2026 Outlook for Investment Management, Banking, and Insurance

The Deloitte 2026 outlook reports paint a compelling picture of the financial services industry at an inflection point. Across investment management, banking, and insurance, common themes emerge: the blurring of traditional boundaries, the industrialization of artificial intelligence, regulatory evolution, and the urgent need for operational transformation.

Key Themes in Financial Services

1. The Blurring of Industry Lines

Investment Management:

The distinction between active and passive management is dissolving, driven by the surge in Active ETFs. Meanwhile, private capital is converging with public markets through semi-liquid funds and regulatory changes allowing alternatives in 401(k) plans. Hedge funds are expanding into private credit, while private equity firms are acquiring or partnering with insurers.

Banking:

Stablecoins, backed by the GENIUS Act, are blurring the line between traditional banking and digital assets. Banks must now decide whether to issue, custody, or process stablecoins—or risk losing deposits to non-bank competitors. Tokenized deposits offer a counter-strategy, keeping settlements within the regulated banking perimeter.

Insurance:

Life insurers are increasingly converging with private equity and alternative asset managers. Alliances with firms like Apollo, Brookfield, and Bain Capital are reshaping investment strategies, with insurers allocating more capital to private credit. This convergence demands new capabilities for managing illiquid assets and navigating heightened regulatory scrutiny.

NeoForm Insight: The convergence of private markets with traditional financial services creates immense operational complexity. Firms must build infrastructure capable of handling hybrid products, cross-sector partnerships, and evolving regulatory expectations.

2. AI at Scale: From Pilots to Enterprise Platforms

Investment Management:

AI is graduating from isolated experiments to enterprisewide platforms. Morgan Stanley’s 98% advisor adoption of AI tools and Schroders’ virtual investment committee agent demonstrate real-world ROI. Agentic AI—autonomous systems that execute tasks—is emerging as the next frontier.

Banking:

Banks face pressure to scale AI beyond proofs-of-concept, but success depends on “AI-ready data.” Fragmented infrastructure and siloed compliance data are throttling progress. The report warns that without robust data governance, even ambitious AI models will stall.

Insurance:

AI is delivering tangible wins in fraud detection (up to $160 billion in potential savings by 2032) and underwriting (AIG’s AI assistant handling submissions without new staff). However, many insurers struggle with “fragmented, messy data sprawl,” making foundational data modernization non-negotiable.

NeoForm Insight: AI’s potential is limitless, but its success hinges on data quality, system modernization, and governance. You cannot scale AI without fixing the plumbing first.

3. Regulatory Evolution as a Catalyst

Investment Management:

The GENIUS Act provides clarity for stablecoins, while SEC guidance opens semi-liquid funds to retail investors. In Europe, ELTIF 2.0 is easing cross-border alternative investments. M&A activity is surging as firms seek scale and capability.

Banking:

The GENIUS Act creates a federal framework for payment stablecoins, potentially putting over $1 trillion in deposits at risk. Banks must prepare for new capital and liquidity rules while exploring roles as issuers, custodians, or processors.

Insurance:

Tax changes under the One Big Beautiful Bill Act offer benefits but introduce uncertainties around Pillar Two global minimum tax rules. Regulatory scrutiny of private equity investments in insurance is intensifying, with the NAIC updating risk-based capital formulas.

NeoForm Insight: Regulatory change is no longer a compliance burden—it’s a strategic opportunity. Firms that proactively adapt their operating models to new rules will capture first-mover advantage.

4. The Talent Imperative: Human-AI Collaboration

Investment Management:

