How Markets Can Turn Geopolitical Trade Shifts into Strategic Advantage

For the better part of three decades, the global playbook for supply chains was simple: find the lowest-cost location, centralize production, and push just-in-time efficiency to its absolute limit. That era is not just ending—it has already been replaced by something far more complex, volatile, and geopolitically charged.

If you are a CFO, a finance transformation leader, or an executive in private markets—managing a portfolio company or a mid-cap industrial firm—you have likely felt this shift as a persistent, grinding uncertainty. Tariffs appear overnight. Critical components get held at borders. Entire trade corridors that once felt reliable suddenly look exposed.

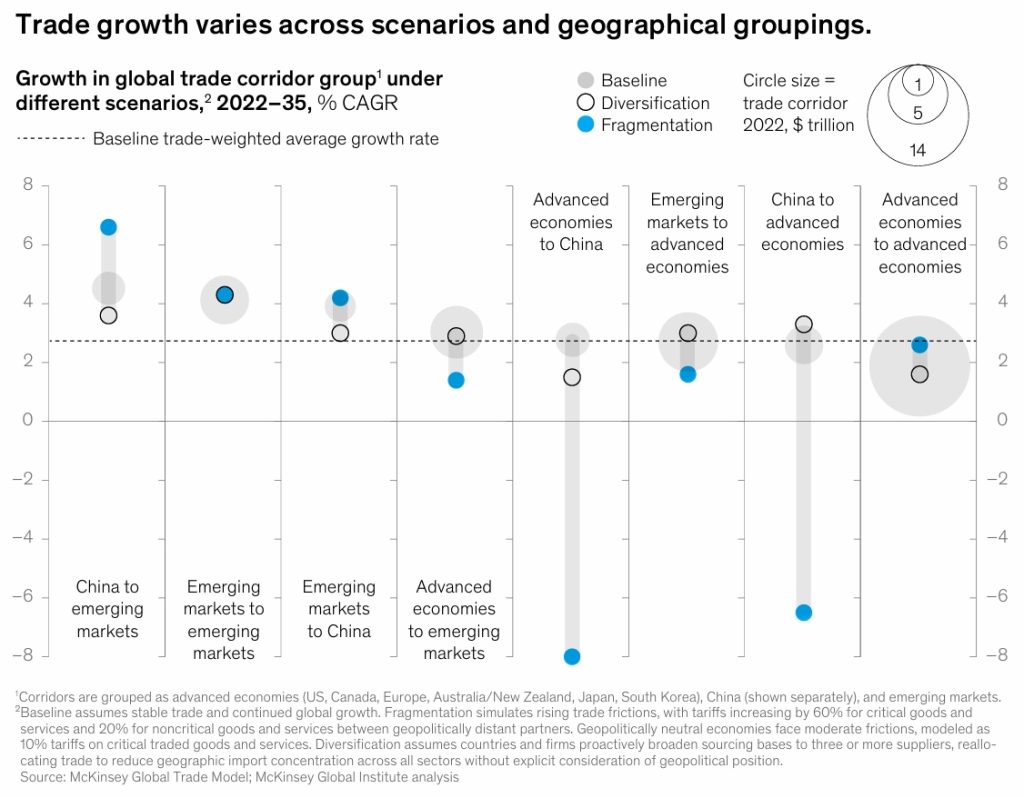

According to a comprehensive analysis from McKinsey & Company (A new trade paradigm: How shifts in trade corridors could affect business, May 2025), the global trade system is undergoing a structural reconfiguration unlike anything seen in recent memory. By 2035, over 30 percent of global trade—representing up to $14 trillion in value—could swing from one trade corridor to another depending on how geopolitical tensions, tariff policies, and diversification strategies unfold.

For NeoForm Business Partners, which specializes in transformational finance in private markets, this is not merely a logistics problem. It is a financial transformation imperative. The way capital is allocated, how working capital is managed, where manufacturing footprints are located, and how risk is priced into long-term contracts—all of these are being rewritten by the tectonic shifts in trade.

This blog post distills the McKinsey report into actionable insights. We will explore the three most likely trade scenarios, identify which corridors are safe bets versus uncertain bets, and—most importantly—provide a practical framework for finance leaders to drive supply chain transformation as a source of resilience and value creation.

The End of the Efficiency-Only Paradigm

Let us start with a candid observation. Most portfolio companies and mid-market firms have optimized their supply chains for a world that no longer exists. That world assumed stable geopolitical relations, low friction cross-border data flows, and tariffs as an exception rather than a rule. That world is gone!

