Introduction: The Unraveling and Rewiring of Global Trade

For decades, the dominant narrative of globalization was one of ever-deepening integration. Supply chain stretched across the world, optimized for cost and efficiency, with China emerging as the “workshop of the world.” But that era is over. Geopolitical tensions, shifting national priorities, and a relentless series of disruptions have fundamentally altered the calculus.

We are now in the midst of what the McKinsey Global Institute (MGI) aptly terms “The Great Trade Rearrangement.” This isn’t a temporary blip but a structural, large-scale rewiring of the global economic system and supply chain. The recent surge in tariffs, particularly between the US and China, is not the cause of this shift but an accelerator of a trend already in motion.

For business leaders, the question is no longer if they need to adapt, but how. The old playbook is obsolete. In this comprehensive analysis, we dive deep into MGI’s groundbreaking research to provide you with a clear-eyed view of the new landscape. We’ll unpack a powerful new metric—the “rearrangement ratio”—that quantifies the challenge, identify the unexpected winners and pivotal players in this new geometry of trade, and outline the four critical strategic pathways every company must consider in supply chain.

The Core Concept: What is the “Rearrangement Ratio”?

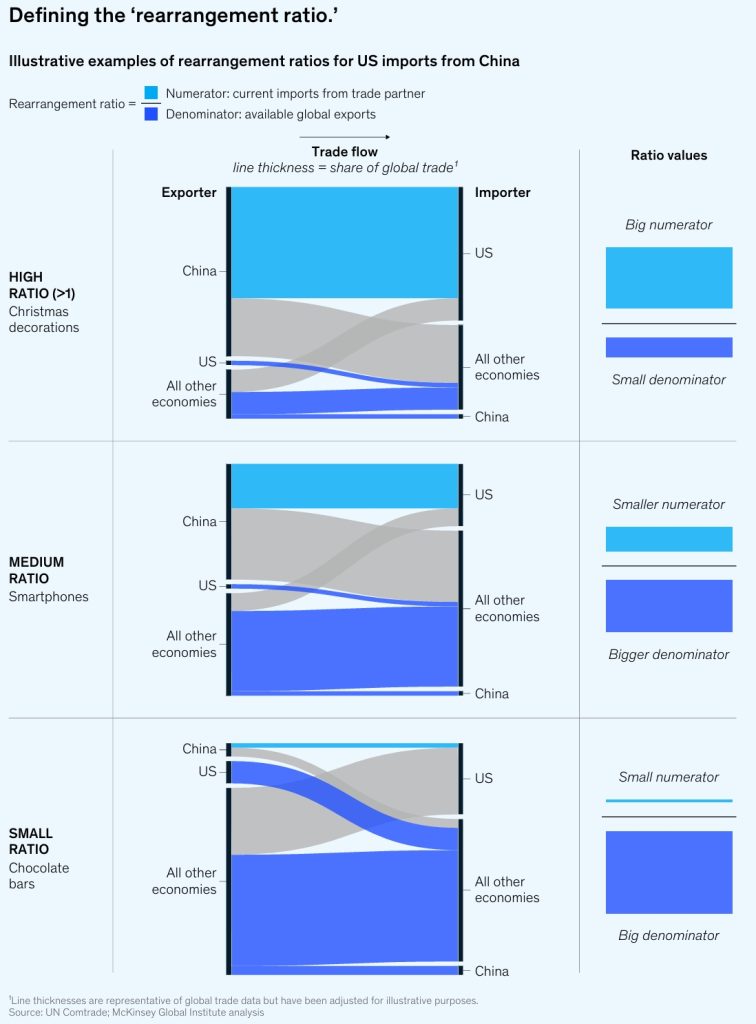

At the heart of understanding this shift is a simple but powerful concept introduced by MGI: the Rearrangement Ratio.

In simple terms, the rearrangement ratio measures how easy or hard it would be for a country (like the US) to replace its imports from a specific partner (like China) by sourcing from the rest of the world.

It’s calculated as follows:

- Numerator: A country’s imports of a specific product from a trade partner (e.g., US imports of laptops from China).

- Denominator: The “available global export market”—that is, all exports of that product from every other country, shipped to every other destination besides the importing country.