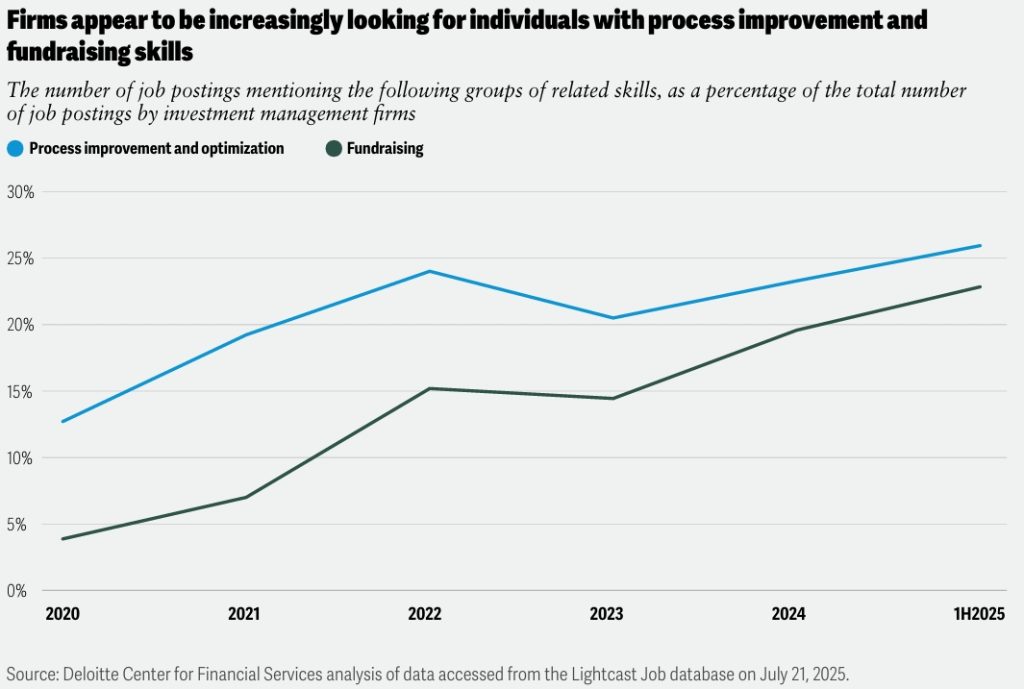

Demand for “AI translators”—professionals who bridge data science and investment strategy—is surging. Process optimization and fundraising skills are now cited in one of every four job postings.

Banking:

Banks must equip mid-career professionals with AI literacy while recruiting specialized talent for prompt engineering and model governance. The report warns that only 4 of 50 banks analyzed have realized measurable ROI from AI, underscoring the need for disciplined value tracking.

Insurance:

The workforce challenge is acute. Veteran employees are retiring, while new graduates recruited for AI expertise are often diverted to traditional workstreams, leading to disengagement. Only 25% of insurance executives have taken tangible action to elevate human skills alongside AI.

NeoForm Insight: Technology alone is not enough. Success requires rethinking how humans and machines collaborate, sharing value created through automation, and designing work experiences that attract and retain next-generation talent.

Part 1: A New Playbook for Investment Management in 2026: The Great Unbundling

The investment management industry is entering 2026 with a paradox. According to Deloitte’s latest 2026 Investment Management Outlook, profit growth remains elusive, yet the opportunities for differentiation have never been greater.

Here are the four seismic shifts redefining the Investment Management Outlook 2026 and what they mean for your operating model.

1. The ETF Revolution Comes to Active Management

For decades, the mutual fund was the king of active management. That crown has officially been passed. The report highlights a structural realignment where actively managed ETFs are taking center stage.

- The Numbers Don’t Lie: In the US, active ETFs’ share of total ETF net inflows skyrocketed from just 1% in 2014 to 26% in 2024. Assets under management for active ETFs grew by 68%, reaching $843 billion.

- The Driver: Investors are no longer choosing between low-cost structures and professional management. They want both. Active ETFs combine the tax efficiency and liquidity of an exchange-traded vehicle with the human judgment of active stock picking.

- The Operational Challenge: For firms, introducing ETF share classes for existing mutual funds isn’t just a product decision; it’s a back-office overhaul. The distinct settlement and operational requirements of ETFs demand significant investment in technology and processes—a core competency of any financial transformation strategy.