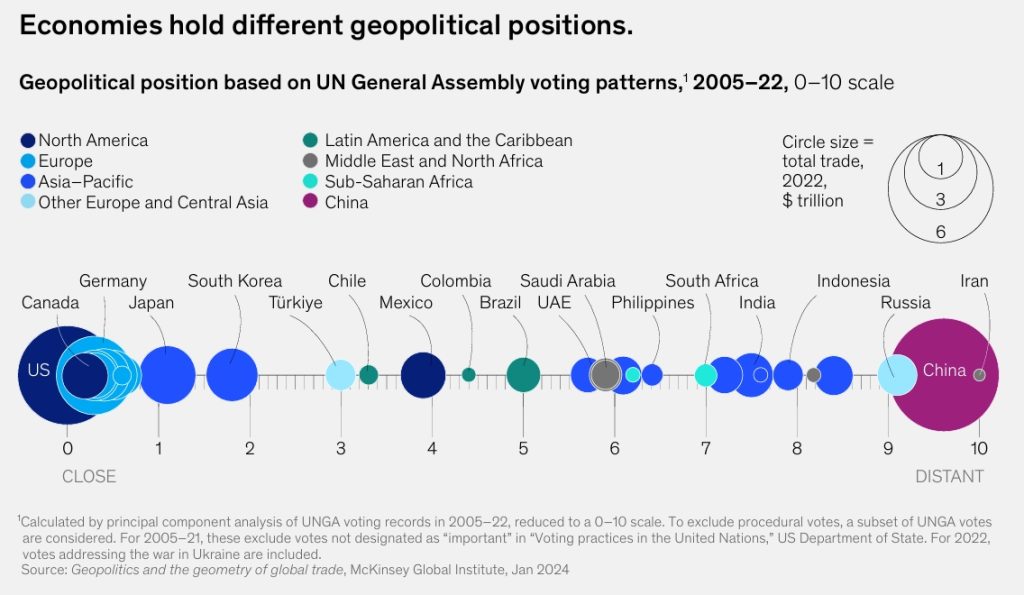

Since 2017, economies have consistently traded less with geopolitically distant partners. The COVID-19 pandemic exposed concentration risks. The war in Ukraine weaponized energy and food supply chains.

And as of 2025, multiple rounds of tariff changes and trade disputes have triggered sharp declines in once-dominant corridors—for example, Chinese customs data recently reported an 18 percent year-on-year drop in imports and a 35 percent decline in exports between the US and China.

And 2026 has started with US invasion to Venezuela and US-Israel war invasion to Iran that the later led to one of greatest energy and trade crises in the world through Persian Gulf and Strait of Hormuz.

But here is what makes this moment different from previous disruptions: the inertia of trade patterns is colliding with deliberate policy choices. Industrial policy is back. World superpowers are using tariffs as strategic tools. And businesses can no longer assume that the cheapest supplier today will be accessible tomorrow.

For finance leaders, this translates directly into balance sheet questions. How much inventory should we carry as a buffer? Which trade receivables are now riskier? What is the cost of capital for a factory located in a geopolitically exposed region? These are not operational details—they are strategic financial decisions.

Three Scenarios for Supply Chain Transformation Toward 2035

The McKinsey analysis models three distinct futures for global trade, each with dramatically different implications for supply chain transformation. Understanding these scenarios is the first step in building a robust financial strategy.

Scenario 1: Baseline – Steady as She Goes

In the baseline scenario, global trade continues to grow according to economic fundamentals. No meaningful new trade barriers are erected relative to recent historical levels. Global GDP grows at an average of 2.7 percent annually through 2035, with China at 3.6 percent and the US at 1.7 percent.