What the Ratio Tells Us:

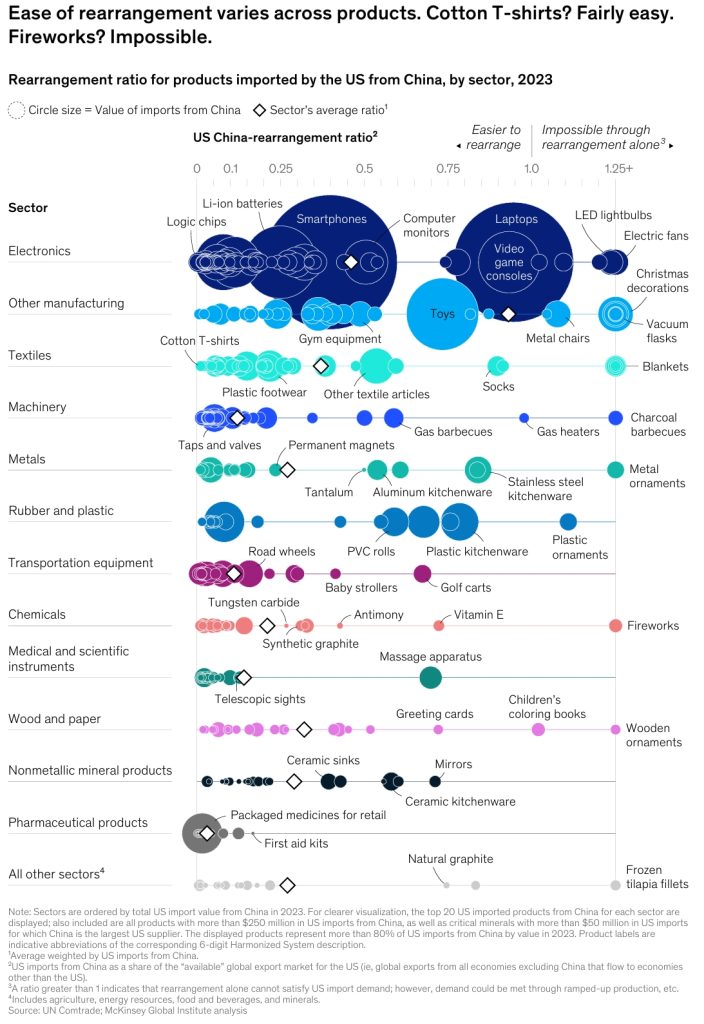

- Ratio < 0.1 (Easy to Rearrange): The import value is tiny compared to the available global market. Finding an alternative supplier should be relatively straightforward. Example: Cotton T-shirts. The US imports from China are a small fraction of what countries like Vietnam, Bangladesh, and others export globally.

