CIB in Transition: How Private Markets Are Driving the Next Wave of Corporate & Investment Banking Growth

The corporate and investment banking (CIB) landscape is no longer what it was even five years ago.

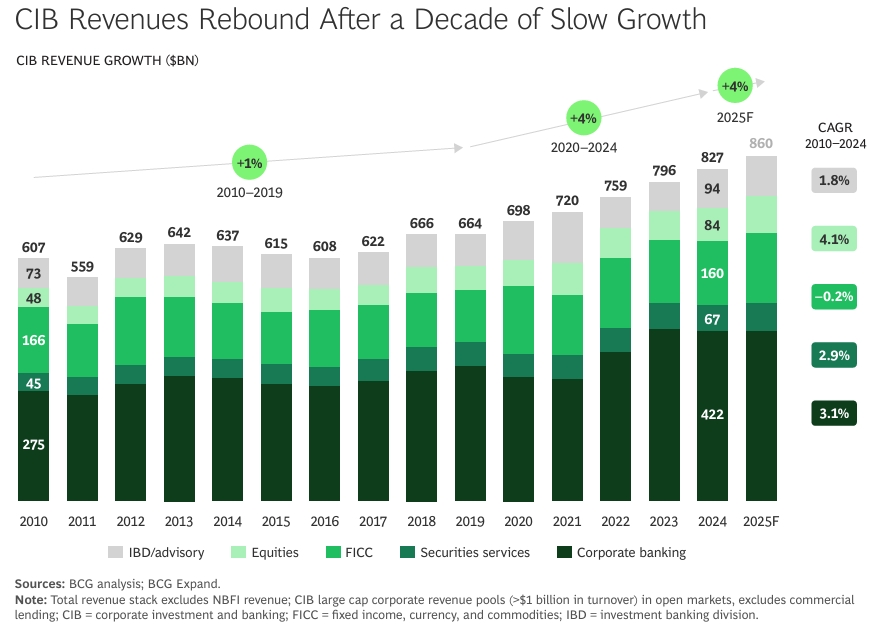

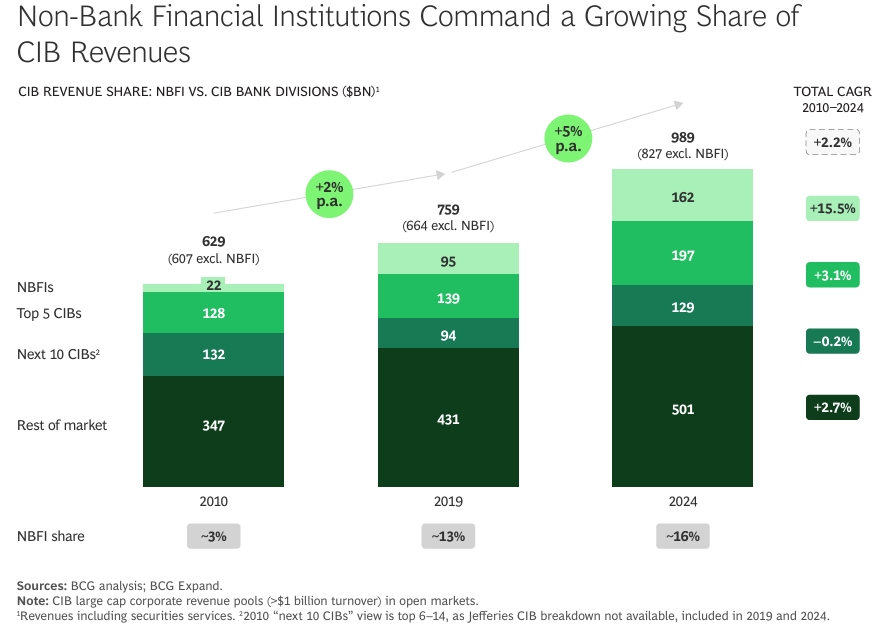

While headlines celebrate a sector rebound—global CIB revenues grew 4% in 2024, reaching $827 billion—a deeper look reveals structural change accelerating beneath the surface.

Private capital is no longer on the sidelines. Non-bank financial institutions (NBFIs) now account for over 15% of global CIB revenues, up from less than 5% in 2010. AI is moving from experimentation to core workflow redesign. Tokenization and digital assets are gaining institutional traction. Geopolitical shifts are redrawing capital and trade flows.

For leaders in private markets and financial transformation, this isn’t just noise—it’s opportunity.

BCG’s Corporate and Investment Banking Report 2025 provides a clear-eyed view of where value is moving, and what firms must do to capture it. Here’s what you need to know.

The New Architects of Capital: NBFIs and Private Markets

One of the most striking shifts is the rising influence of non-banks and private capital providers.