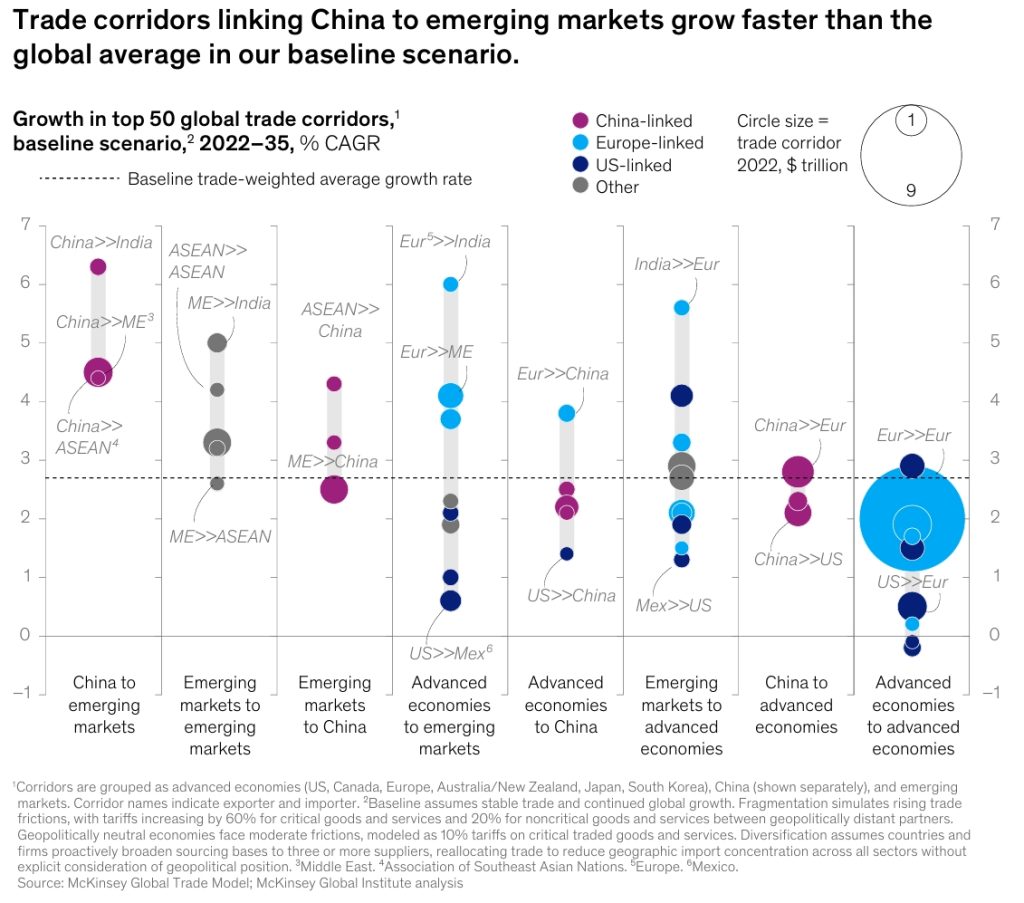

In this world, global trade of goods, services, and resources grows by approximately $12 trillion in real terms to reach $45 trillion by 2035, up from $33 trillion in 2024. Trade corridors connecting emerging markets with each other and with China grow at 4 to 5 percent annually, outpacing the global average.

The baseline scenario represents a continuation of current trends, albeit with moderate growth. The challenge here is not survival but opportunity capture—specifically, which corridors are expanding fastest and how to position capital accordingly.

Scenario 2: Fragmentation – The Geopolitical Ice Age

This is the scenario that keeps CFOs awake at night. In a fragmentation scenario, trade relationships deteriorate sharply. Tariffs on most goods rise to 10 percent globally, while tariffs on critical goods traded between advanced economies and China or Russia rise by up to 60 percent.

The results are stark. Approximately $3 trillion of the potential $12 trillion in trade growth is simply lost. Trade between China and advanced economies drops significantly, while trade among advanced economies (Europe-US, Europe-Japan) speeds up as countries turn to geopolitically closer partners.

Most notably, trade between China and emerging economies proves resilient and actually grows faster under fragmentation than under the baseline, as China aggressively seeks new partners. Corridors like China-ASEAN (Association of Southeast Asian Nations) and China-Middle East accelerate.

For private markets, fragmentation means bifurcation. Some corridors become highly profitable but politically sensitive. Others shrink dramatically. The cost of capital rises for exposed regions. And supply chain transformation becomes a defensive necessity.

Scenario 3: Diversification – The Resilience Pivot

In the diversification scenario, businesses and countries proactively broaden their sourcing bases to reduce concentration. The goal is to ensure that no product has an import concentration so high that 90 percent comes from just three or fewer economies.

Interestingly, this scenario does not necessarily benefit all emerging markets equally. As McKinsey points out: “Conventional wisdom suggests that emerging markets would benefit from a diversification scenario, but our model shows that this isn’t necessarily the case. As countries diversify, they often turn to the next-best suppliers. Emerging markets already integrated into these networks stand to gain, but those outside remain on the sidelines.”

About $1 trillion of potential trade growth is foregone in this scenario compared to baseline. However, the trade that remains is more resilient, less concentrated, and arguably more sustainable.

For finance leaders, diversification presents both a challenge and an opportunity. The challenge is the near-term cost of requalifying suppliers, renegotiating contracts, and potentially holding more inventory. The opportunity is reduced exposure to single-point failures and the ability to price resilience into customer relationships.