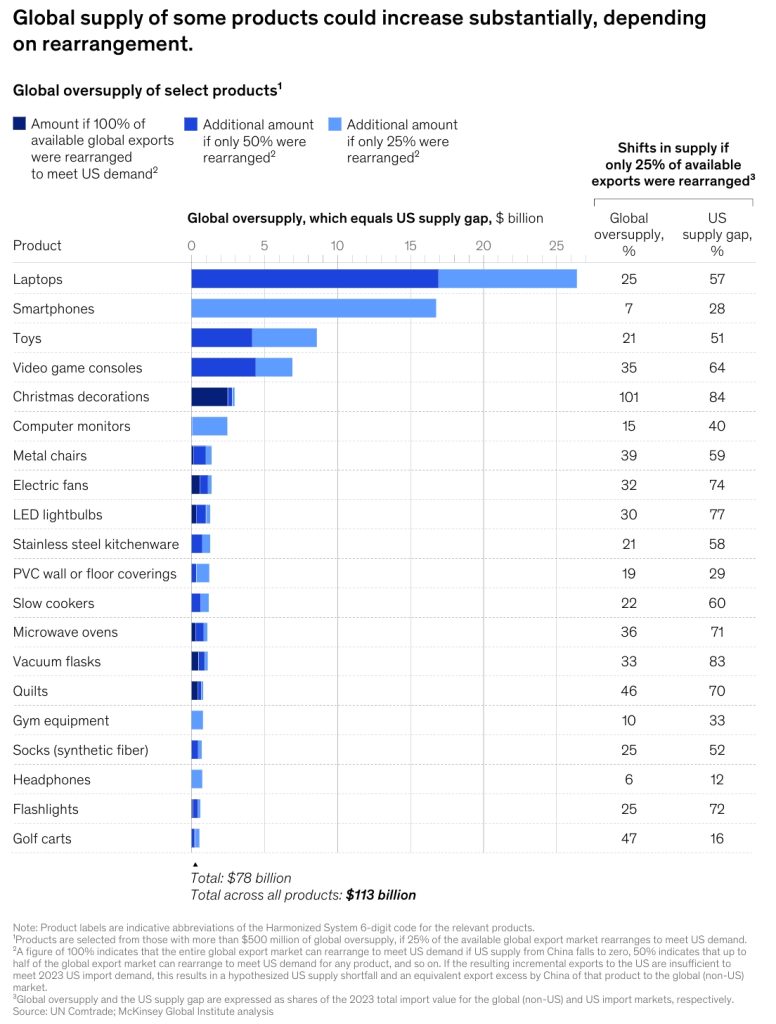

- Ratio > 1.0 (Impossible to Rearrange): The country’s imports from its partner exceed the entire available global export market. Simply shifting suppliers is not an option. Example: Christmas Decorations. The US imports $3 billion from China, but the total available market from all other countries is only $600 million. Even if the US bought every Christmas decoration exported by every other nation, it would still face a massive shortfall.

- Ratios between 0.1 and 1.0 (Hard but Possible): This is the messy middle ground. Rearrangement is feasible but requires significant effort, negotiation, and potentially higher costs.

This ratio moves the conversation from vague anxieties about “supply chain risk” to a quantifiable, product-level assessment of vulnerability and opportunity.

The State of Play: Key Findings from the Front Lines of Supply Chain Rearrangement