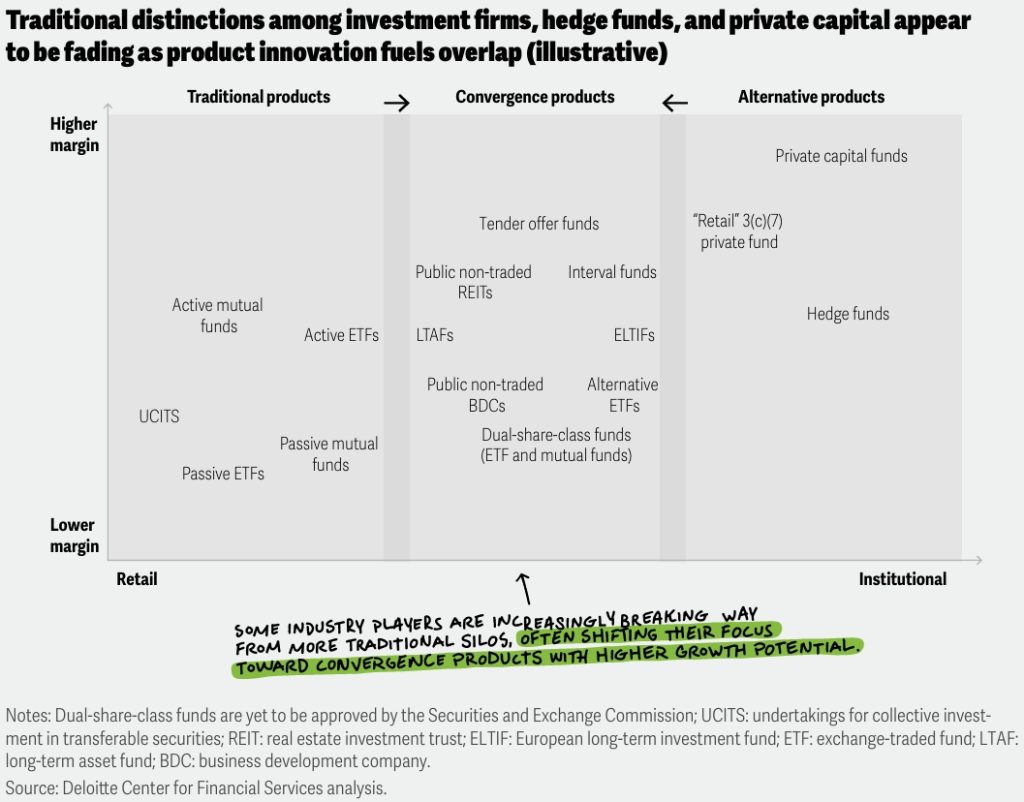

2. Private Markets: The Great Democratization

Private capital fundraising has dipped from its 2021 peak, but the long-term trajectory is clear: Private markets are about to go mainstream. The Investment Management Outlook 2026 points to a regulatory environment that is finally opening the floodgates to retail capital.

- Regulatory Tailwinds: The US Department of Labor has rescinded guidance that discouraged private equity in 401(k) plans. In Europe, the ELTIF 2.0 (European Long-Term Investment Fund) framework is easing the marketing of alternatives to retail clients.

- Semi-Liquid Structures: The rise of interval funds and tender offer funds is allowing retail investors access to traditionally illiquid assets like infrastructure and private credit.

3. The Talent Playbook Has Been Rewritten

As AI and product complexity rise, the demand for traditional portfolio management skills is flattening. Instead, firms are scrambling for a new hybrid talent profile.

- Digital Fluency is Non-Negotiable: The report notes that job postings mentioning AI have risen nearly 25% since 2022. But more interestingly, demand for “AI translators”—liberal arts graduates who can bridge the gap between data science and investment strategy—is surging.

- Process Optimization & Fundraising: In a margin-compressed environment, skills related to fundraising and process optimization are appearing in roughly one out of every four US investment management job postings.

- The Takeaway: It’s no longer enough to be a great investor. You need talent that can educate clients on complex ETF trading mechanics, translate AI outputs into actionable insights, and streamline the capital raising engine. The workforce is becoming a competitive differentiator.

4. AI Scales Up: From Sandbox to Enterprise Platform

Perhaps the most critical shift in the Investment Management Outlook 2026 is the maturation of Artificial Intelligence. We have moved past the era of isolated “sandbox” experiments. AI is now being deployed as an enterprise-wide platform.

- Real-World Use Cases:

- Distribution: Morgan Stanley advisors are using AI to match internal research with client needs, accelerating asset gathering with 98% penetration of the tools.

- Investment Decisions: Schroders has deployed a “virtual investment committee agent” to analyze sector dynamics and risk factors.

- Due Diligence: 64% of PE firms are now using AI to streamline the due diligence process, identifying prospective portfolio companies faster than ever.

- Enter Agentic AI: The next frontier is “Agentic AI”—software systems that can act independently. Imagine an AI agent that screens client interactions, analyzes portfolios for diversification gaps, and alerts relationship managers with compliant recommendations before a human even notices the opportunity.

- The Governance Gap: However, the report warns of a significant risk. While tech investment is accelerating, governance is lagging. Job postings for AI are up, but mentions of AI-specific governance remain generic. Firms must establish robust frameworks—model inventories, risk assessments, and clear data lineage—to ensure they scale safely.

Looking Forward to Investment Management in 2026

The investment management industry is unbundling and rebuilding itself simultaneously. Product lines are blurring (private equity firms moving into credit, hedge funds launching private funds), and technology is becoming the central nervous system of the firm.

The gap between bold, well-governed execution and cautious incrementalism is widening. Leaders who move now to rewire their operating models for this new era will convert the complexity of 2026 into a compound advantage.

Part 2: The New Banking Battleground: AI, Stablecoins, and the Fight for Deposits in 2026

The banking industry is entering 2026 on relatively strong footing, but according to Deloitte’s latest 2026 Banking and Capital Markets Outlook, the year ahead will be anything but predictable. Macroeconomic crosscurrents, the disruptive entrance of regulated stablecoins, and the pressure to industrialize Artificial Intelligence (AI) are converging to create a defining moment for financial institutions.

Here are the four key forces reshaping the Banking Outlook 2026 and what they mean for your institution’s future.

1. The Squeeze is On: Growth Moderation Meets Cost Intensity

The macroeconomic “soft landing” narrative is giving way to a more complex reality. Deloitte forecasts modest GDP growth of 1.4% in 2026, but the path is narrow.