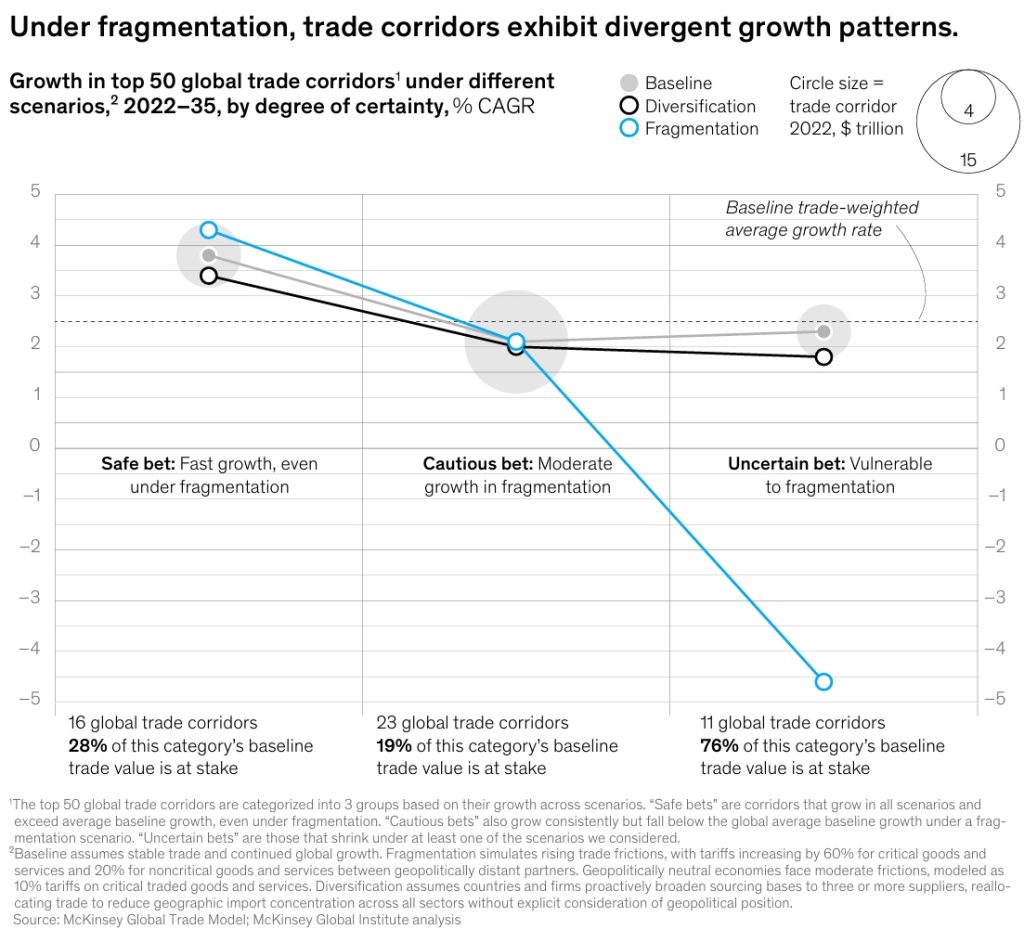

The Corridors That Matter: Safe Bets, Cautious Bets, and Uncertain Bets

One of the most valuable contributions of the McKinsey analysis is its granular breakdown of trade corridors. Of the 50 largest trade corridors today, the report identifies three distinct categories based on how they perform across the three scenarios.

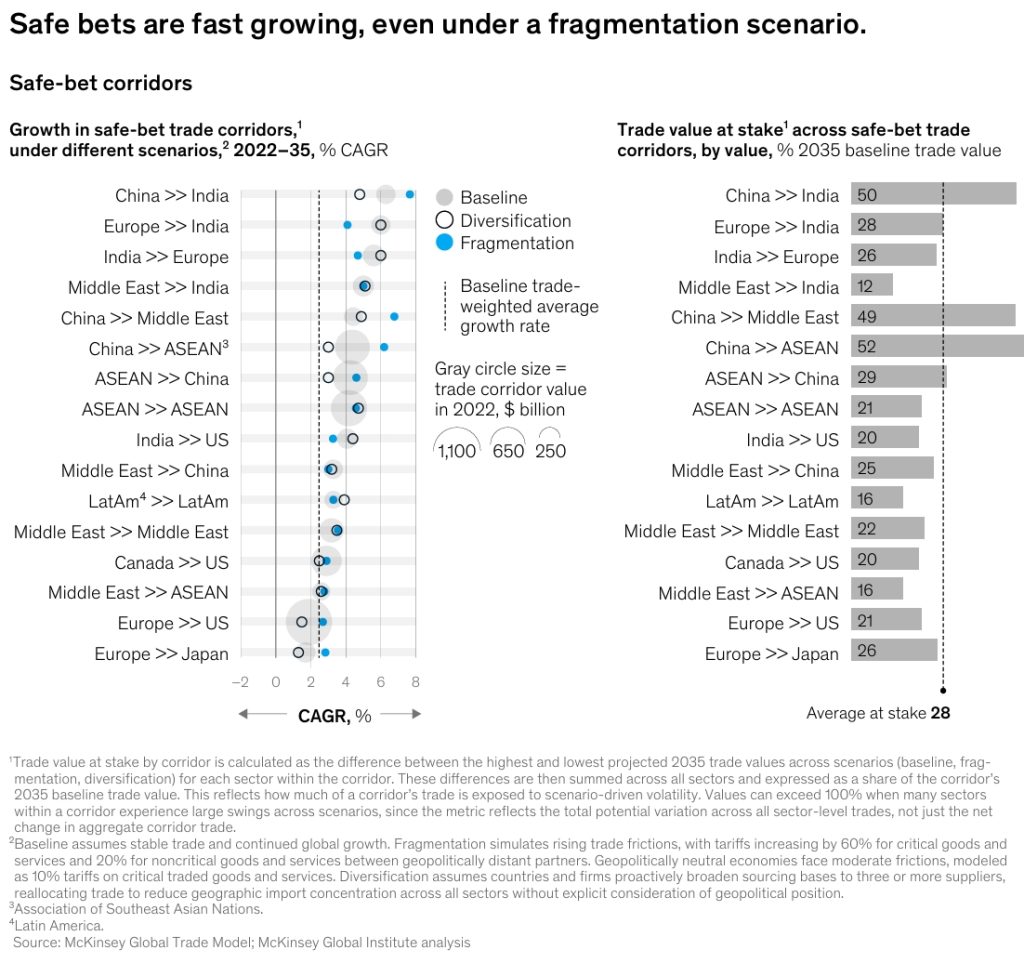

Safe Bets: Resilient Growth No Matter What

Sixteen corridors emerge as “safe bets”—they grow in all scenarios and exceed average baseline growth even under fragmentation. These corridors deserve strategic attention and capital allocation.

