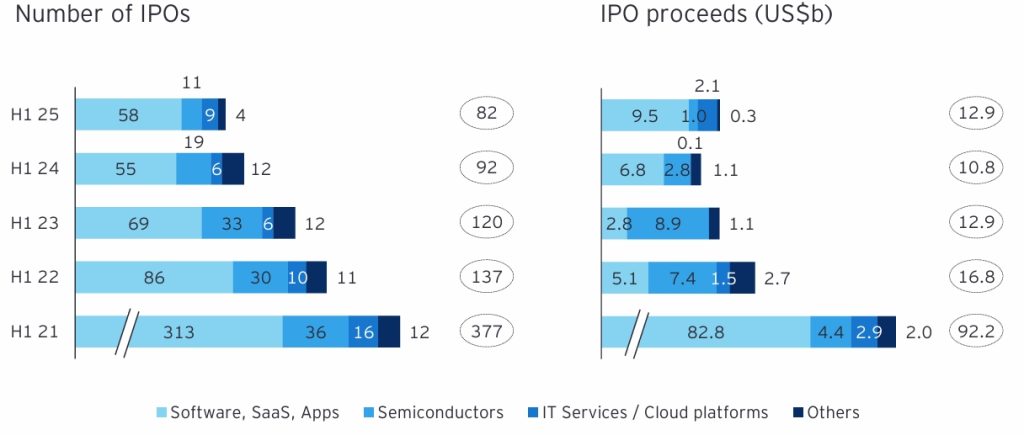

2. Technology: Proceeds Rebound on AI and Software Strength

While deal volume dipped, Technology sector proceeds grew 19% to $12.9B. The rebound was driven by software, with four mega-IPOs exceeding $1B (including Circle Internet and CoreWeave).

- Software & AI: Enterprise applications, eCommerce, and vertical solutions (fintech, healthtech) attracted capital, even as the pure-play AI investment frenzy cooled from its VC peak.

- Hardware Challenges: Semiconductor IPO proceeds fell -64%, with significantly reduced activity from Chinese mainland listings.

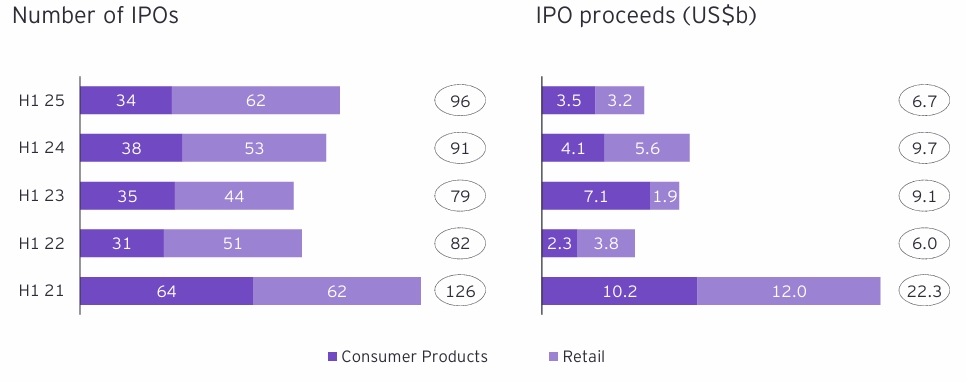

3. Consumer: Asia-Pacific Strength Navigates Volatility

The Consumer sector secured a top-three position by volume, driven by robust retail activity. Hong Kong was exceptional, with consumer IPOs averaging 1,700 times oversubscription.

- Strategic Themes: Companies are using IPO proceeds for portfolio expansion, technology upgrades, and supply chain optimization. Examples include a Chinese tea chain expanding its global store network and a camera maker investing in advanced R&D centers.