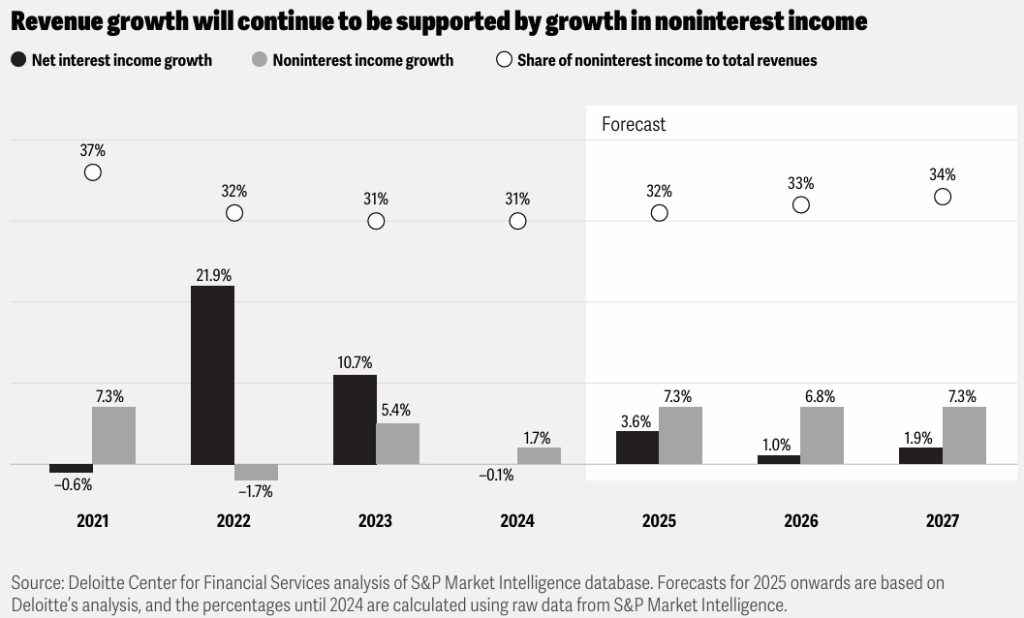

- Revenue Pressures: Net interest income growth is expected to moderate as the Fed potentially drops rates to 3.125%. While lower rates might spark loan growth (especially in C&I lending for AI data centers), deposit costs are sticky. The competition for core deposits remains fierce, keeping funding costs elevated.

- The Fee Income Imperative: With spread income under pressure, noninterest income becomes the star. Investment banking fees are poised to climb on renewed dealmaking, and wealth management is expanding. However, the real game-changer highlighted in the outlook is new fee income from stablecoins, data monetization, and embedded finance.

- The NeoForm View: In a flat revenue environment, efficiency ratios are edging higher. This is not the year for broad cost-cutting; it’s the year for targeted transformation. Banks must reallocate capital toward high-growth fee areas while using automation to strip costs out of legacy processing.

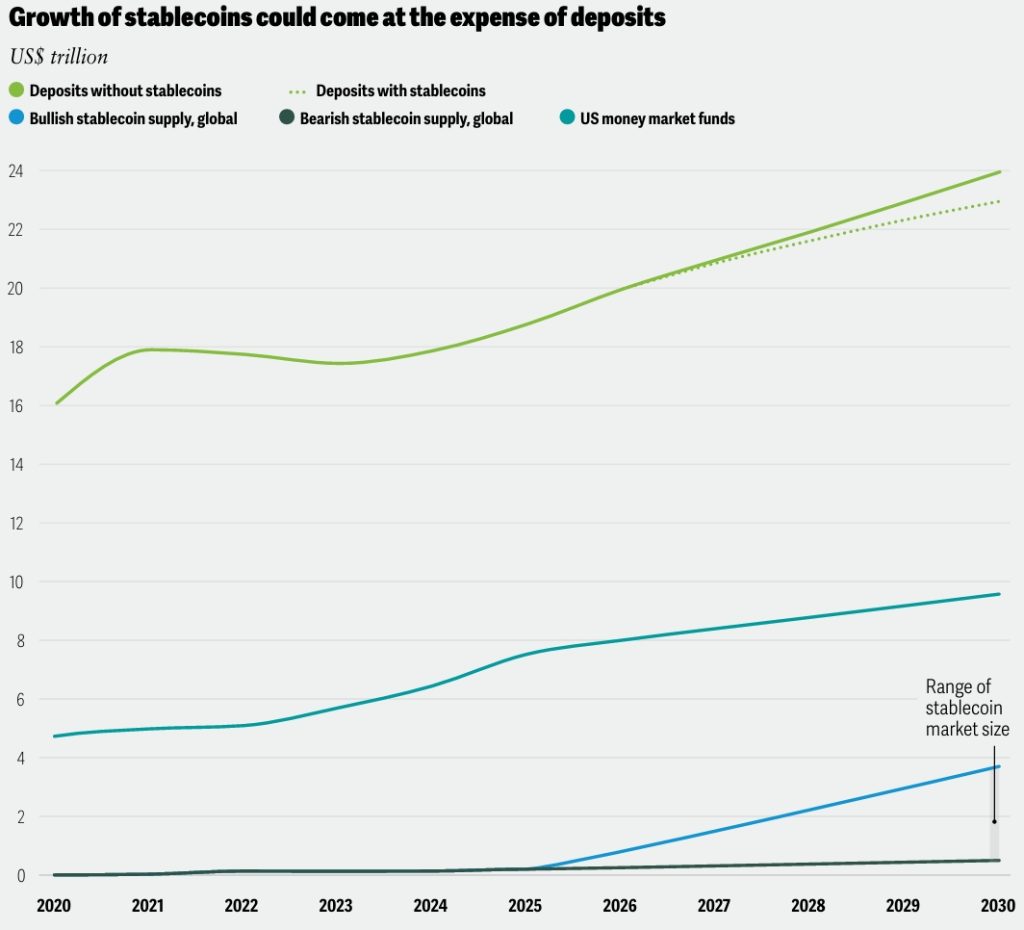

2. Stablecoins Go Legit: The $1 Trillion Deposit Question

The July 2025 GENIUS Act has fundamentally altered the US payments landscape. For the first time, there is a federal legislative framework for payment stablecoins (PSCs), opening the door for traditional banks to engage in tokenized digital assets.

