Precision Over Size: Why Targeted Strategy Wins in Banking’s New Era

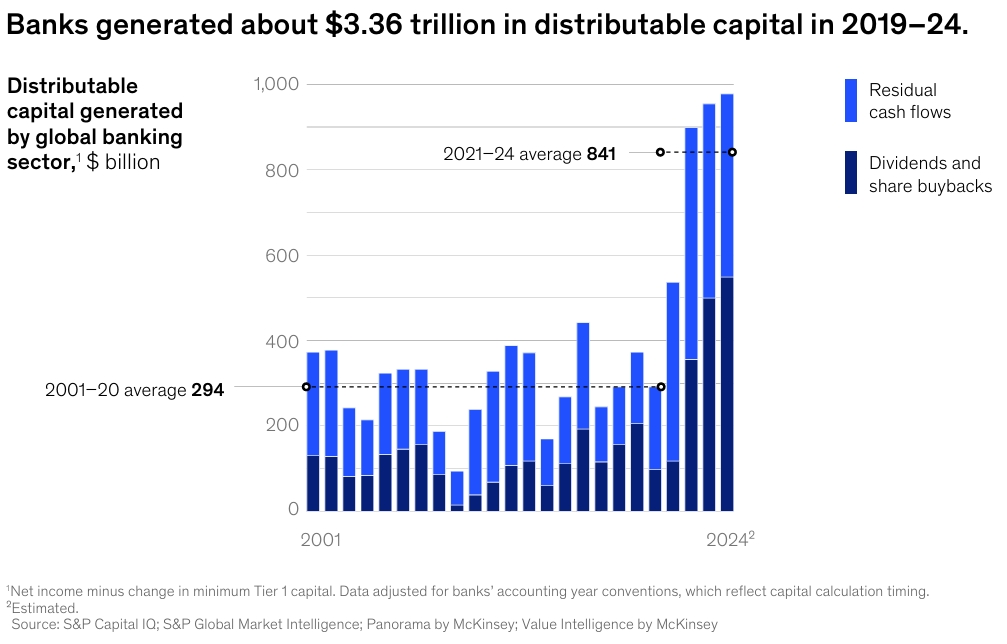

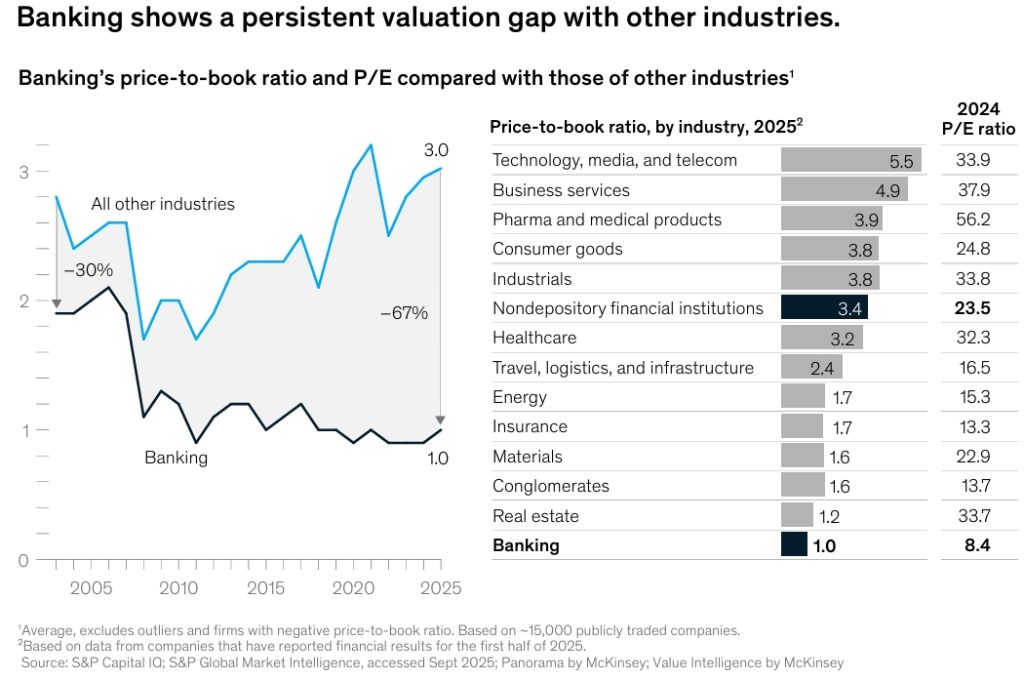

McKinsey’s Global Banking Review 2025 shows that the global banking industry is at a crossroads. In 2024, banks worldwide generated a staggering $1.2 trillion in profits—the highest of any industry. Yet, despite these record numbers, capital markets remain deeply skeptical. Banks trade at a valuation discount of nearly 70% compared to other sectors. Why?