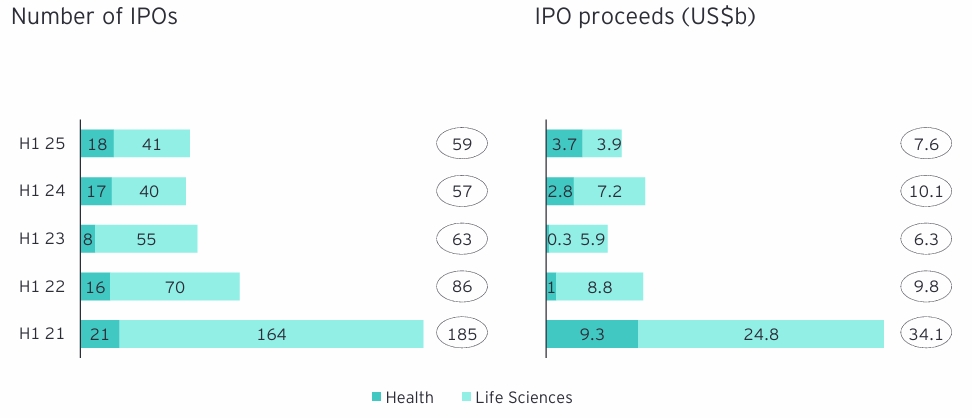

4. Health and Life Sciences: Smaller Deals, Selective Investors

Deal count held steady, but total proceeds fell as average transaction sizes shrunk. Investors showed a strong preference for companies with experienced management and proven products. The US market retreated, while Greater China and South Korea saw growth, with biotech firms increasingly exploring alternative financing like royalty transactions instead of public listings.

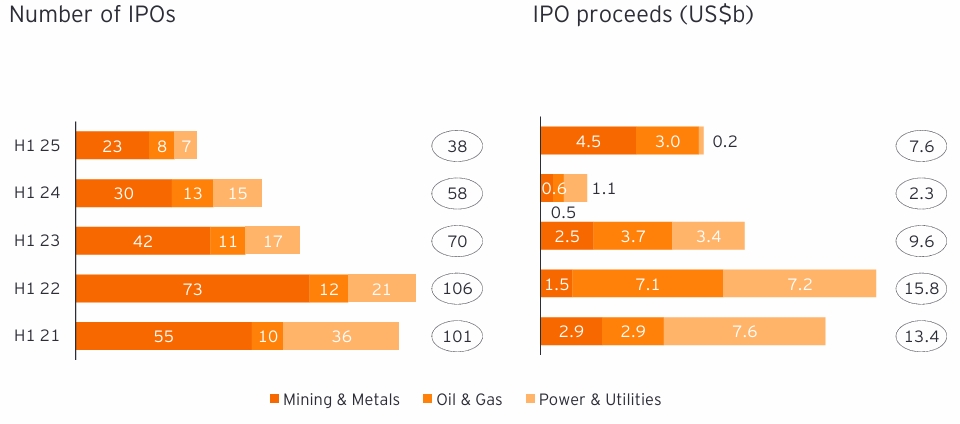

5. Energy: A Tale of Contrasts

Despite fewer deals, Energy sector proceeds tripled to $7.6B, driven by two mega-IPOs: a Japanese non-ferrous metal manufacturer and a US liquefied natural gas (LNG) provider. This reflects investor selectivity and a strategic focus on critical minerals and resilient energy infrastructure.

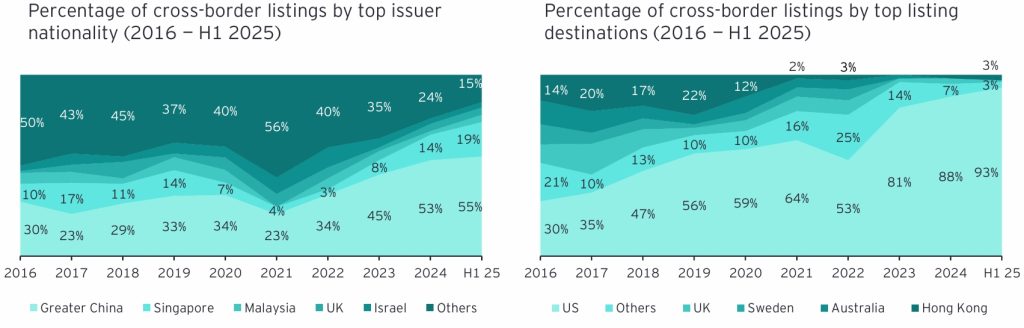

Cross-Border Listings: The Great Rewiring

Cross-border IPO activity hit record highs in H1 2025, accounting for 14% of all global deals, up from just 6% a decade ago. This trend represents a fundamental rewiring of global capital flows.

- The Allure of the US: 93% of all global cross-border IPOs chose to list in the United States, a dramatic surge from 30% in 2016. The US market’s deep capital pools, liquidity, and valuation premiums remain irresistible.

- Key Sources: Companies from Greater China and Singapore are leading this charge, representing 74% of all international listings.

- A Strategic Pivot: Chinese issuers are deliberately choosing smaller deal sizes and less politically sensitive sectors (like Consumer/Retail over Tech) to navigate audit-compliance pressures while maintaining access to US capital.