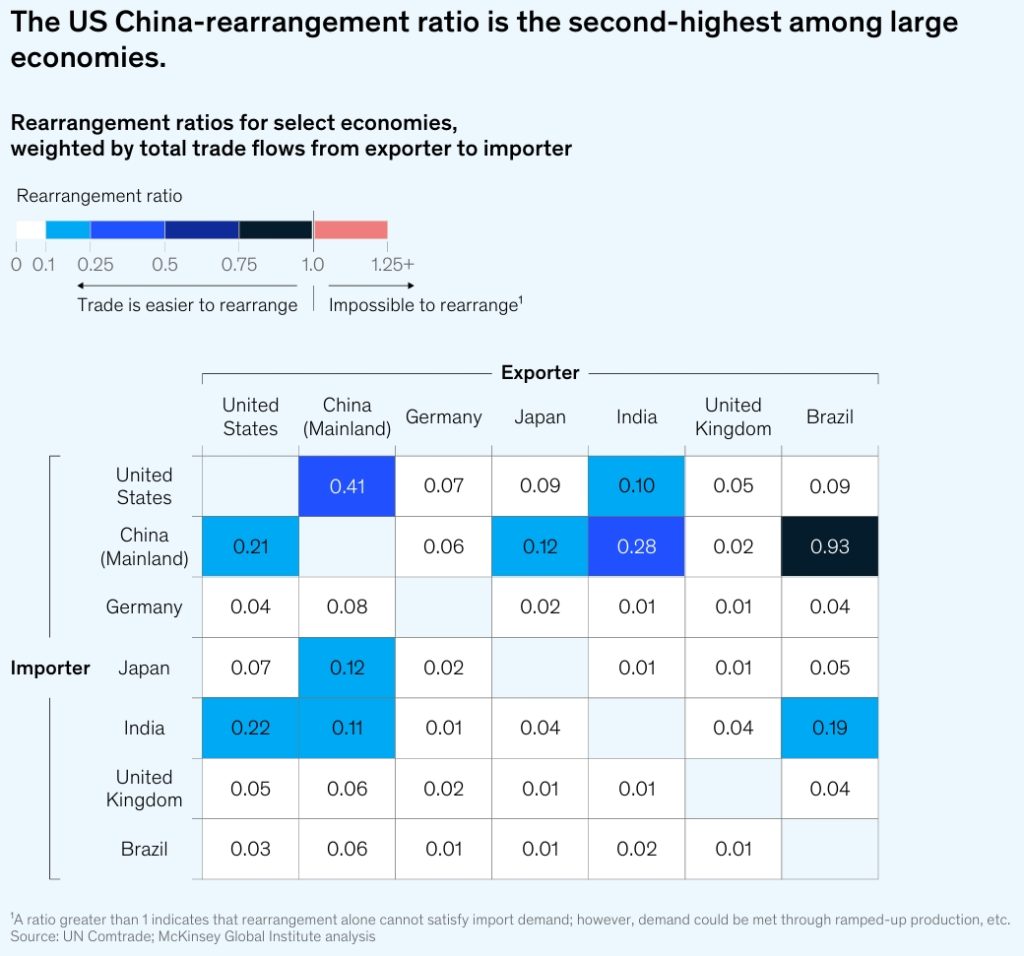

MGI’s application of the rearrangement ratio to US-China trade reveals several critical patterns that will define the next decade.

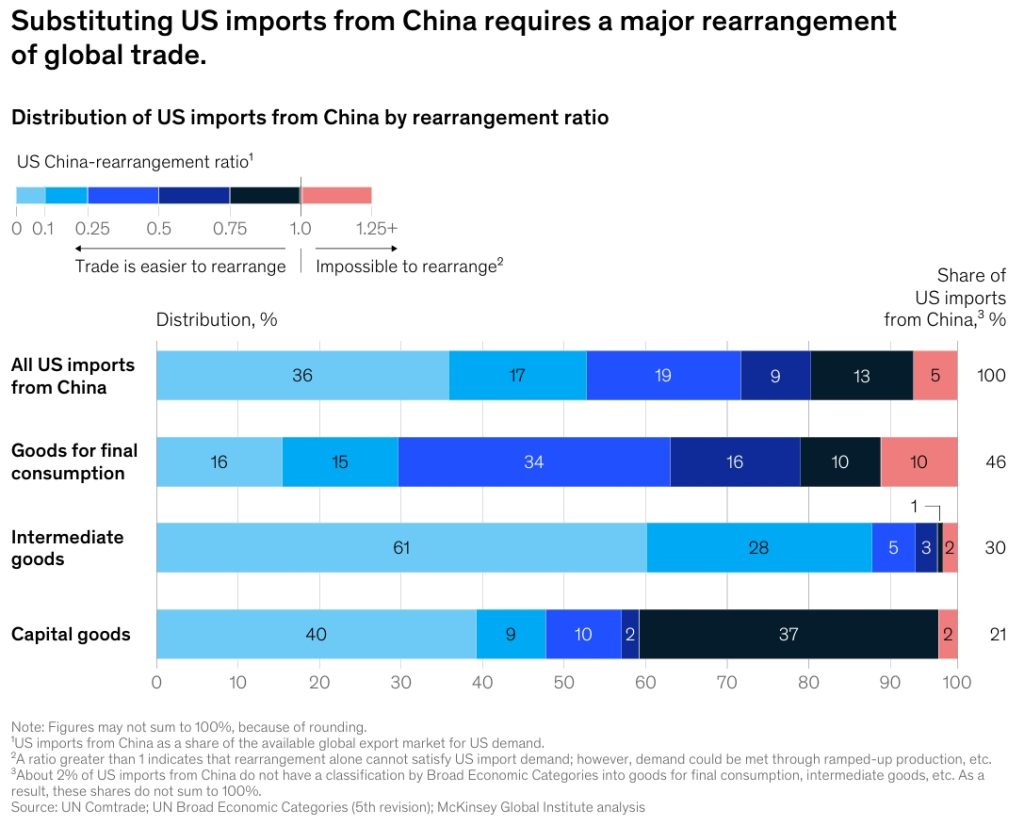

1. The Hard Truth: Consumer Goods Are the Biggest Challenge in Supply Chain

A striking finding is the disparity between business inputs and consumer goods.

- Business Inputs are Easier: A full 61% of intermediate goods (like semiconductors and auto parts) have a low rearrangement ratio (<0.1). The global supply base for these components is diverse and can be tapped.

- Consumer Goods are Harder: In contrast, only 16% of goods for final consumption fall into this “easy” category. Major products like laptops, smartphones, and toys have high ratios, making them extremely difficult to source away from China in the short term.

