Beyond the Slowdown: Why Strategic Investment is the Only Path to Productivity Growth

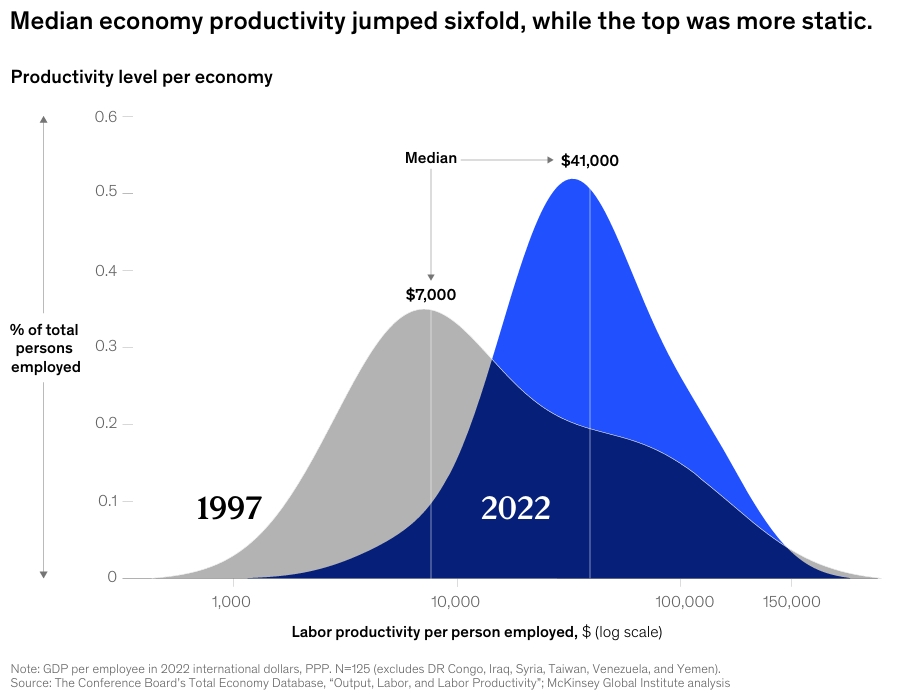

For a quarter of a century, the global economy was on a remarkable trajectory. Living standards climbed, poverty rates plummeted, and emerging economies lifted billions of people into a new era of prosperity. The engine behind this progress was a singular, powerful force: productivity growth. The McKinsey Global Institute’s (MGI) latest research, “Investing in productivity growth,” reveals that the median economy’s productivity jumped an astounding sixfold between 1997 and 2022.