Because markets see these profits as windfall-driven, not sustainable. The truth is, traditional banking models—built on scale, broad segmentation, and blanket digitalization—are running out of road. In an era defined by AI, shifting consumer loyalty, and fierce competition from fintechs, precision has emerged as the defining competitive advantage.

This isn’t just a trend; it’s a fundamental shift in how banks create value. According to McKinsey’s Global Banking Annual Review 2025, the future belongs not to the biggest banks, but to the most focused ones. Welcome to the age of precision banking.

The Paradox of Peak Performance

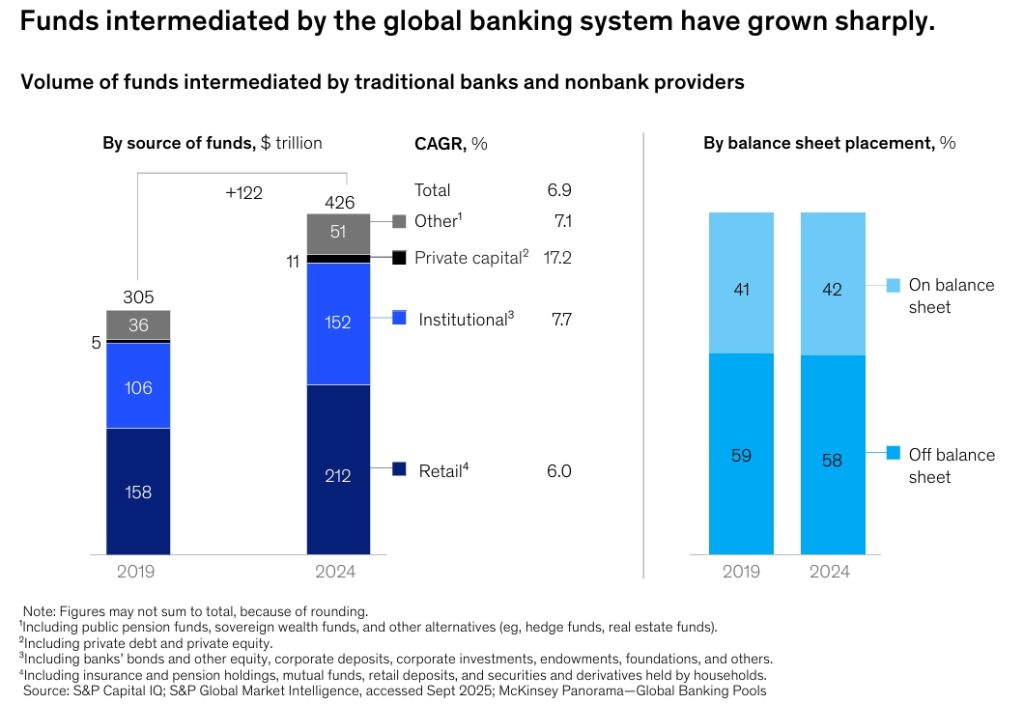

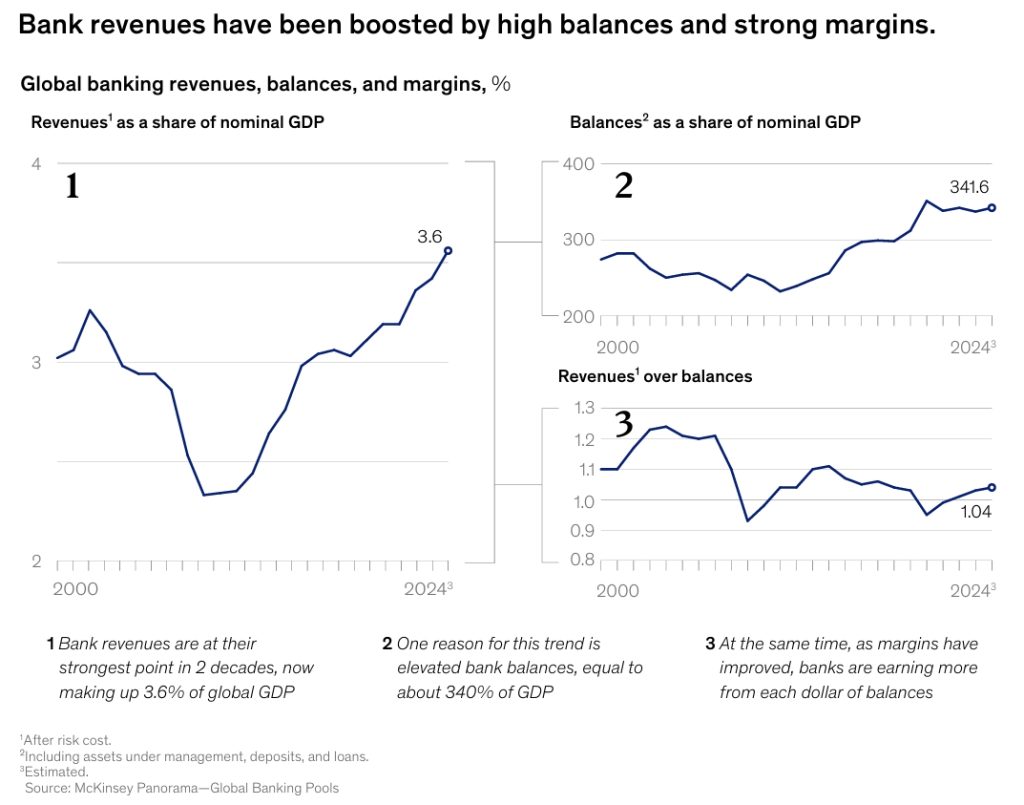

Banks are coming off a historic run. Record balances, favorable interest margins, and low risk costs propelled revenues and profitability to all-time highs. The global banking system now intermediates a colossal $426 trillion—nearly four times global GDP.

But beneath the surface, pressures are mounting:

- Valuation Gap: The industry’s price-to-book ratio languishes at 1.0, far below the cross-industry average of 3.0.

- Eroding Tailwinds: The interest rate boost is normalizing, wealth cycles may be peaking, and risk costs are expected to rise.

- Profit Pool Pressure: Nonbank players—fintechs, private credit firms, and wealth managers—are systematically capturing the most attractive slices of revenue.

The market’s message is clear: past performance, driven by favorable conditions, is not a guarantee of future success. Banks must reinvent their value-creation playbook.

The Precision Toolbox: Four Levers for Future-Proof Banking

So, how do banks transition from broad-stroke strategies to targeted value creation? McKinsey in Global Banking Review 2025 introduces the “Precision Toolbox,” a framework built on four core dimensions:

1. Technology: Surgical Focus Over Blanket Investment

Banks spend more on tech as a percentage of revenue than any other sector, yet productivity gains have been elusive. The new imperative is surgical precision. This means:

- Moving beyond “digital transformation” buzzwords to identify and scale only the AI applications with proven impact—like zero-touch operations or real-time risk monitoring.

- Ruthlessly scaling back unfocused tech programs that don’t directly improve workflows, engagement, or the business model.

- Modernizing core systems not as a monolithic project, but through modular, “hollow-out-the-core” approaches that enable speed and flexibility.

2. The New Consumer: From Segments to a “Segment of One”

Customer loyalty is fading. In the US, only 4% of new checking account applicants now choose their existing bank without shopping around, down from 25% in 2018. Winning today means moving beyond broad labels like “mass affluent” to true individualization.

- Use data and AI to hyper-personalize products, pricing, servicing, and risk at the individual level.

- Recognize that primacy (being a customer’s main bank) is the cornerstone of profitability, and it starts by winning a place in the customer’s initial consideration set.

- Deliver seamless, mobile-first journeys that blend digital ease with human connection for high-stakes moments.

3. Capital Efficiency: Line-by-Line Discipline

Historically, capital management involved sweeping reallocations across business lines. Precision demands micro-level discipline.

- Review capital allocation product-by-product, client-by-client, down to individual risk-weighted assets.

- Deploy AI agents to continuously optimize the balance sheet, simulate scenarios, and uncover underperformance.

- Use partnerships (e.g., with insurers or private credit funds) for risk transfer, freeing up capital for higher-return activities.

4. Targeted M&A: Plugging Gaps, Not Just Adding Bulk

The era of mega-deals for scale’s sake is over. The new M&A playbook is capability- and gap-driven.

- Pursue acquisitions that add specific technologies (like AI models), access to niche customer segments, or presence in strategic micromarkets.

- Focus on disciplined, rapid integration to capture synergies, not just headline size.

- Examples like DBS in wealth management or OTP Bank in Europe show how targeted deals create superior returns.