This means the average consumer will feel the impact of trade rearrangement more directly and painfully than many industrial sectors. Expect continued volatility and price increases for electronics and other everyday goods.

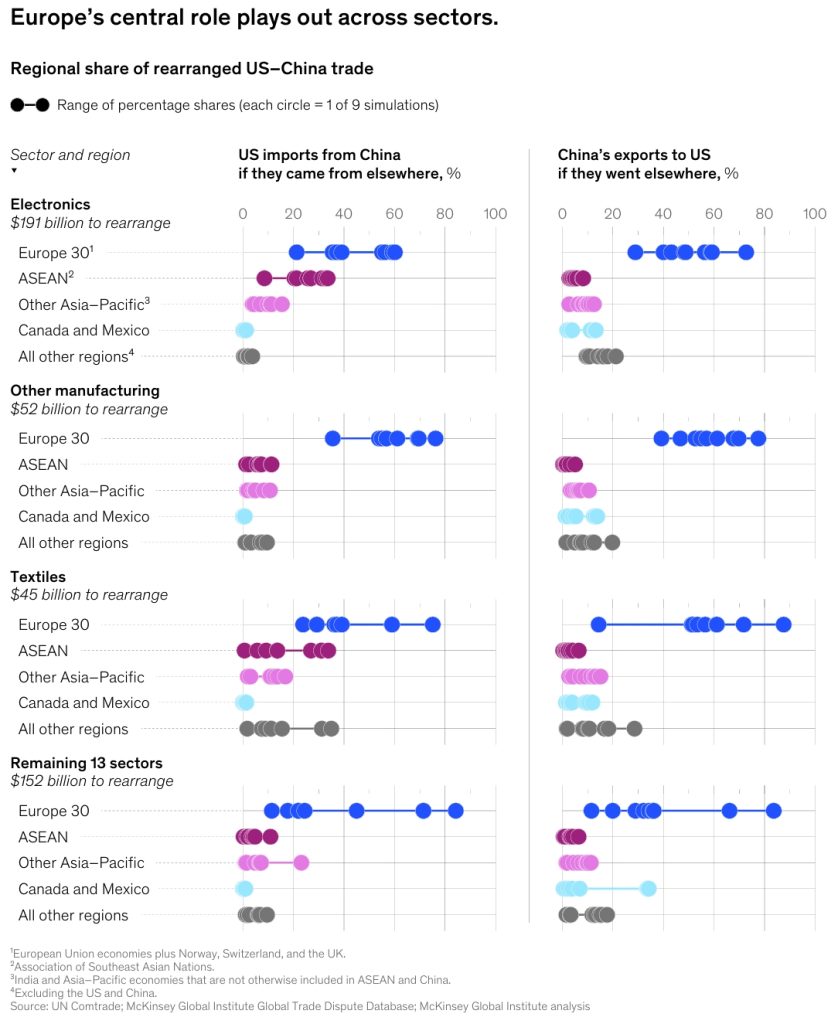

2. The Surprise Pivot: Europe as the Fulcrum of Global Trade

If you picture the global trade map having a new center of gravity, place it squarely on Europe. Across nine different simulations run by MGI, one pattern held constant: Europe emerges as the indispensable hub of rearranged supply chain.

Here’s how it works:

- Europe as an Exporter to the US: Europe is a major producer of many goods the US currently buys from China. As US companies seek alternatives, they will naturally turn to European suppliers. MGI simulations show European exports to the US increasing by nearly $200 billion.

- Europe as an Importer from China: But this creates a vacuum within Europe. If Polish factories are now sending lithium-ion batteries to the US, who supplies Europe? The answer, in many cases, is China. European imports from China are also projected to rise by nearly $200 billion.

This dual role makes Europe the critical linchpin. It will see its trade surplus with the US balloon while simultaneously deepening its economic interdependence with China. For businesses, this means Europe is simultaneously a key source of resilient supply chain and a massive, contested market for Chinese goods.

3. The Limited Roles of Other Major Players

The rearrangement is not a free-for-all where every US ally benefits equally.