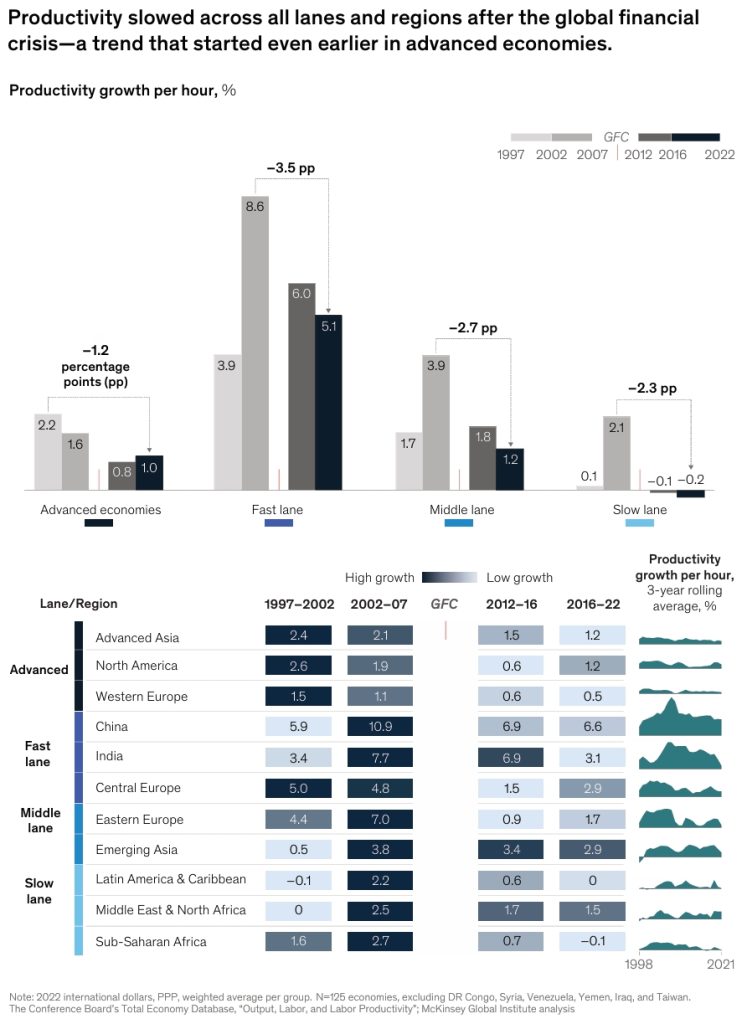

But if you look under the hood of this global success story, the picture becomes more complex and, frankly, more concerning. The powerful engine of growth is sputtering. Since the Global Financial Crisis (GFC) around 2008, the world has experienced a near-universal productivity slowdown. Advanced economies, once the frontier of efficiency, have seen their growth rates cut in half. Meanwhile, a vast segment of the emerging world, home to 1.4 billion people, has been left in the “slow lane,” failing to narrow the gap with their wealthier peers.

For business leaders, investors, and financial strategists navigating the private markets, this isn’t just an academic data point. It is the defining macroeconomic backdrop of our era. Stagnant productivity translates directly to tepid revenue growth, compressed margins, and heightened competition for diminishing returns. As the report starkly notes, without a surge in productivity, we could be facing a prolonged period of economic drag, making the already complex challenges of the net-zero transition, aging populations, and supply chain reconfiguration feel insurmountable.

However, within this diagnosis lies a powerful, actionable cure. The common thread tying together the success stories of the past and the potential for future prosperity is singular: investment.

This blog post synthesizes the key findings of the MGI report, translating its data-heavy analysis into a clear narrative for decision-makers. We will explore why productivity has stalled, what separates the “fast-lane” economies from the laggards, and most importantly, what a strategic agenda for productivity growth investment looks like in this new geo-economic era.

The Great Slowdown: A Tale of Two Waves

To understand where we are going, we must first understand how we got here. The MGI report debunks the popular narrative that the productivity slowdown was solely a post-GFC phenomenon. In reality, the seeds were planted earlier.

For advanced economies, the two decades leading up to the GFC were powered by two distinct and powerful waves in the manufacturing sector:

- The Moore’s Law Wave: The exponential increase in computing power translated into massive quality and price improvements, fueling high total factor productivity (TFP) growth in the electronics sector.

- The Offshoring & Restructuring Wave: Companies aggressively automated and moved labor-intensive production to lower-cost nations. This led to a sharp decline in manufacturing hours worked in advanced economies while capital investment remained high, creating a powerful boost in capital per worker and, consequently, productivity.