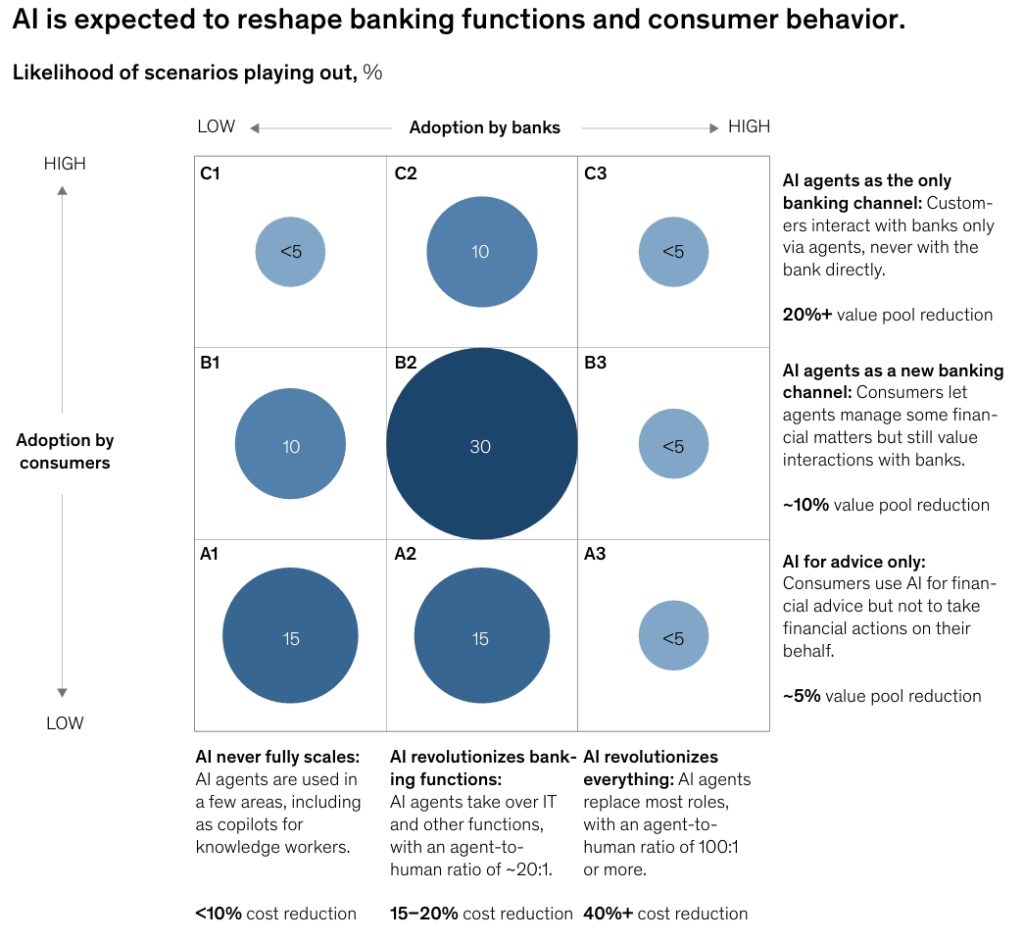

The AI Inflection Point: Agentic Disruption Looms

AI, particularly agentic AI (autonomous systems that execute multi-step processes), is the single greatest force reshaping banking. Its impact will be twofold, affecting both bank operations and customer behavior.

Inside the Bank: Productivity Gains & Competitive Erosion

Agentic AI promises massive efficiency:

- Agent-first customer care: A universal AI layer serving all channels.

- Zero-touch operations: AI teams handling onboarding, document processing, and reconciliations.

- Autonomous risk management: Real-time fraud detection and credit monitoring.