- Canada & Mexico: Surprisingly, America’s closest trading partners see minimal export growth to the US. Why? Their manufacturing is already deeply integrated with the US economy. Over 80% of their goods exports already go to the US, leaving little “spare” capacity to rearrange.

- ASEAN (especially Vietnam): Southeast Asia plays a significant role, but it’s concentrated. Vietnam alone accounts for over 80% of ASEAN’s projected export growth, primarily in electronics (laptops and smartphones). Its role in other sectors like textiles is more variable and depends heavily on tariff policies.

- Japan & South Korea: These advanced economies also see limited gains. They tend to export complex components rather than the finished consumer goods that the US is trying to replace.

4. The US Itself is a Wild Card

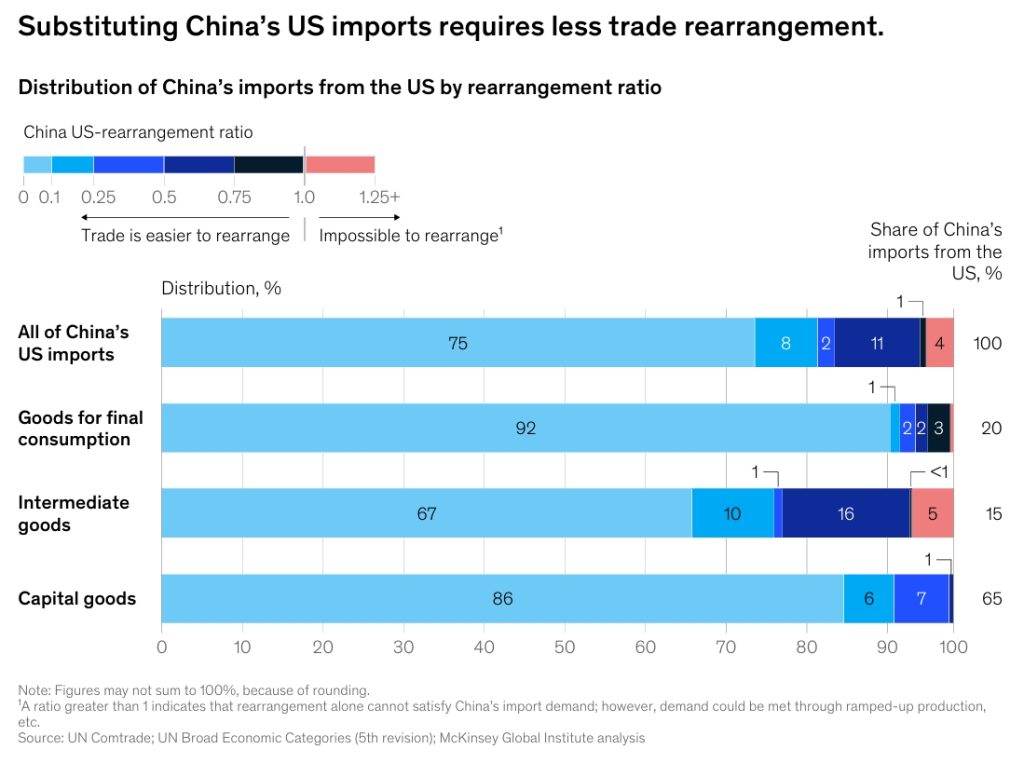

A crucial, often overlooked factor is the United States’ own export capacity. The US imported $440 billion from China in 2023 but also exported $1.7 trillion in goods to the world. MGI’s analysis suggests the US could redirect $180 billion of its own exports to meet domestic demand, effectively becoming its own largest alternative supplier.

This “US-first” approach would have massive ripple effects: Canada and Mexico would then need to replace the US goods they no longer receive, likely by turning to China, further accelerating the rearrangement.

The Four Strategic Pathways in Supply Chain Management

Faced with this new reality, companies cannot afford to be passive. MGI provides a vital alliterative framework for strategic response. Your company’s path will likely be a blend of all four.

1. Reduce

This involves decreasing consumption, either by consumers cutting back or firms using materials more efficiently.

- When to use it: As an immediate response to shortages or as a strategic choice to exit vulnerable or low-margin business lines.

- Key Questions for Leaders:

- Can we improve operational efficiency to use less of a scarce input?

- Is this the moment to pivot our product portfolio or target a less affected customer segment?