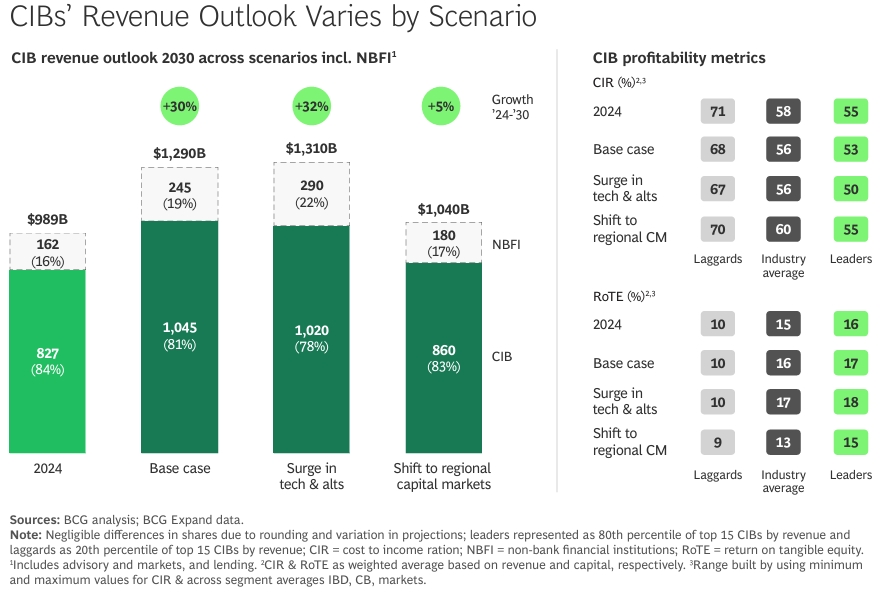

By 2030, NBFIs are projected to account for 22% of total CIB revenue pools—and a staggering 30% of trading revenues.

Why? Agility, specialization, and freedom from traditional regulatory capital constraints allow them to move into spaces where banks retreat. Private credit funds now make up 11% of global lending, expanding into asset-based finance, NAV facilities, and warehouse platforms.

For private market players: This isn’t just growth—it’s market redefinition. Your role in capital formation, deal sourcing, and structured finance is becoming central, not complementary.

AI Beyond Pilots: From Efficiency to Transformation

AI in CIB has evolved. What began with risk modeling and chatbots is now transforming front-to-back workflows.

BCG estimates that by 2030, AI could free up 25–40% of banker capacity and boost operations productivity by 20–35%.

Leading firms are no longer experimenting in silos. They’re launching CEO-backed transformation programs anchored in four to six high-impact initiatives—client meeting prep, pitchbook automation, credit underwriting—with clear P&L ownership.

Transformation takeaway: AI isn’t an IT project. It’s a strategic lever to deepen client relationships, accelerate execution, and reshape cost structures.

Digital Assets Move to the Core

After years of speculation, institutional adoption of digital assets is accelerating.

Stablecoins alone are expected to reach $3 trillion in market cap by 2030, moving from fringe experiments to core market infrastructure.

Tokenization is gaining momentum in repo transactions, collateral management, and structured products—enabling new levels of automation, traceability, and fractional ownership.

For forward-looking firms: The question is no longer if but how to build token-native capabilities into custody, settlement, and liquidity management.

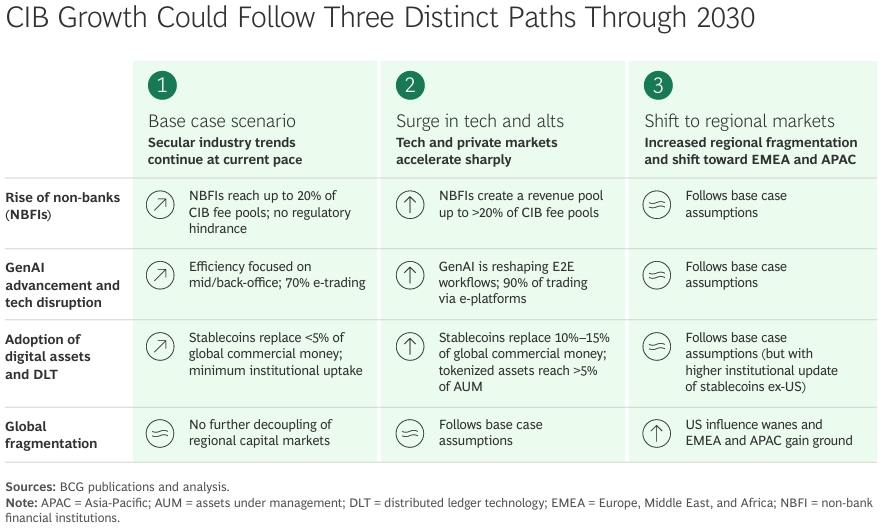

Three Scenarios for Corporate & Investment Banking in 2030

BCG outlines three plausible pathways for the coming decade:

- Base Case – Steady growth (~4% annually), with NBFIs nearing 20% of revenues.