- Future Challenges: This trend faces headwinds from rising US-China geopolitical tensions and potential regulatory tightening from the SEC, which may push large Chinese listings toward Hong Kong in the future.

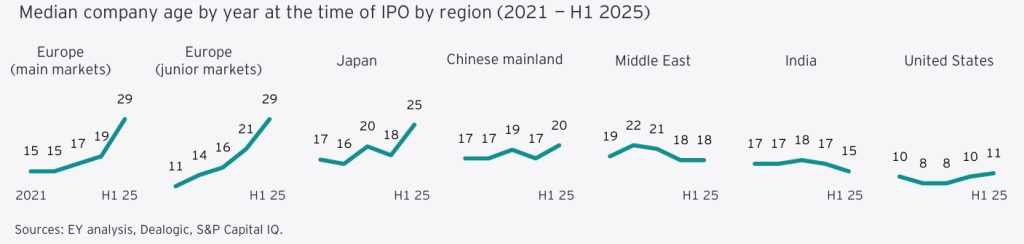

The IPO Readiness Imperative in a Volatile World

The path to going public has become more complex. Market volatility is the new normal, and the “IPO window” is open only to the most credible and well-prepared issuers.

The EY Private Equity Exit Readiness Study 2025 found that 78% of firms are holding assets beyond their typical five-year horizon, reinforcing the “private for longer” trend. In Europe, the median age of a company at IPO has surged to 29 years, up from 15 in 2021.

This environment demands a new playbook for IPO candidates:

- Embrace Agile Financial Strategies: With shifting monetary policies, robust risk management and financial agility are non-negotiable.

- Develop a Compelling Equity Story: Investors are looking beyond traditional financial metrics. The EY survey reveals that three of the top five investment factors are non-financial: Research & Innovation, Brand Strength, and Quality of Corporate Strategy.

- Prepare for a Dual-Track Process: Given market uncertainty, companies must simultaneously prepare for both an IPO and M&A, maximizing optionality to choose the optimal exit path.

- Prioritize ESG and Digital Transformation: Embedding a clear ESG strategy and articulating how AI/digital transformation drives value are critical to attracting modern investors.

- Ensure Public Company Readiness: Being “always ready” is key to seizing narrow market windows, which can open and close rapidly.

Outlook for H2 2025 and Beyond: Cautious Optimism

The outlook for the global IPO trends in the remainder of 2025 hinges on two potential scenarios:

- Optimistic Scenario: A broad-based IPO rebound is possible with more cooperative trade frameworks, accommodative monetary policy, controlled inflation, and geopolitical de-escalation. This would stabilize markets and renew investor confidence.

- Cautious Scenario: Persistent inflation, uneven interest rates, and escalating geopolitical tensions could further delay the IPO window, leading to a more selective environment where only the most resilient companies succeed.

Despite the uncertainty, pockets of opportunity are abundant. Companies aligned with long-term, structural trends—reshoring, defense technology, clean energy infrastructure, AI hardware, and biotech innovation—are well-positioned to attract capital and succeed in the public markets.

Conclusion: Shape Your Future with Confidence

The global IPO market of 2025 is not for the faint of heart. It is a market of stark contrasts, defined by volatility and strategic nuance. Success will not come to those who simply wait for perfect conditions, but to those who proactively prepare, build resilience, and craft a compelling narrative for long-term value creation.

The dramatic resurgence of Hong Kong, the steady flow of capital into strategic industrials, and the record pace of cross-border listings into the US all signal a market that is evolving at breakneck speed. The companies that will thrive are those that can shape uncertainty into opportunity.

🔗 Links for More:

Download and read the full guide from EY website or NeoForm LinkedIn page.

📌 About NeoForm:

NeoForm Business Partners is a strategic and transformational partner specialized in Financial Transformation through financial efficiency and agility.

At NeoForm, we partner with ambitious companies to navigate this complex journey. From building IPO readiness and crafting your equity story to navigating regulatory hurdles and communicating your vision, our expertise is designed to guide you toward a successful public debut.

Visit our blog for more insights on public and private market trends.

🔗 Related Readings:

- The Next Big Arenas of Competition: 18 Super High Growth Sectors Shaping the Future Economy

- McKinsey Global Private Markets Report 2025

- Global M&A Trends 2025: Key Insights from Bain Report

- Credit Market Outlook 2025: Rising Private Credit and Asia-Pacific

- Midyear Private Equity Report 2025 by Bain

Ready to explore your path to the public markets? Contact NeoForm today for a strategic consultation.