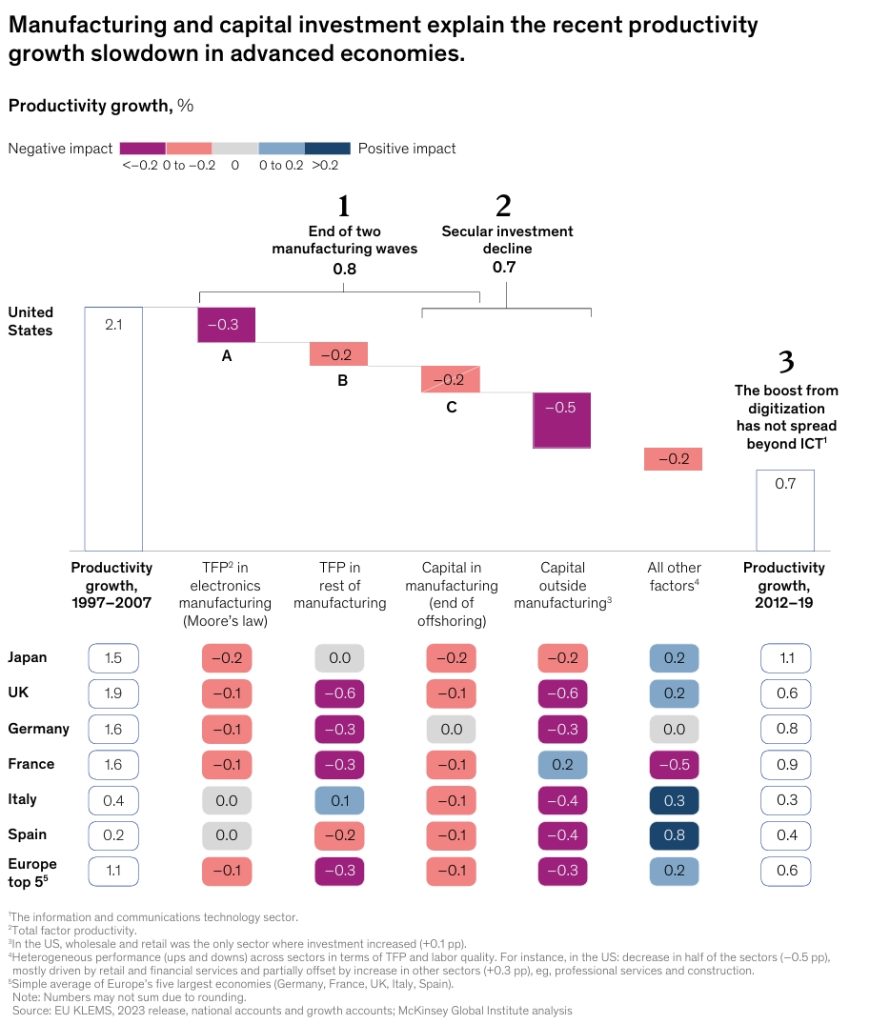

These waves created a powerful surge, but they were inherently finite. Moore’s law, while still in effect, began to deliver diminishing returns in terms of real value-added growth. The low-hanging fruit of offshoring was largely picked. When the GFC hit, it didn’t just create a temporary dip; it broke these waves entirely.

As the report illustrates using the US as an example, the contribution of manufacturing to overall productivity growth plummeted after the crisis. Crucially, nothing emerged to take its place. The much-hyped digital revolution, while creating immense value within the ICT sector itself, failed to make a broad splash across the rest of the economy—at least not yet.

The Investment Vacuum: The Core of the Crisis

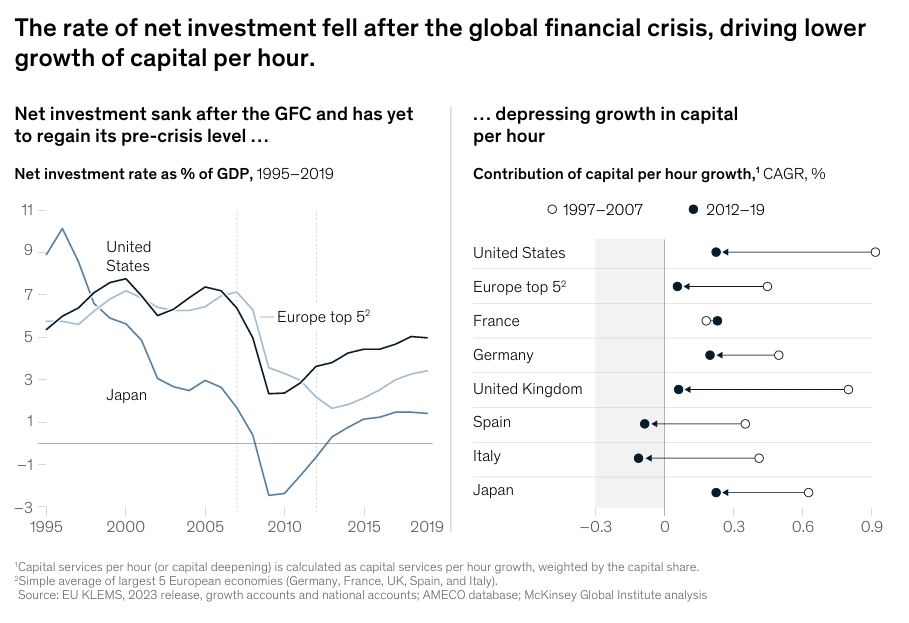

If the breaking waves explain the “what,” the decline in investment explains the “why.” The MGI analysis is unequivocal: a marked and persistent decline in the growth of capital per worker explains roughly half of the post-GFC productivity slowdown in major advanced economies.

This wasn’t just a dip in a single sector. It was a secular decline spanning almost all industries. The rate of net investment as a percentage of GDP has never recovered to pre-crisis levels. In the United States, gross fixed capital formation in tangible assets like machinery, equipment, and buildings fell from 22% to just 14% of gross value added. While investment in intangibles (R&D, software) proved more resilient, it was not enough to offset the collapse in the physical world.

Why did investment dry up? The timing points to the crises themselves. In the wake of the dot-com bust and then the GFC, the macroeconomic outlook was uncertain and demand was weak. Businesses, spooked by the environment, hoarded cash instead of deploying it. This created a “hysteresis” effect—a temporary shock that caused long-term scarring. Even when demand returned, the investment never did, trapping economies in a cycle of sluggish demand and low productivity growth. While regulation and other factors may have played a supporting role, the primary culprit was a simple lack of confidence and demand.