- The Threat: Deloitte estimates that over $1 trillion in bank deposits could be at risk from PSC growth by 2030. Flows will come from corporate working capital, retail transaction balances, and cross-border settlement float. If banks do not act, non-bank issuers will capture low-cost funding traditionally held in low-yield transaction accounts.

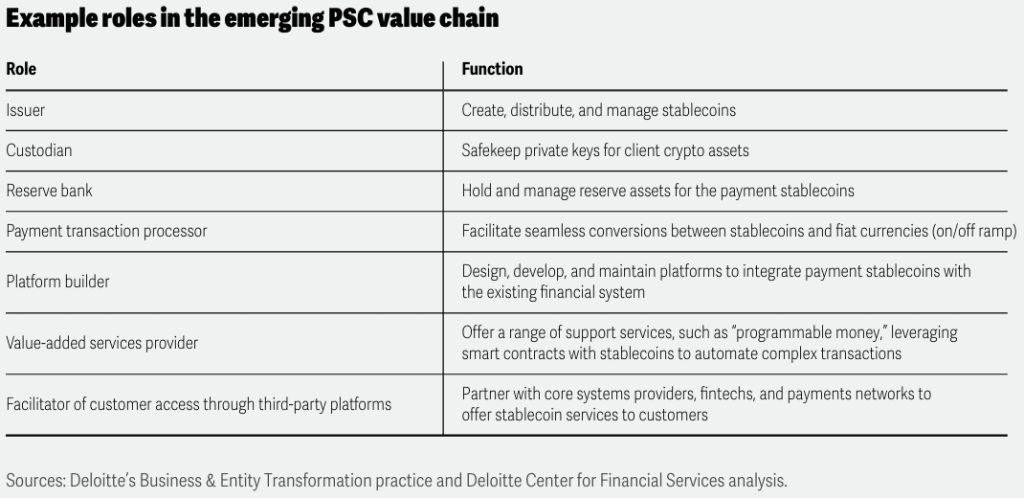

- The Opportunity: The report outlines multiple roles banks can play—Issuer, Custodian, Reserve Bank, or Payment Processor. J.P. Morgan and Citi are already exploring tokenized deposits as a counter-strategy, offering the benefits of instant settlement and programmability within the existing regulatory perimeter.

- The Operational Reality: PSCs and tokenized deposits are not just product decisions; they are core-system evolutions. They demand new capabilities for KYC/AML on the blockchain, private key safekeeping, and integration with legacy core systems. Regional banks may turn to “PSC-as-a-service” solutions, but larger institutions must decide if they will build the “proprietary layers” that make stablecoin services truly their own.

3. AI’s Pivot: From Sandbox to Industrial Scale

The Banking Outlook 2026 makes it painfully clear: The era of isolated AI proofs-of-concept is over. 2026 is the year banks must scale or stall.

- The Governance Gap: Many banks are stuck with “reactive, siloed efforts.” The report argues that success requires a unified vision, a hub-and-spoke operating model (like an AI Center of Excellence), and, critically, a disciplined approach to measuring ROI.

- The Rise of Agentic AI: The next frontier is autonomous agents that can execute tasks. Imagine an agent that monitors transaction flows for fraud and freezes a compromised account before a human even notices. However, agentic AI demands a cultural reset—shifting from a “human-at-the-center” to an “AI-agent-at-the-center” model, with humans in the loop for oversight.

- The NeoForm Perspective: For banks, the “build vs. buy” debate is evolving into an “assembly” approach. You buy the foundation model, but you must build the proprietary layers—the data connectors, guardrails, and workflows—on top. This is where differentiation lies. If every bank uses the same LLM, the only competitive edge is the quality of your proprietary data and the talent you have to orchestrate it.