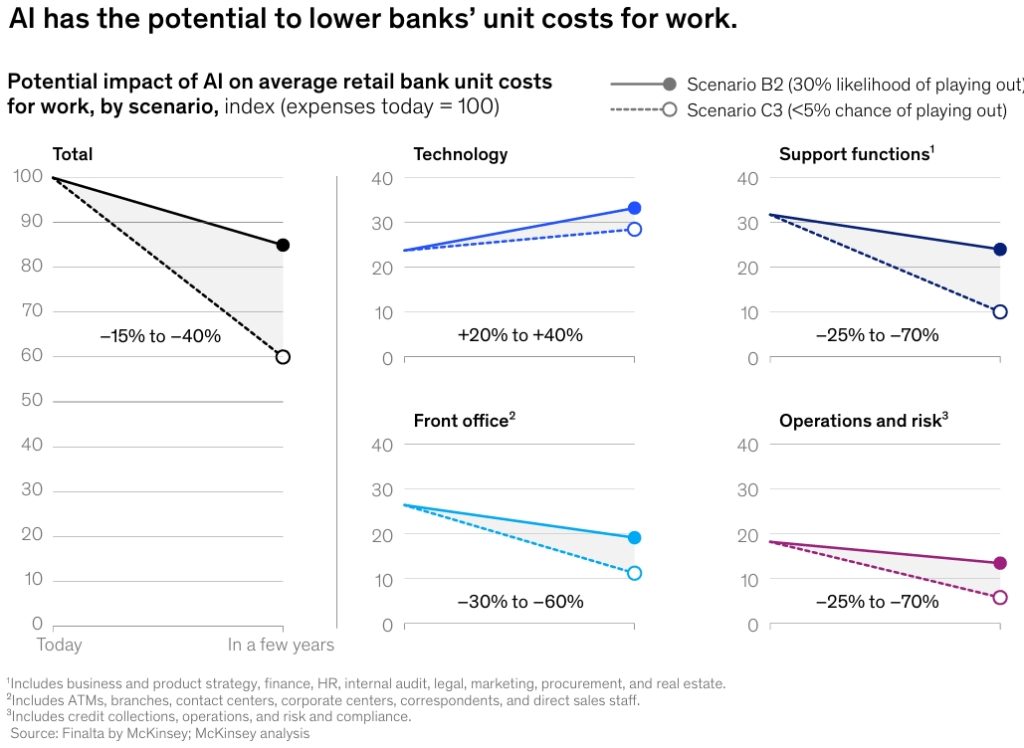

Global Banking Review estimates gross cost savings in some categories could reach 70%. However, the net effect across the total cost base is likely 15-20%, as tech costs rise. Crucially, these savings won’t simply boost bank profits long-term. Competition will force banks to pass most benefits to customers, eroding the temporary advantage.

The Customer Side: The End of Inertia

The bigger disruption may come from how customers use AI. Banking profitability in areas like deposits and credit cards has long relied on customer inertia—the hassle of switching for a better rate.

AI agents could shatter that inertia by:

- Automatically moving deposits to the highest-yielding accounts.

- Optimizing credit card debt, consolidating balances into lower-rate loans.

- Shopping for financial products based purely on value, not brand.

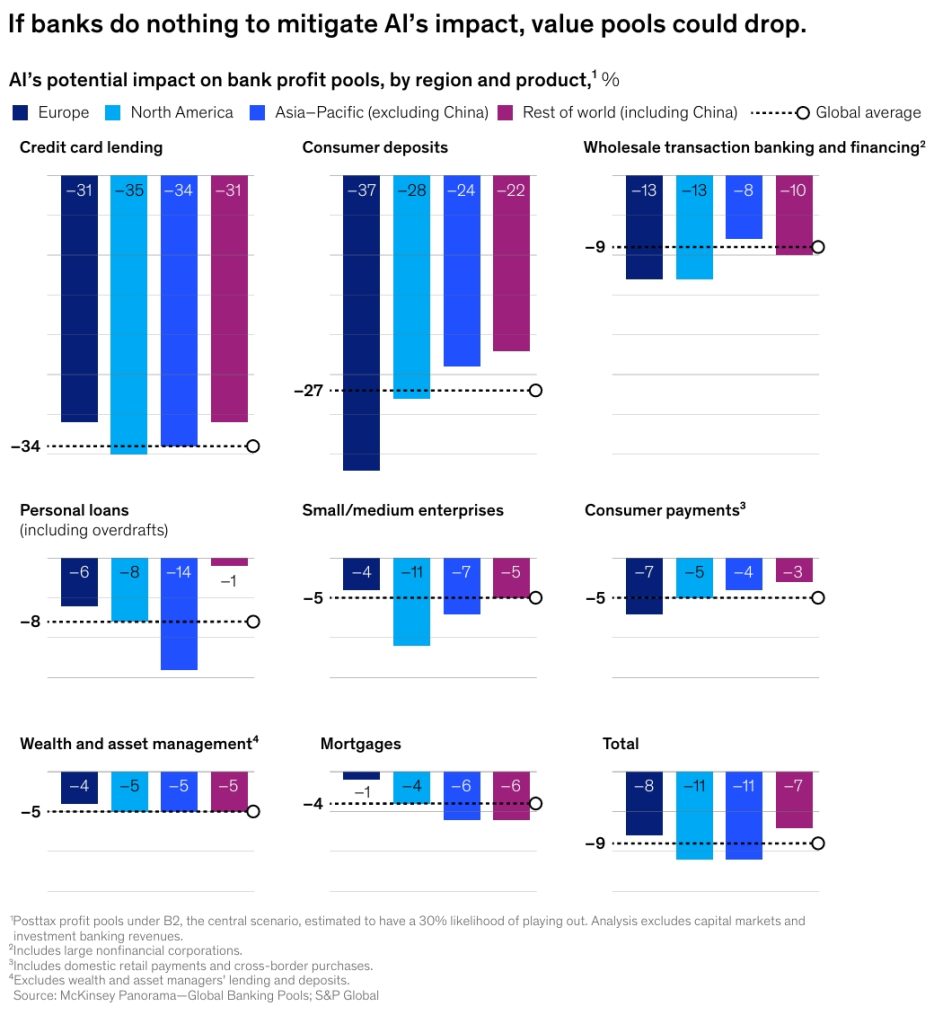

If banks don’t adapt, McKinsey’s central scenario predicts a $170 billion (9%) erosion of global banking profit pools, potentially pushing average returns below the cost of capital.