- Should we strategically “dial down” certain business lines that are too exposed?

2. Replace

This means substituting one product for another that is sufficiently similar.

- When to use it: When a direct rearrangement is too difficult or costly, but a functional alternative exists.

- Key Questions for Leaders:

- Which of our critical inputs or products need a “substitution contingency plan”?

- Can we redesign our products or processes to make future substitution easier by design?

- Is there a branding or marketing opportunity in promoting an alternative product?

3. Ramp Up

This is the most capital-intensive path: increasing total manufacturing capacity, either domestically or in allied countries.

- When to use it: For critical products where long-term supply is deemed insecure, and where the economics (including government incentives) justify the investment.

- Key Questions for Leaders:

- What are the true economics of ramping up, considering upfront costs, steady-state margins, and market opportunity?

- Do we have a clear trigger for action, or is there a first-mover advantage to acting preemptively?

- Should we partner with a supplier who is committing to ramp up capacity?

4. Rearrange

This is the act of shifting sourcing from one country to another without necessarily changing the product or total production.

- When to use it: When the rearrangement ratio is favorable and the tariff cost curve makes alternative suppliers economically viable.

- Key Questions for Leaders:

- For Importers: How do we secure access to low-tariff suppliers before our competitors do? What is our strategy for Europe vs. ASEAN vs. other regions?

- For Exporters in Low-Tariff Countries: How can we position ourselves to capture a greater share of the US market? Which specific products and customer segments should we target?

- For Firms Not Directly Trading with the US: How will we be affected by ripple effects? Can we capitalize on potential surpluses (to negotiate lower prices) or shortages (to gain market share) in our home markets?

The First-Mover Advantage and the Granularity Imperative

In the scramble to rearrange, the first-mover advantage is real. MGI’s analysis shows that first movers can secure supplies with an average tariff of just 5%, while latecomers could face average tariffs of 22%. The time for strategic planning and building new supplier relationships is now.

Furthermore, success in this new environment demands granularity. Macro-level trends are useful, but the real opportunities and risks lie at the product level. A company that understands the specific rearrangement dynamics for “synthetic-fiber socks” (which may require sourcing from 30 countries) versus “massage apparatus” (which may be sourced from one) will be the one that navigates this transition successfully.

Conclusion: Building Resilience in a Reordering World

The Great Trade Rearrangement is not a hypothetical future event; it is underway. The geometry of global trade is being redrawn, with Europe as its new fulcrum and product-level dynamics dictating the pace of change.

The strategies of the past—optimizing for lean, centralized, and cost-effective supply chain—are now sources of vulnerability. The new mandate is for resilience, diversification, and strategic agility.

Business leaders must:

- Diagnose their exposure using frameworks like the rearrangement ratio.

- Decide on their strategic mix of Reduction, Replacement, Ramp-up, and Rearrangement.

- Execute with speed and granularity, recognizing the immense first-mover advantages at stake.

The coming years will be defined by customers buying new things, from new sources, and using them in new ways. The companies that thrive will be those that see this rearrangement not as a threat, but as the defining strategic opportunity of our time.

🔗 Links for More:

Read the full report on McKinsey website or NeoForm LinkedIn page.

📌 About NeoForm:

At NeoForm Business Partners, we empower enterprises to maximize sustainable growth and profitability through financial efficiency & agility and manage internal and environmental risks with our transformational CFO services and strategic finance business partnering.

Visit NeoForm blog for more insights on global business trends.

🔗 Related Readings:

- The Next Big Arenas of Competition: 18 Super High Growth Sectors Shaping the Future Economy

- McKinsey Technology Trends 2025: What Is Crucial to Align Your Business

- McKinsey Global Private Markets Report 2025

- Private Equity Market Trends in 2025: A Year of Recovery and Strategic Shifts

- Global M&A Trends 2025: Key Insights from Bain Report

At NeoForm, we help businesses navigate complex global supply chain transformations. Explore NEO Services or Contact us today to learn how we can help you build a resilient, rearranged, and future-proofed supply chain strategy.

1 Comment

Bain Technology Report 2025: AI is Dividing Leaders - NeoForm Business Partners

[…] The Great Trade Rearrangement: McKinsey Insights for Global Supply Cha… […]