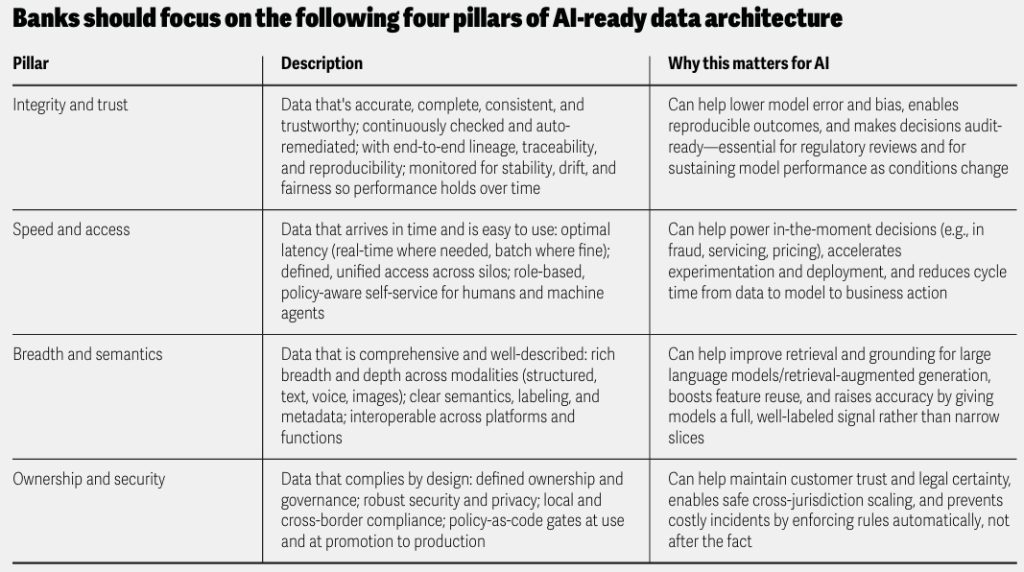

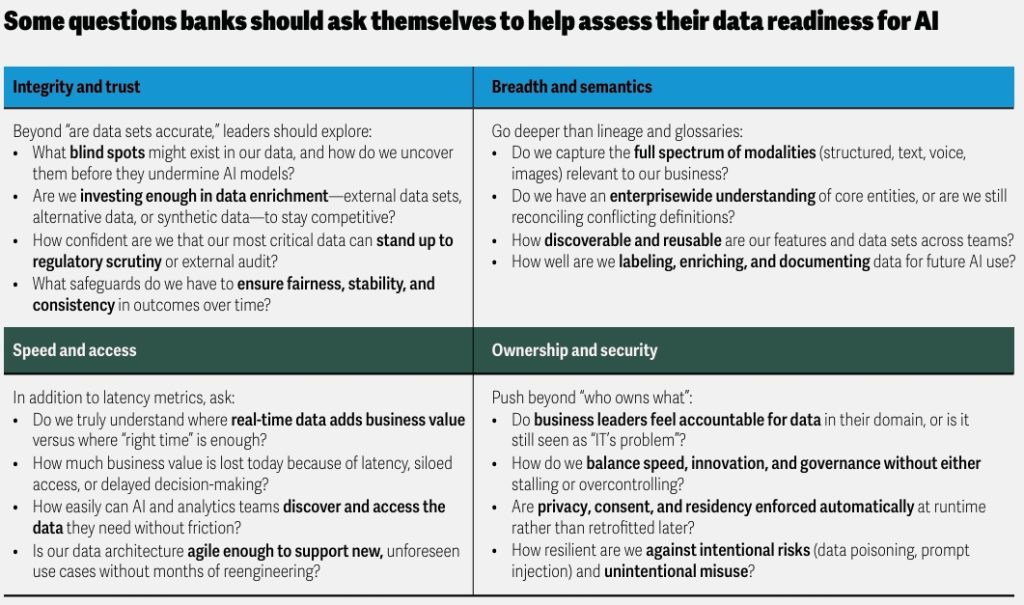

4. The Data Foundation: Why “AI-Ready” is Non-Negotiable

You cannot have AI without “AI-ready data.” The report dedicates significant focus to the four pillars of a modern data architecture: Integrity & Trust, Speed & Access, Breadth & Semantics, and Ownership & Security.

- The Warning: Poor infrastructure leads to data sprawl, bias, and stalled pilots. Shockingly, over 90% of data users in banks report that the data they need is often unavailable or takes too long to retrieve.

- The Prescription: Banks must assess their data readiness against these four pillars. This is not just an IT issue; it is a business leadership issue. The report suggests appointing the Chief Data Officer and Chief Risk Officer as joint data stewards to align risk appetite with data quality.

- The Feedback Loop: Interestingly, AI can be used to make data better. Banks can deploy “AI for data” agents—supervised anomaly detection models that flag data anomalies at ingestion points, auto-generate lineage graphs, and keep metadata current. This creates a virtuous cycle where AI improves the data that feeds AI.

Looking Forward: Defining the New Banking Playbook

The convergence of macroeconomic moderation, regulatory-driven innovation (stablecoins), and technological inflection (AI) means that standing still is a losing strategy.

Banks need to understand that financial transformation is not just about adopting new technology, but about rewiring the operating model to leverage it safely and profitably.

Part 3: Beyond the Premium for Defining Transformation in Insurance

According to Deloitte’s latest 2026 Global Insurance Outlook, the insurance sector is navigating a perfect storm. Economic uncertainty, the blurring of industry boundaries (particularly with private capital), rapidly evolving customer expectations, and the immense pressure to scale Artificial Intelligence (AI) are converging.