India-connected corridors feature prominently: India-European Union, India-United States, Middle East-India, and China-India. India’s rapid economic growth drives expansion across multiple trade routes, both as an exporter to advanced economies and as an importer of machinery, energy, and intermediate goods.

China-emerging economy corridors also qualify as safe bets: China-ASEAN, China-Middle East, and China-Africa. Under fragmentation, China shifts exports away from advanced economies and deepens ties with emerging markets. For example, ASEAN is already becoming China’s largest trading partner, integrating into Chinese value chains in electronics and textiles.

Intra-emerging market corridors—within ASEAN, within Latin America, and within the Middle East—also show above-average growth in all scenarios. Regional integration initiatives like the Regional Comprehensive Economic Partnership (RCEP) are laying the groundwork for increased trade flows.

Finance implication: For portfolio companies with exposure to these corridors, the strategic question is not whether to invest but how fast to scale. You need to prioritize working capital optimization, trade finance facilities, and local currency hedging.

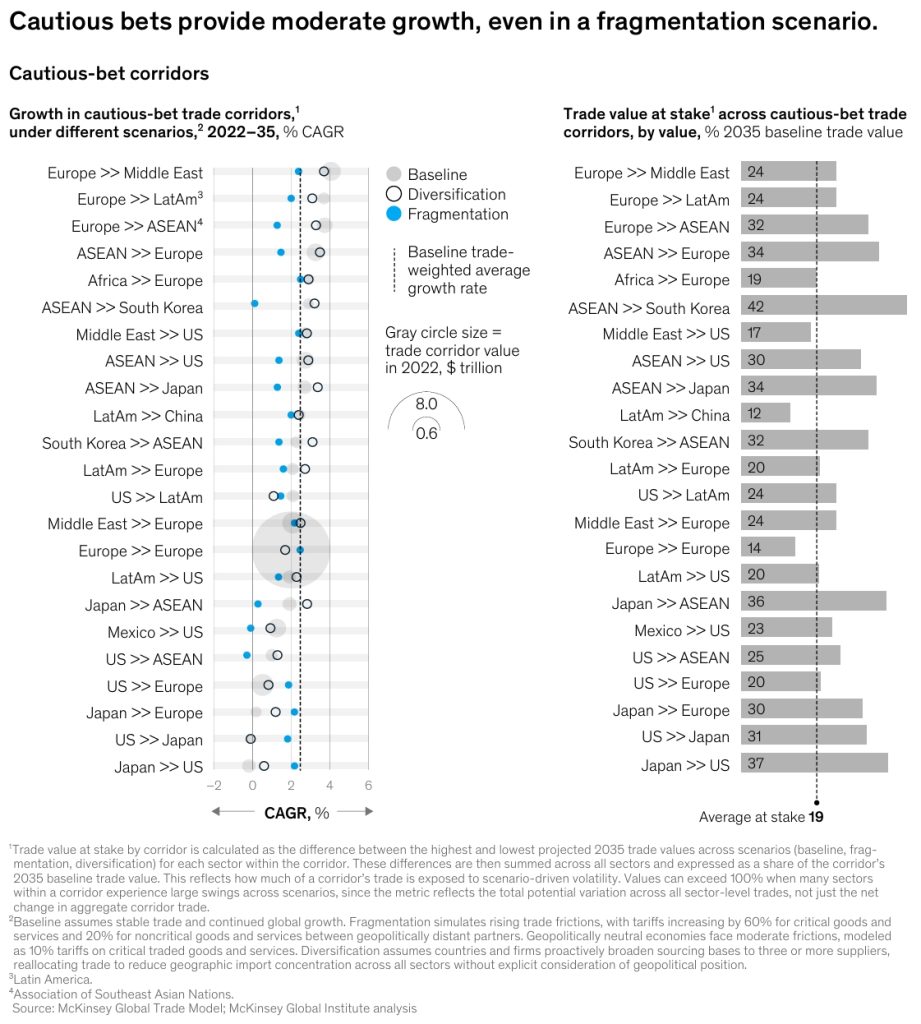

Cautious Bets: Positive but Slower Growth

Twenty-three corridors fall into the “cautious bets” category. They grow in all scenarios, but under fragmentation, their growth lags behind the global baseline average. These include corridors like Europe-Middle East, Europe-Latin America, Europe-Africa, and advanced Asia-ASEAN.

These corridors often involve complementary endowments—advanced economies exporting pharmaceuticals and transport equipment while emerging markets export textiles, electronics, energy, or metals. However, under fragmentation, slower growth in emerging economies creates a drag. Additionally, as China redirects exports toward emerging markets at lower prices, local producers in cautious-bet corridors face competitive pressure.

Finance implication: In cautious-bet corridors, the priority is selectivity. Not all products or partnerships will perform equally. Finance leaders should segment their exposures, stress-test margins under slower growth assumptions, and maintain flexibility in supplier contracts.