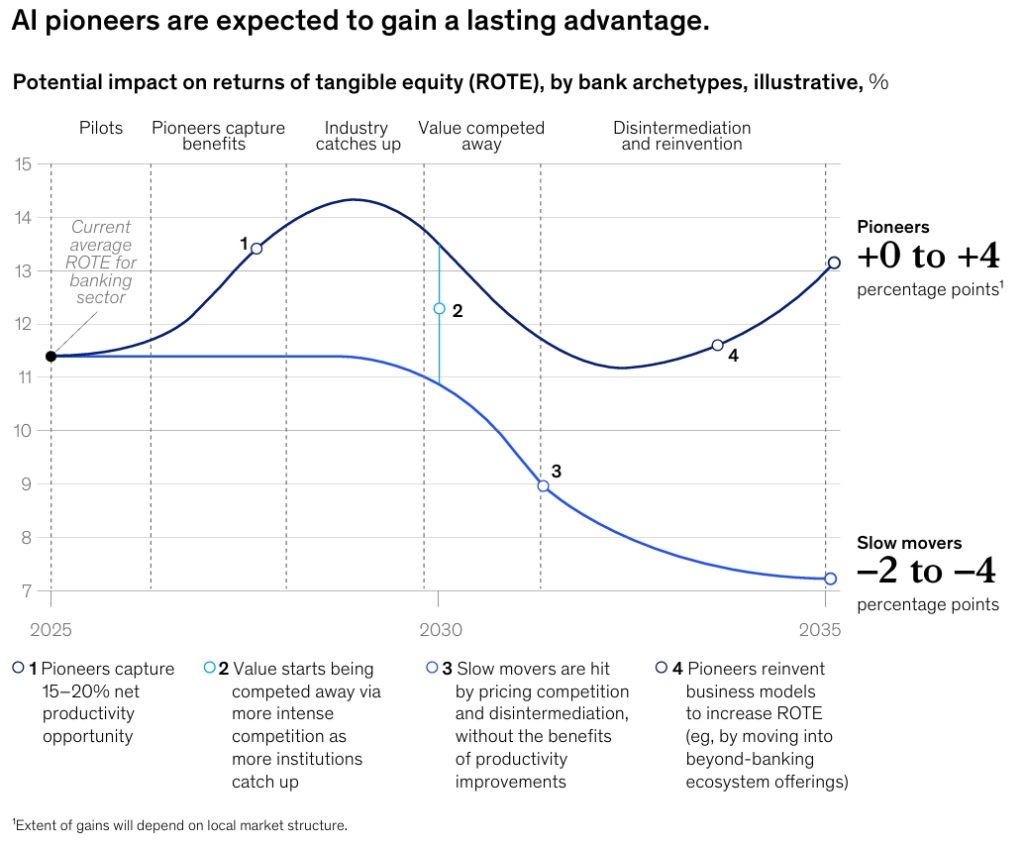

The Pioneer’s Advantage

The AI divide will separate winners from losers. Early adopters who capture the productivity opportunity could see a 4-percentage-point increase in Return on Tangible Equity (ROTE), gaining cash to reinvest and reinvent. Slow movers risk an uncompetitive cost base and irreversible decline.