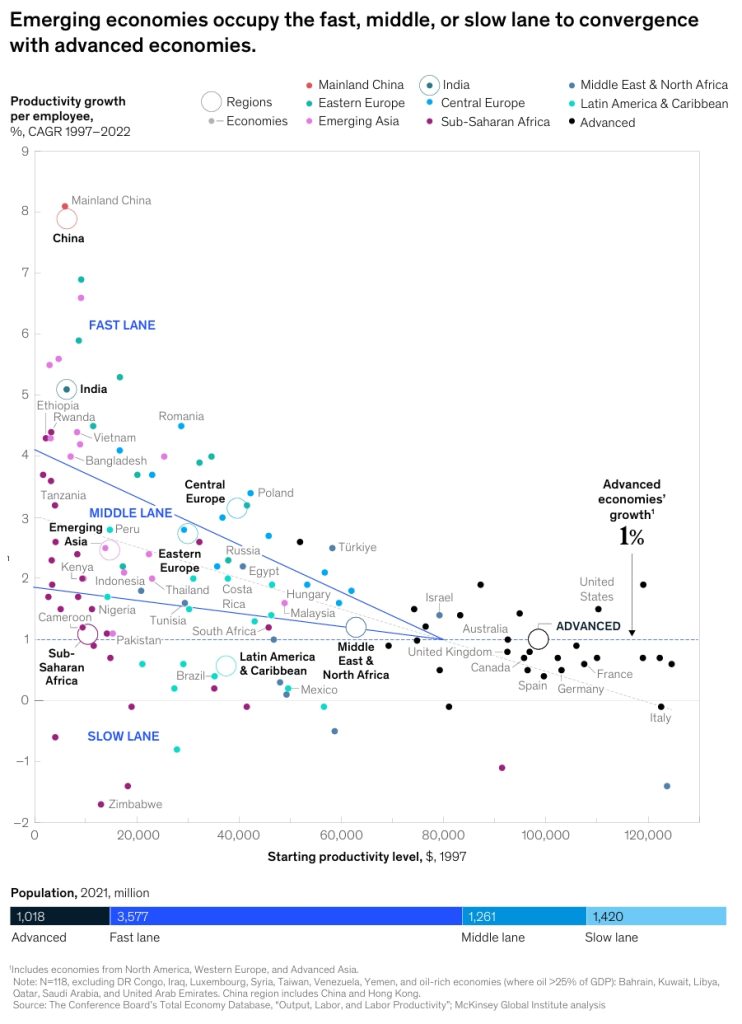

The Three-Lane Highway to Prosperity (or Poverty)

If advanced economies are struggling to maintain their lead, the story in the emerging world is one of stark divergence. The report visualizes this as a three-lane highway.