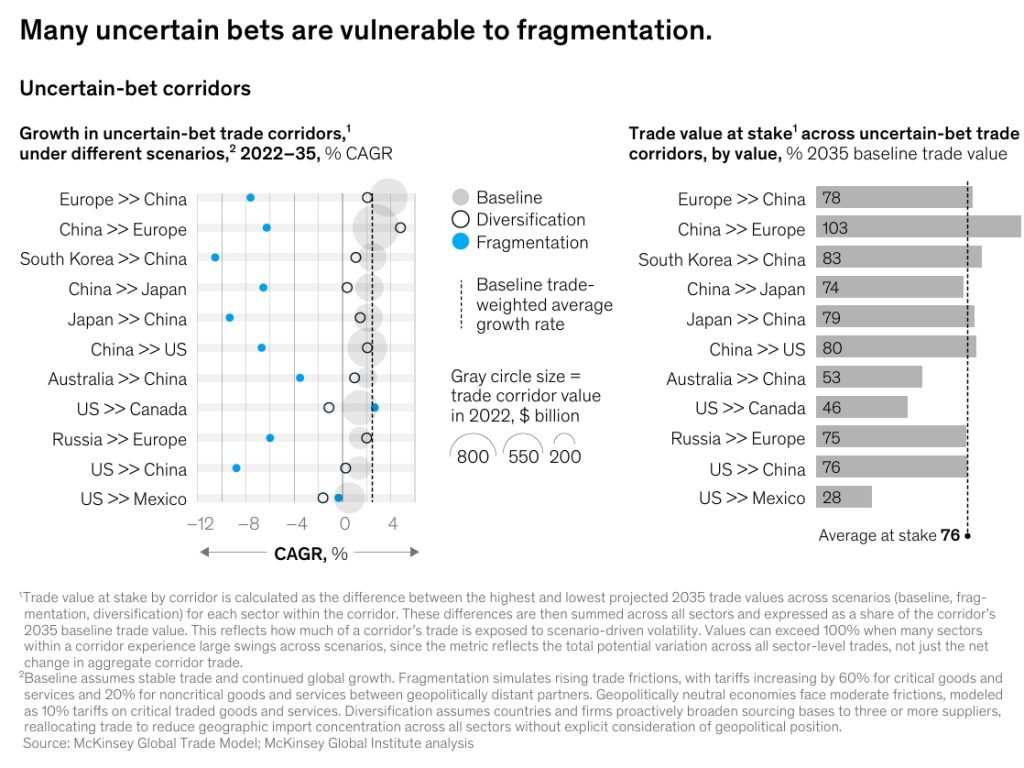

Uncertain Bets: High Risk, High Exposure

Eleven corridors are classified as “uncertain bets”—they shrink materially in at least one scenario. Nine of these connect geopolitically distant economies with advanced economies. Under fragmentation, these corridors shrink by an average of 5.8 percent per year, compared with 2.3 percent growth in the baseline.

The most vulnerable corridors involve trade between China and Russia and advanced economies. For critical goods and services, these corridors fall from a 15 percent share of global trade today to just 2 percent by 2035 in a fragmentation scenario.

Two other uncertain-bet corridors involve Canada-US and Mexico-US trade. These are not vulnerable to fragmentation but to diversification—the US already accounts for 80 to 90 percent of Canadian and Mexican manufactured exports, making them highly concentrated and thus exposed if the US actively seeks alternative suppliers.

Finance implication: For firms with significant exposure to uncertain-bet corridors, supply chain transformation is an urgent necessity. This may involve dual sourcing, nearshoring, or entirely reconfiguring production footprints. From a finance perspective, these firms should model accelerated depreciation of assets in exposed regions, increase reserve allocations for trade disruption, and potentially divest non-core exposed operations.