Winning the New Consumer: Hyper-Personalization is Non-Negotiable

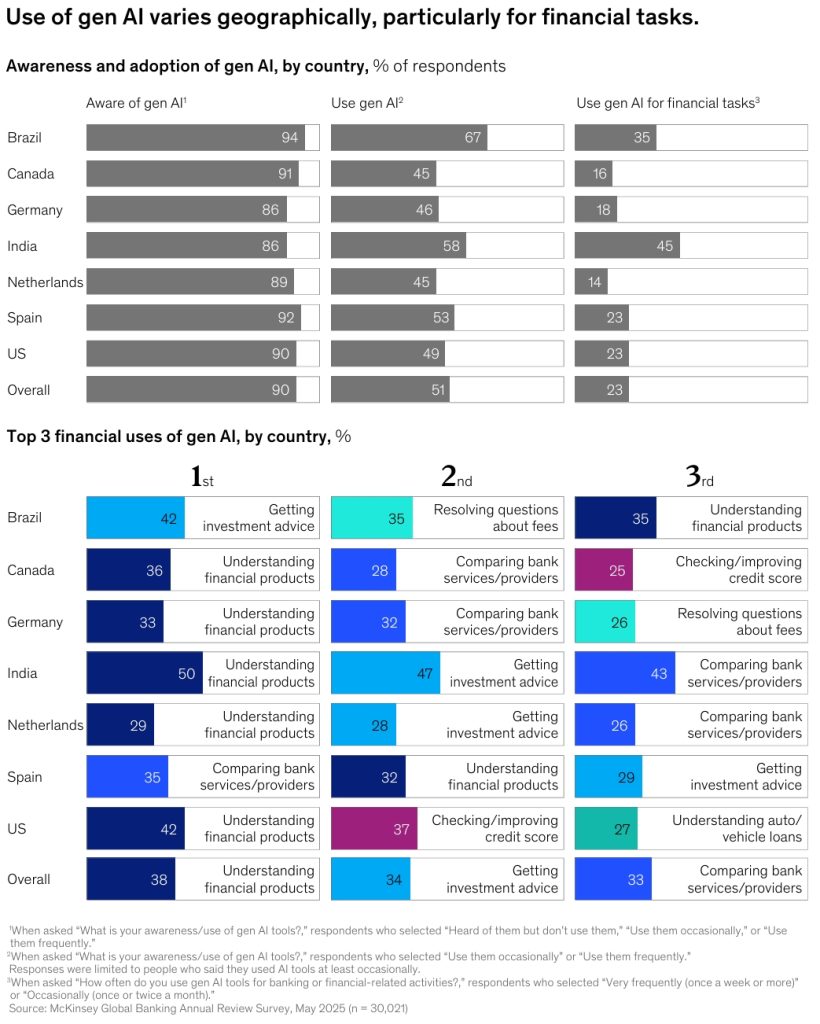

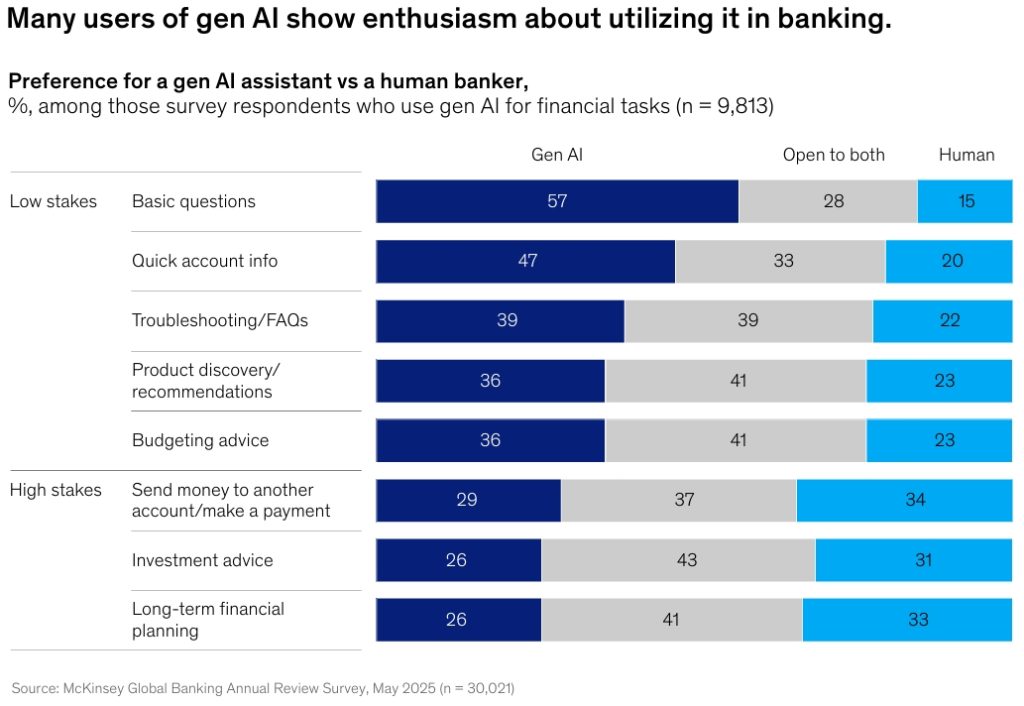

The modern banking consumer is digital-first, less loyal, and has higher expectations. Over half of consumers globally now use GenAI tools, and 23% use them for finance-related tasks. They expect their banks to keep up. Key shifts:

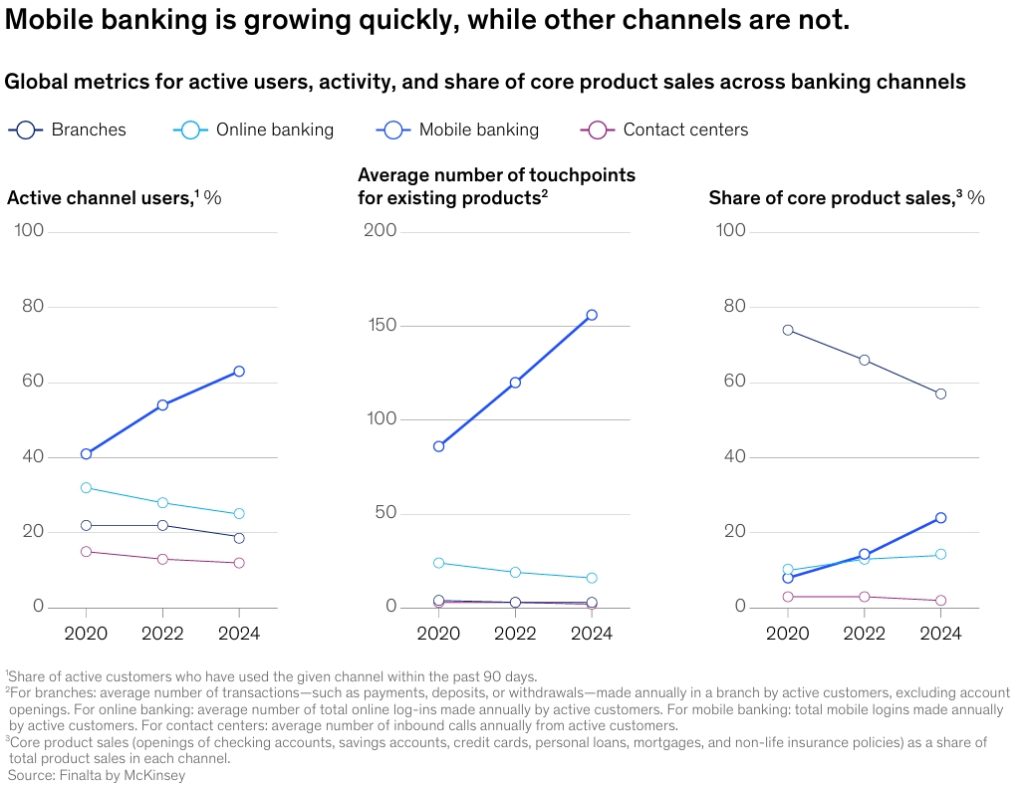

- Mobile as the Orchestrator: Mobile is now the dominant banking channel. Mobile-active customers are significantly more valuable, holding more products and generating higher revenue. A mobile-first, integrated channel strategy is essential.

- The Human-Digital Blend: Despite digital growth, branches remain critical for high-stakes, complex interactions (like mortgage applications). The winning model blends seamless digital journeys with accessible human support.

- Generational Divides: Younger generations (Gen Z & Millennials) prioritize great service over low cost, are more open to new products, and will abandon banks with poor digital functionality. They are the future prime customer base.

Banks must use precision to:

- Win Mind Share: Get into the initial consideration set through targeted awareness and leveraging word-of-mouth (a key decision trigger).

- Supercharge Personalization: Use AI and data to move from segmentation to a “segment of one,” delivering the right offer at the right time.

- Embed AI Trustworthily: Integrate AI tools into customer journeys with strong security and privacy guardrails, meeting rising demand.

Global Banking Review: The Path Forward

Based on Global Banking Review insights, the principles of precision banking are universally applicable:

- Strategy is Now a Data-Driven Science: Moving from gut-feel and scale-based plans to hyper-targeted, analytically rigorous strategies is critical.

- Agility Trumps Size: The ability to rapidly deploy targeted capabilities—be it in tech, customer analytics, or capital allocation—will define leaders.

- Partner for Precision: Few institutions can build all precision capabilities in-house. Strategic partnerships to access specialized tech, data, or distribution channels will be key accelerators.

The message of the Global Banking Review 2025 is unequivocal: the next growth curve will not be won by heft. It will be won by precision—the disciplined, data-driven, and surgical focus on where true value is created.

Banks that retrofit their strategies around the precision toolbox—targeting technology, individualizing engagement, optimizing capital line-by-line, and pursuing gap-filling M&A—will capture outsized rewards. Those waiting on the sidelines, clinging to the old scale-driven playbook, risk irrelevance.

In the end, precision is more than a strategy. It is the new foundational capability for thriving in the AI era of banking.

🔗 Links for More:

Read and download the full report on McKinsey website or from NeoForm LinkedIn page.

📌 About NeoForm:

At NeoForm Business Partners, we partner with financial institutions and FinTechs for financial transformation through financial agility and efficiency to build these very capabilities and elevate financial performance.

Visit our blog for more insights on financial services industries, investment management and private markets.

🔗 Related Readings:

- Global Wealth Management Report 2025: Rethinking the Playbook

- Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment

- The Next Big Arenas of Competition: 18 Super High Growth Sectors Shaping the Future Economy

- How Global Economic Profit Reached an All-Time High

- McKinsey Global Private Markets Report 2025

Need tailored solutions? Explore NEO Services or contact our partners to learn how our strategic and technology solutions can help you build a more resilient and efficient growth engine.

1 Comment

How Private Markets Are Redefining Corporate & Investment Banking - BCG 2025 - NeoForm Business Partners

[…] Global Banking Review 2025: McKinsey Insights on Winning Strategies […]