Introduction: The “iPhone Moment” for Credit Markets

In 2007, Steve Jobs unveiled the iPhone, revolutionizing how people interact with technology. Fast forward to 2025, and KKR’s latest market review suggests that credit markets are undergoing a similar transformation. In their report, “And One More Thing…in Credit,” KKR highlights how the shift from fragmented, siloed credit products to diversified, multi-asset solutions is redefining credit market outlook and investment strategies in 2025.

This blog post breaks down KKR’s key insights, including:

- The rise of diversified income strategies in a higher-for-longer rate environment

- The convergence of public and private credit markets

- The growing role of private credit and asset-based finance (ABF)

- Why Asia-Pacific (APAC) is the next frontier for credit investors

Let’s dive in.

1. The Credit Market’s “iPhone Moment”: A Unified, Multi-Asset Approach

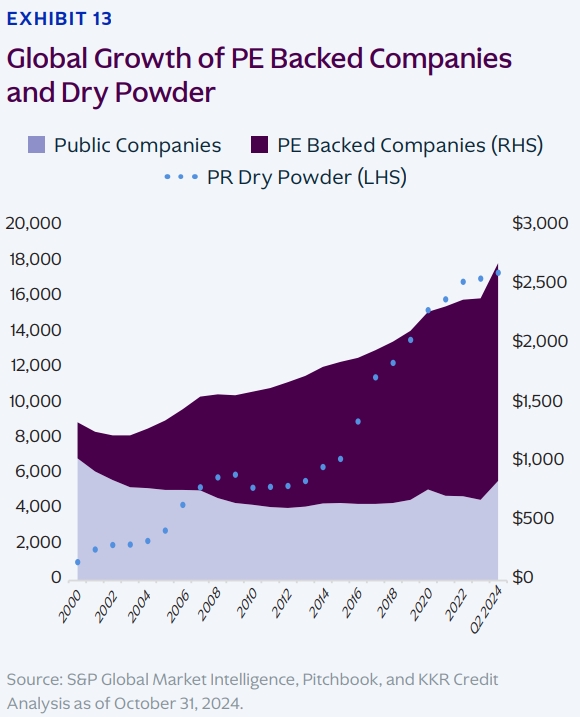

KKR draws a compelling parallel between the iPhone’s impact on tech and today’s credit market evolution. Just as the iPhone consolidated multiple devices into one seamless platform, modern credit portfolios are shifting toward multi-asset solutions that blend:

- Leveraged loans

- High-yield bonds

- Private credit

- Asset-based finance (ABF)

- Insurance-linked strategies

Why This Matters for Investors

- Diversification: A blended approach reduces volatility and enhances risk-adjusted returns.

- Income Stability: In a higher-rate environment, yield-generating assets are critical.

- Flexibility: Multi-asset strategies adapt to market cycles better than single-asset allocations.

“The shift in credit markets is significant, fundamentally redefining how capital is accessed and deployed.” — KKR

2. Key Themes Shaping the 2025 Credit Market Outlook

KKR’s report outlines four major themes for credit market outlook in 2025:

A. A Streamlined Shift: Market Dynamics & Fed Policy

- The Fed’s final 25bps rate cut in 2024 brought rates to 4.25%-4.5%, but Powell signaled patience on further easing.

- Inflation remains sticky, with December CPI at 2.9% YoY and core CPI at 3.2% YoY.

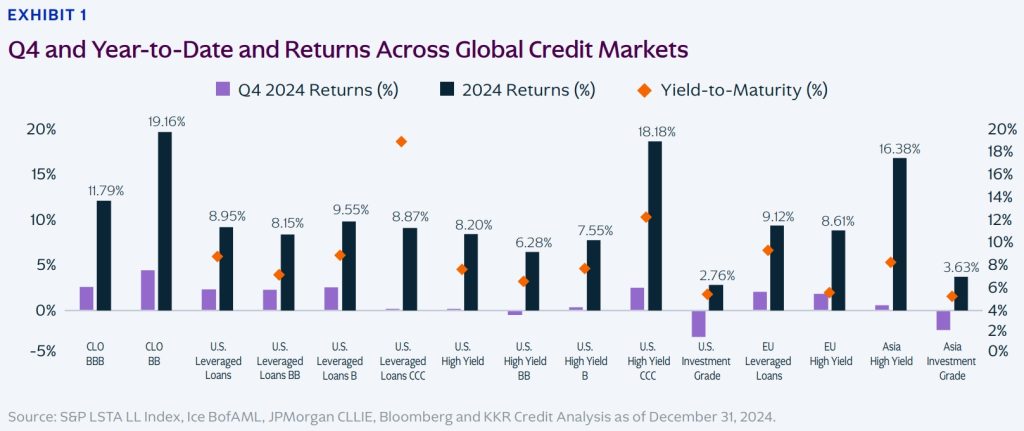

- Leveraged loans and CLOs saw record issuance, with $1.9T in new deals and $800B in repricings.

Takeaway: Investors should focus on yield-generating assets (e.g., direct lending, ABF) that thrive in this environment.