Here are the four key shifts defining the Insurance Outlook 2026 and what they mean for carriers ready to walk the talk.

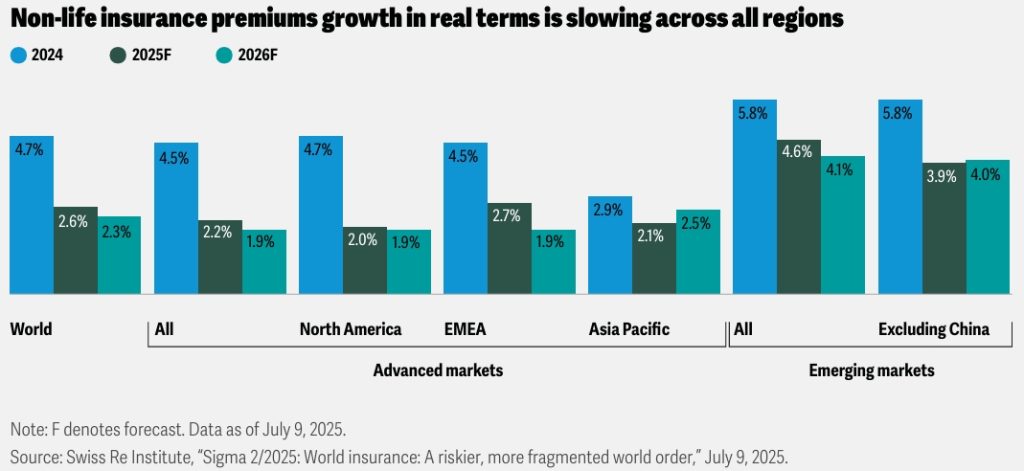

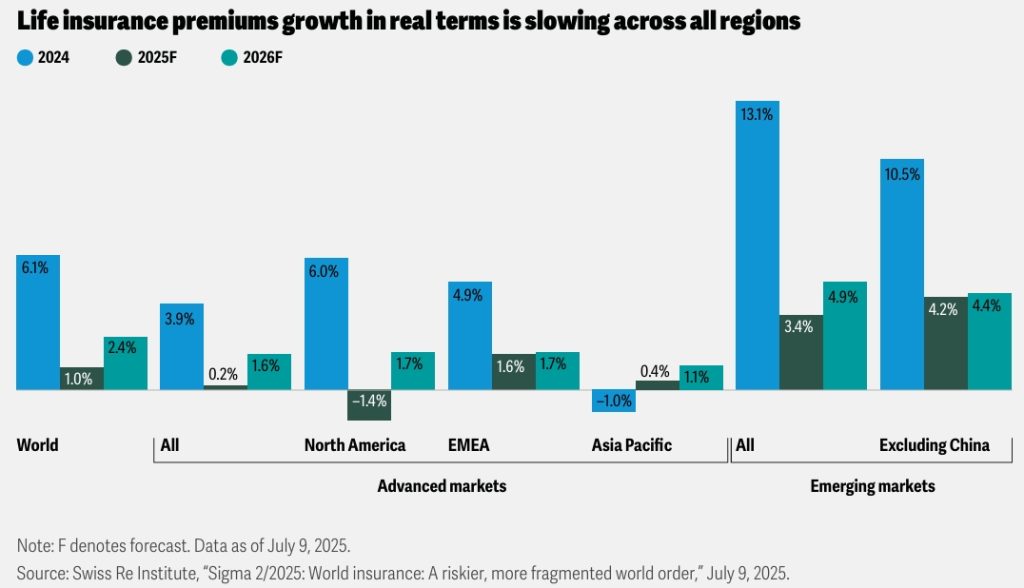

1. The Hard Market Eases, But the Pressure Intensifies

Globally, premium growth is expected to slow through 2026. In the US, the combined ratio—a key measure of underwriting performance—is forecast to worsen from 97.2% in 2024 to 99% in 2026.

- The Squeeze: While rate momentum diminishes, cost pressures from supply chain disruptions, labor shortages, and potential tariffs are mounting.

- The Divergence: Advanced markets in Europe are seeing a rebound in return on equity, but this is happening against a backdrop of fragmentation. Emerging markets face headwinds from a slowdown in China, which accounts for half of all emerging market premiums.

- The NeoForm View: In a flat growth environment, operational efficiency becomes the primary lever for profitability. Insurers must move beyond incremental cost-cutting to fundamental operating model transformation.

2. The Great Convergence: Insurance Meets Private Capital

Perhaps the most transformative trend in the Insurance Outlook 2026 is the accelerating convergence between life and annuity (L&A) carriers and private equity (PE) firms.

- The Appetite for Yield: Insurers’ managed assets in private credit expanded by 25% to $4.5 trillion in 2024. Private placements now account for 21.1% of total insurance AUM. A Goldman Sachs survey cited in the report found that 61% of CFOs and CIOs globally expect private credit to deliver the highest total returns over the next year.