- Tech & Alternatives Surge – Accelerated AI and private capital expansion, widening the performance gap between leaders and laggards.

- Regional Fragmentation – Geopolitical shifts drive capital markets regionalization, favoring local champions.

In all scenarios, corporate banking faces the greatest disruption, while FICC and equities stand to benefit most from digitization and NBFI expansion.

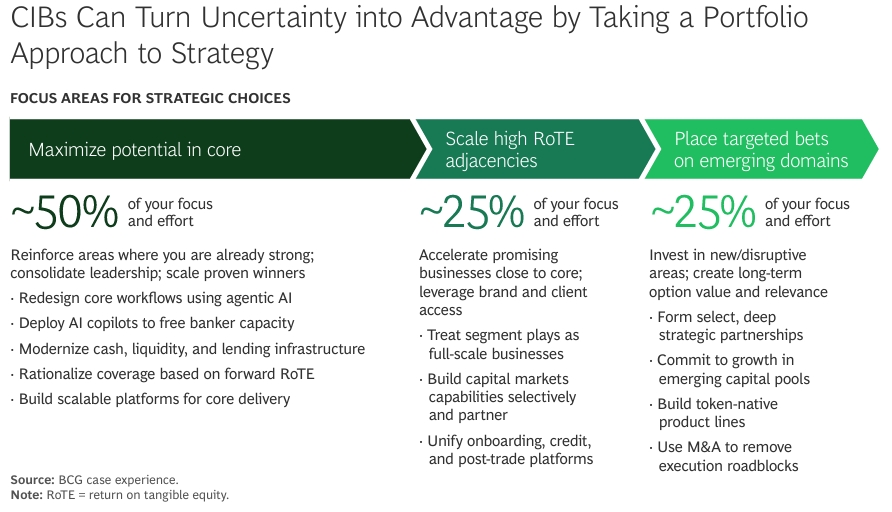

A Portfolio Strategy for Uncertain Times

To navigate these shifts, BCG recommends a portfolio-based approach to strategy:

- 50% of effort: Maximize the core

Redesign workflows with AI, modernize treasury platforms, rationalize coverage based on forward RoTE. - 25% of effort: Scale high-ROTE adjacencies

Treat segments like sponsor finance or cross-border transaction banking as standalone growth engines. - 25% of effort: Place targeted bets in emerging domains

Build token-native product lines, form deep infrastructure partnerships, commit to emerging capital pools.

Firms that double down on strengths while strategically investing in new capabilities will be best positioned to capture growth—regardless of which future unfolds.

The Bottom Line for Private Market Leaders

The CIB industry is at an inflection point. Value is migrating toward private capital, technology-enabled efficiency, and digital asset innovation.

For transformational finance partners, this presents a clear mandate:

Help clients rethink coverage models, embed AI at scale, and build bridges between traditional and tokenized finance.

The gap between leaders and laggards will widen. The time to choose your role is now.

🔗 Links for More:

Read and download the full report “Corporate and Investment Banking Report 2025: Positioning for Growth in Uncertain Times” on BCG website or from NeoForm LinkedIn page.

📌 About NeoForm:

At NeoForm Business Partners, we partner with financial institutions and FinTechs for financial transformation through financial agility and efficiency to build these very capabilities and elevate financial performance.

Visit our blog for more insights on financial services industries, investment management and private markets.

🔗 Related Readings:

- Global Wealth Management Report 2025: Rethinking the Playbook

- Global Banking Review 2025: McKinsey Insights on Winning Strategies

- Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment

- The Next Big Arenas of Competition: 18 Super High Growth Sectors Shaping the Future Economy

- McKinsey Global Private Markets Report 2025

Need tailored solutions? Explore NEO Services or contact our partners to learn how our strategic and technology solutions can help you build a more resilient and efficient growth.

1 Comment

How Non-Banks Are Disrupting CIB: Asia Leads Private Credit & Bank Strategy Shift – Investment Banking Updates

[…] 12 2025 [2] http://www.ft.com (Financial Times) — Dec 16 2025 [3] http://www.imf.org (IMF) — Oct 14 2025 [4] neoform.partners (NeoForm Business Partners / BCG) — Oct 2025 [5] http://www.bcg.com (BCG) — Oct 14 2025 [6] […]