B. There’s an App for That: The Rise of Income Diversification

Just as the App Store revolutionized software access, cross-asset credit solutions are transforming finance:

- Private credit now surpasses leveraged loans in deal volume.

- Asset-based finance (ABF) is growing, offering non-corporate exposure (e.g., real estate, receivables).

- Asia-Pacific is leapfrogging Western markets in adopting multi-asset strategies.

Takeaway: The future belongs to flexible, hybrid financing models that blend debt and equity.

C. Reinventing Corporate Capital: The Emergence of Capital Solutions

With IPOs sluggish and private equity hold periods extending (now 7.1 years on average), companies are turning to structured capital solutions, including:

- NAV loans & continuation funds (helping PE firms monetize assets without selling).

- Sale-leaseback structures (freeing up capital for growth).

- Convertible debt & preferred equity (balancing income and upside).

Takeaway: Capital solutions offer downside protection + equity-like upside, making them a compelling alternative to traditional financing.

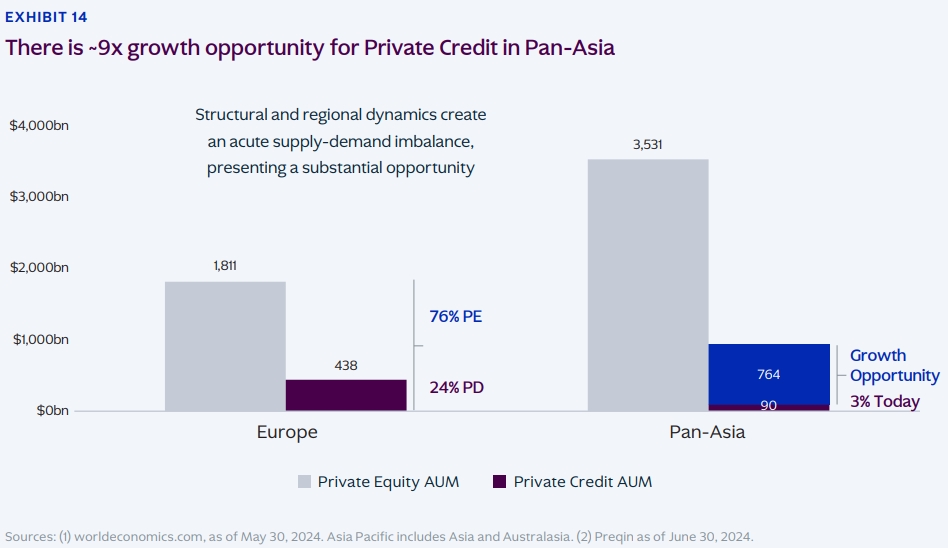

D. When is the Next Upgrade? Asia-Pacific’s Credit Boom

APAC is the most exciting opportunity in credit today:

- Private credit is underpenetrated (only 3% of the market vs. 24% in Europe).

- Domestic consumption drives 50% of GDP, with strong demand for tech, healthcare, and infrastructure financing.

- Japan is a standout, with corporate governance reforms unlocking value in undervalued assets.

Takeaway: APAC offers higher yields + lower correlation to Western markets, making it a must-have for diversified portfolios.

3. Actionable Insights for Investors

Based on KKR’s findings, here’s how investors can position themselves for 2025:

1. Allocate to Multi-Asset Credit Strategies

- Blend leveraged loans, private credit, and ABF for optimal diversification.

- Focus on yield-generating assets to combat inflation and rate volatility.

2. Capitalize on Private Credit Growth

- Direct lending and ABF are outperforming traditional leveraged loans.

- Look for perpetual evergreen funds, which reinvest income for compounding returns.

3. Explore Asia-Pacific Opportunities

- Favor developed markets (Australia, Japan, Singapore) for creditor-friendly structures.

- Consider offshore collateralization to mitigate jurisdictional risks.

4. Leverage Capital Solutions for Flexibility

- NAV loans and continuation funds help unlock liquidity in illiquid PE portfolios.

- Sale-leasebacks enable capital-light transitions for corporates.

Conclusion: Embracing the New Credit Paradigm

KKR’s report makes one thing clear: The future of credit is integrated, diversified, and global. Just as the iPhone replaced flip phones, multi-asset credit strategies are displacing traditional siloed approaches.

For investors, this means:

✅ Prioritizing yield and resilience in a higher-for-longer rate world.

✅ Expanding into private credit and ABF for enhanced returns.

✅ Tapping into APAC’s growth for uncorrelated alpha.

The credit market’s “iPhone moment” is here—will you adapt or risk irrelevance?

Links For More

Download and read full report on KKR’s website or NeoForm LinkedIn page.

Want to stay ahead of market trends? Check out NeoForm’s insights for expert analysis on private markets and alternative investments.

Need help on managing your investment strategies in private markets? Contact our experts for more tailored solutions.

2 Comments

McKinsey Global Private Markets Report 2025 - NeoForm Business Partners

[…] 3. Private Debt: Steady in the Crosswinds […]

Asset-Based Finance: The $6+ Trillion Private Credit Opportunity You Can't Ignore - NeoForm Business Partners

[…] Credit Market Outlook 2025: Rising Private Credit and Asia-Pacific […]

Comments are closed.