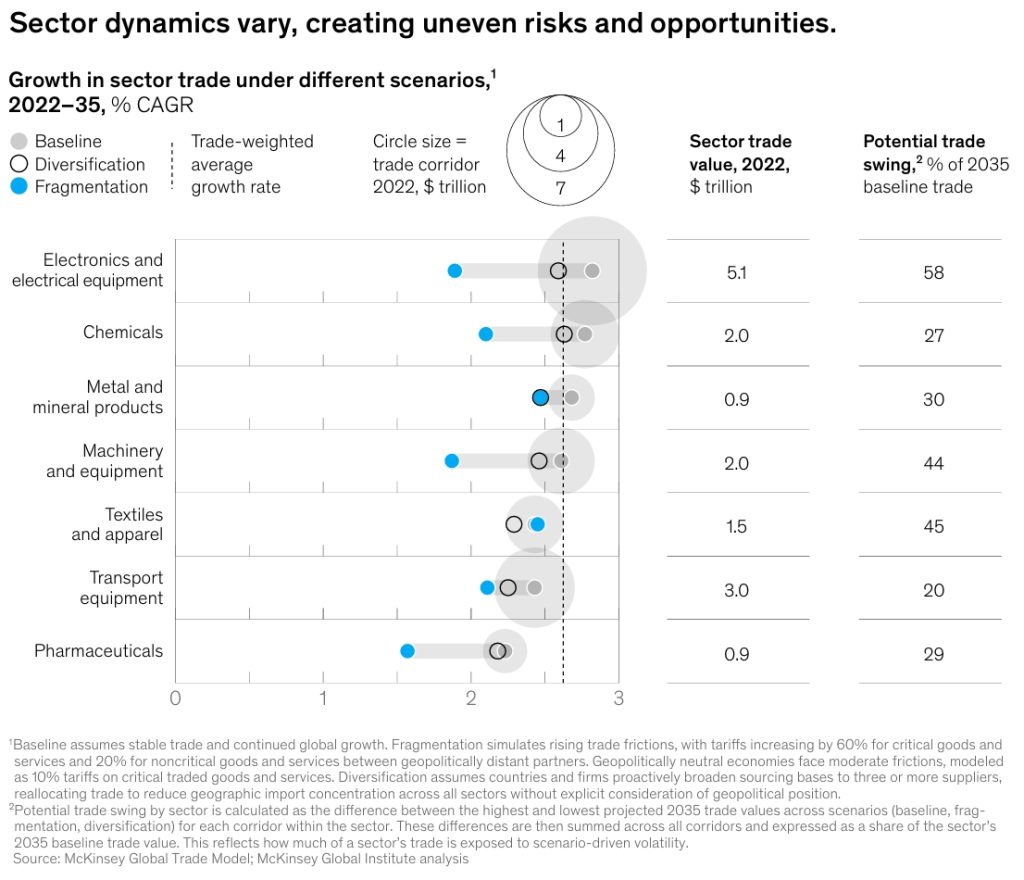

Sector Deep Dive: Where the Swings Are Largest

Not all sectors are created equal. The McKinsey analysis reveals dramatic differences in exposure across manufacturing, resources, and services.

Electronics: The Most Exposed Sector

Fully 58 percent of future baseline trade value in electronics is exposed to shifts in global trade dynamics. Three factors drive this vulnerability:

First, 22 percent of electronics trade occurs between geopolitically distant partners—well above the 12 percent global average. Second, critical subsectors like semiconductors and electrical equipment face significantly higher tariffs in a fragmentation scenario. Third, the sector is highly concentrated, with China alone accounting for approximately 75 percent of global laptop exports.

For private market firms in or adjacent to electronics, this means that supply chain transformation cannot be incremental. It requires scenario-based redesign.

Textiles and Machinery: Also Highly Exposed

Textiles and machinery follow closely behind electronics in terms of potential trade swings. These manufacturing value chains similarly bridge geopolitically distant economies, making them susceptible to fragmentation. Diversification efforts would have pronounced impacts, particularly in concentrated subsectors like electrical machinery, where the top three exporters account for about half of global exports.

Pharmaceuticals and Transport Equipment: More Resilient

In contrast, pharmaceuticals and transport equipment have lower value exposed to shifts. Most pharmaceutical trade occurs between geopolitically close advanced economies—Europe, Japan, and the United States. Similarly, transport equipment has strong intraregional trade within Europe and North America.

However, as the McKinsey report cautions, the model may underestimate real-world disruption because it does not fully capture cascading impacts from small but critical components. The 2022 shortages of semiconductors and wiring harnesses that forced automakers to halt production are a powerful reminder.

Resources: Concentration Is Costly

In energy, mining, and agriculture, the story is about concentration—both global and local.

Mining is globally concentrated. The top three producers account for over 70 percent of lithium, 80 percent of nickel, and over 90 percent of cobalt. Refining is even more concentrated, with China holding 70 percent of lithium refining capacity. Development timelines of a decade or more make rapid diversification challenging.

Energy (oil and gas) is more distributed but locally concentrated. Korea and Japan import over 75 percent of their oil from the Middle East and have optimized refineries for those specific grades. Shifting away would be costly.

Agriculture is similarly locally concentrated. While many products have multiple potential suppliers, countries often rely on nearby partners for logistical and perishability reasons. The war in Ukraine demonstrated how quickly agricultural prices can surge—20 to 50 percent for key commodities before gradually returning to prewar levels.

Finance implication: For firms reliant on concentrated resources, the priority is vertical integration or long-term offtake agreements that lock in supply. Financial transformation here means moving from transactional procurement to strategic partnership models, potentially including direct investment in upstream assets.

Beyond Goods: Services and Intangibles

It would be a mistake to focus only on physical goods. As McKinsey notes, flows of intellectual property (IP) and services grew about twice as fast as goods trade between 2010 and 2019. Data flows grew at almost 50 percent per year.

These intangible flows are often interlinked with goods trade. A US chip-design company licensing its architecture to an Asian foundry generates IP and services flows westward while goods flow eastward.

In a fragmentation scenario, however, intangible flows face high barriers—not tariffs, but regulatory restrictions, licensing requirements, data localization rules, and lack of mutual recognition of credentials. For professional services firms, technology companies, and financial institutions, this could be as disruptive as any goods tariff.

For private markets, this suggests that supply chain transformation must encompass not just physical supply chains but also data supply chains, IP licensing structures, and service delivery models.

A Five-Question Framework for Finance Leaders

Knowing the scenarios and sector dynamics is necessary but not sufficient. The real value lies in action. Drawing from the McKinsey report and NeoForm’s expertise in transformational finance, here is a five-question framework to guide your supply chain transformation efforts.

1. What is the mid- to long-term impact on your current business due to trade shifts across corridors?

This is a diagnostic question. Map your revenue, cost of goods sold, and working capital by trade corridor. Which corridors are growing or shrinking? Which are exposed to fragmentation, and which to diversification?