- Strategic Alliances: This is not just about buying assets; it’s about buying capability. Partnerships like Lincoln Financial with Bain Capital, and Guardian Life with Janus Henderson, show insurers are seeking external investment expertise to optimize portfolios and free up capital.

- Regulatory Scrutiny: However, this shift brings complexity. Private credit is less liquid and transparent than public bonds. Regulators (NAIC, Bermuda Monetary Authority) are actively updating risk-based capital formulas to address this opacity.

- The NeoForm Perspective: For insurers, partnering with or being acquired by alternative asset managers is a double-edged sword. It unlocks higher returns but demands a new level of financial infrastructure—one capable of handling complex, illiquid assets with the same rigor as traditional portfolios, all while satisfying evolving regulatory demands for transparency.

3. The AI Reckoning: Data Plumbing Before AI Shine

The insurance industry is buzzing with AI pilots, but the report delivers a sobering reality check: You cannot have AI without AI-ready data.

- From Pilots to Scale: Fraud detection is a clear win—Deloitte estimates AI-driven fraud analytics could save P&C insurers up to $160 billion by 2032. Agentic AI is emerging, with AIG launching an AI underwriting assistant that handles submissions without adding staff.

- The Foundation Crisis: Despite the hype, many insurers struggle with “fragmented, messy data sprawl and outdated systems.” The report argues that “perfect data hygiene may not be essential,” but proper standardization is critical to avoid conflicting results.

- The Talent Friction: There is a growing disconnect between tech-savvy new graduates and insurers still stuck in pilot mode. Mid-career professionals need to become AI-literate, yet only 25% of insurance executives have taken tangible action to elevate human skills alongside machine capabilities.

4. The Human-AI Partnership: Empathy as a Differentiator

Insurance is ultimately about protecting people in their most vulnerable moments—a house fire, a death in the family, a serious diagnosis. In these moments, customers seek empathy, not just efficiency.

- Right-Channeling: Insurers are adopting “right-channeling” strategies—using rules-based systems to steer customers to the most effective service channel (digital self-service for simple queries, human agents for complex claims).

- Empathy Meets Efficiency: The report highlights Cigna linking frontline compensation to customer experience metrics, aligning incentives with service excellence. Technology is augmenting advisors with real-time quoting and AI-driven suggestions, freeing them to build deeper relationships.

- The NeoForm Takeaway: The future of insurance is not automated or human; it is collaborative. The winning carriers will be those that design workflows where humans and AI collaborate meaningfully, sharing the value created through that partnership.

Looking Forward: Walking the Talk in 2026

The Insurance Outlook 2026 makes one thing clear: The industry’s evolution is no longer a series of incremental steps. It is a decisive shift. Emerging risks, disruptive technology, and the convergence with private capital are forcing a fundamental rethink of the business model.

For insurers, the path forward requires:

- Modernizing the core: Investing in data foundations and flexible architectures.

- Transforming the workforce: Bridging the gap between legacy expertise and digital fluency.

- Forging strategic partnerships: Collaborating with tech providers and alternative asset managers to access new capabilities.

- Prioritizing customer-centricity: Integrating digital and human touchpoints seamlessly.

As NeoForm Partners knows well, transformation is not about adopting the latest shiny technology. It is about rewiring the operating model to ensure that technology, talent, and capital work in concert. The future of insurance is here. The only question is: Are you ready to walk the talk?

The NeoForm Perspective: A Final Thought

Across all these financial services industries, one theme resonates most deeply with NeoForm’s mission: The gap between bold, well-governed execution and cautious incrementalism is widening.

The firms that thrive in 2026 will not be those with the biggest budgets or the most aggressive AI pilots. They will be those that:

- Fix the foundations—modernizing core systems and data architecture before adding new technology layers

- Embrace convergence—building operational models capable of handling hybrid products and cross-sector partnerships

- Rethink talent—designing workflows where humans and AI collaborate meaningfully

- Navigate regulation strategically—turning compliance into competitive advantage

As Deloitte makes clear, the boundaries that once defined financial services—public vs. private, active vs. passive, banking vs. insurance—are dissolving. In their place emerges a more fluid, interconnected landscape where success belongs to those who can transform their operating models as quickly as the markets evolve.

🔗 Links for More:

Read and download the full reports on Deloitte website or from NeoForm LinkedIn page (Investment, Banking, Insurance).

📌 About NeoForm:

At NeoForm Business Partners, we partner with financial institutions and FinTechs for financial transformation through financial agility and efficiency to build these very capabilities and elevate financial performance.

Visit our blog for more insights on financial services industries and financial solutions in private markets.

🔗 Related Readings:

- Global Wealth Management Report 2025: Rethinking the Playbook

- Global Banking Review 2025: McKinsey Insights on Winning Strategies

- Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment

- How Private Markets Are Redefining Corporate & Investment Banking – BCG 2025

- The Next Big Arenas of Competition: 18 Super High Growth Sectors Shaping the Future Economy

Need tailored solutions? Explore NEO Services or contact our partners to learn how our strategic and technology solutions can help you build a more resilient and efficient growth in financial services industries.