Finance action: Build a scenario-based financial model that quantifies EBITDA, free cash flow, and return on invested capital (ROIC) under baseline, fragmentation, and diversification for your most important corridors.

2. Which trade corridors will become more important for your business, and which will become lower priorities?

Not all corridors deserve equal attention. Based on the McKinsey categorization, identify whether your key corridors are safe bets, cautious bets, or uncertain bets. Allocate strategic attention accordingly.

Finance action: For safe-bet corridors, consider increasing working capital lines or trade finance limits. For uncertain-bet corridors, develop contingency plans including alternative suppliers, inventory buffers, or nearshoring options.

3. What is the value creation potential of these important trade corridors over the mid- to long-term?

This is where transformation meets value. Diversifying a supply chain has costs—requalifying suppliers, requalifying products, potentially higher unit costs. But it also has benefits: reduced disruption risk, pricing power, and potentially faster time-to-market for new products.

Finance action: Calculate the “resilience premium”—the additional gross margin or reduced volatility that justifies diversification costs. Use real options valuation to compare the flexibility value of diversified supply chains against the cost savings of concentrated ones.

4. How is your business positioned today to capture this value?

Honest assessment is critical. Do you have the procurement team, the supplier relationships, the data infrastructure, and the balance sheet capacity to execute a supply chain transformation?

Finance action: Conduct a capability audit. If gaps exist, consider whether to build internally, partner with specialists, or acquire complementary capabilities. In private markets, this often favors buy-and-build strategies.

5. What strategic and organizational changes are needed to support your action plans?

Supply chain transformation is not a project; it is a new operating model. It requires changes in incentive systems, performance metrics, and decision rights. The CFO and finance team must be at the table, not just signing off after the fact.

Finance action: Establish a cross-functional “trade corridor council” including finance, procurement, operations, and sales. Redefine KPIs to include supply chain resilience metrics alongside traditional cost and efficiency measures.

A Real-World Example: Micron’s Bold Move in India

The McKinsey report offers a compelling case study: Micron, the US-based semiconductor company. Semiconductors are among the most geopolitically exposed industries. Rather than waiting for clarity, Micron acted decisively.

When the Indian government invited investment, Micron committed several billion dollars to build an ASTM-certified facility in India—a country where semiconductor fabs were largely unknown. The new fab was geopolitically nearer than alternatives and allowed Micron to tap nascent domestic demand expected to double from roughly $50 billion to $100 billion by 2030.

Because Micron moved early, the Indian government recognized its first-mover status with a substantial 70 percent capital subsidy for the new project.

The lesson for private markets: Speed and commitment in supply chain transformation can create asymmetric advantages. Waiting for certainty is itself a risky strategy.

The NeoForm Perspective: Finance as the Enabler of Transformation

At NeoForm Business Partners, we specialize in transformational finance in private markets. We see firsthand how portfolio companies and mid-cap firms struggle to translate geopolitical insights into financial action.

The traditional finance function—focused on reporting, compliance, and periodic planning—is not equipped for this environment. What is needed is a finance function that can:

- Model scenarios dynamically, not just annual budgets.

- Allocate capital flexibly, with the ability to pivot as trade corridors shift.

- Structure trade finance and hedging instruments that reflect corridor-specific risks.

- Partner with operations and procurement to redesign supplier networks.

- Communicate resilience strategies to lenders, investors, and insurers.

That is the essence of supply chain transformation from a finance perspective. It is not about moving a factory or signing a new supplier contract. It is about rewiring the financial systems, metrics, and mindsets that enable those moves to happen quickly and profitably.

Supply Chain Transformation: The Window for Action Is Now

The McKinsey analysis is clear: by 2035, over 30 percent of global trade could swing from one corridor to another. $14 trillion in trade value is at stake. The corridors that win and lose are not random—they follow geopolitical, economic, and strategic logic.

The question is not whether your supply chain will be disrupted. It is whether you will be a passenger or a pilot during that disruption.

Supply chain transformation is not a cost center. It is a value creation opportunity. The firms that invest now in understanding their corridor exposures, modeling alternative scenarios, and building flexible financial and operational capabilities will emerge stronger, more resilient, and more valuable.

The tectonic plates of global trade are shifting. The only bad choice is to stand still.

🔗 Links for More:

For a deeper analysis of the data and insights, download the full report from McKinsey website or NeoForm LinkedIn page.

📌 About NeoForm:

NeoForm Business Partners is a transformational finance business partner specializing in financial transformation in private markets. We help portfolio companies and mid-cap firms navigate complexity, optimize capital structures, and build resilient operations through financial business transformations for an uncertain world.

Visit our blog for more insights on financial transformation, resilience, risk management and future of financial business and emerging trends.

🔗 Related Readings:

- The Great Trade Rearrangement: McKinsey Insights for Global Supply Chain

- How Global Economic Profit Reached an All-Time High

- The Future of Investing: Private Markets and Credit in 2025

- Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment

- The Next Big Arenas of Competition: 18 Super High Growth Sectors Shaping the Future Economy

Need tailored solutions? Explore NEO Services or contact our partners to learn how we can support your supply chain transformation journey.