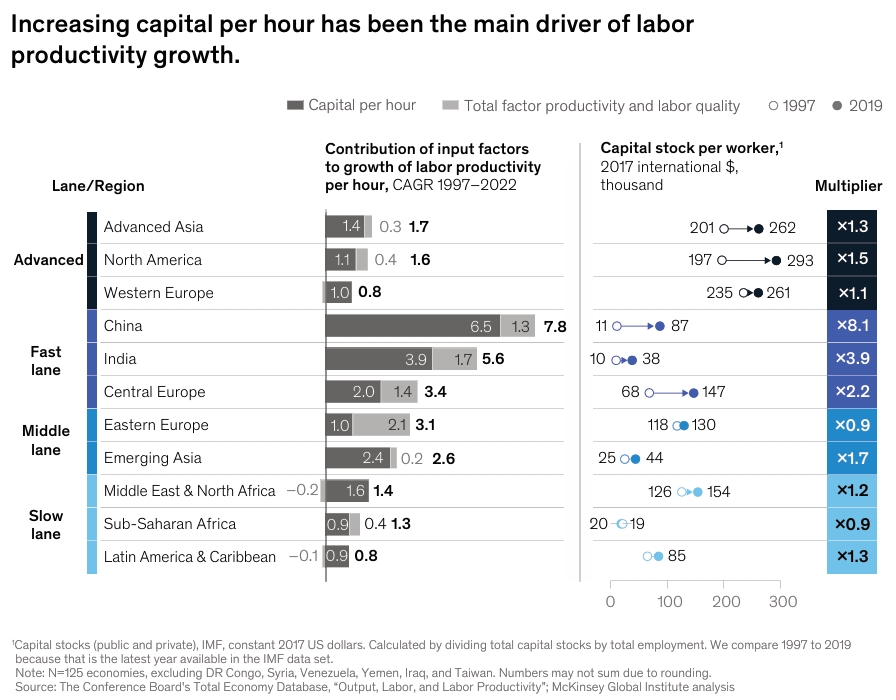

- The Fast Lane (3.6 billion people): This lane, occupied by China, India, parts of Central and Eastern Europe, and a few other stars, is characterized by blistering productivity growth of around 6% per year. At this pace, they are on track to converge with advanced economies within a generation. The key? Radically high capital investment, sustained at 20% to 40% of GDP. This capital wasn’t just deployed blindly. It was channeled into building world-class infrastructure, powering successful urbanization, and creating globally connected, sophisticated manufacturing hubs.

- The Middle Lane (1.3 billion people): Economies here are growing, but slowly. At their current 2.1% annual pace, it would take them over a century to catch up. They have many of the building blocks but lack the sustained, high-octane investment needed to truly accelerate.

- The Slow Lane (1.4 billion people): This is the lane of stagnation. With productivity growth averaging a paltry 0.3%, these economies, largely in Latin America, Sub-Saharan Africa, and the Middle East, are not just failing to catch up—they are actively falling further behind. They suffer from chronic underinvestment, weak institutions, and a reliance on volatile commodity exports.

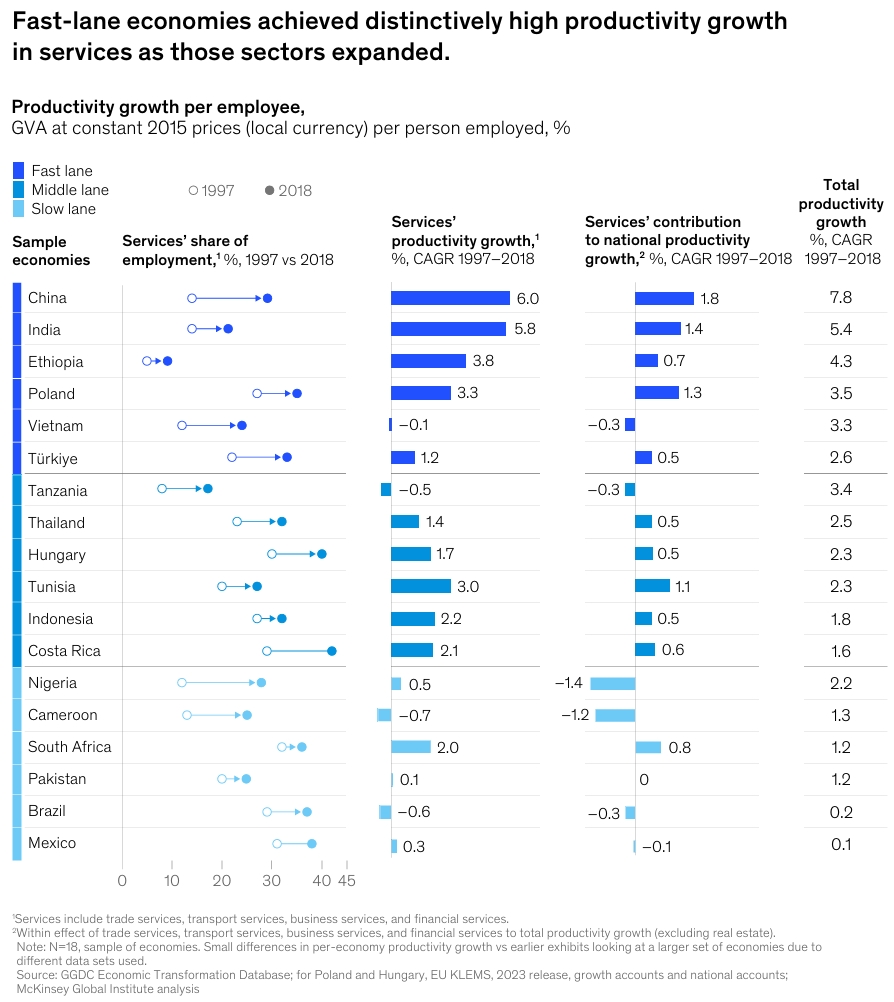

The report’s analysis of the fast lane is particularly insightful. It challenges the traditional development narrative that focuses solely on industrialization. While manufacturing remains vital, fast-lane economies also achieved distinctively high productivity growth within their service sectors. They didn’t just move people from farms to cities; they invested in the capital—from digital infrastructure in India to modern retail formats in China—that made those urban service jobs highly productive. They built the cities in the right way.

An Agenda for Action: Investment in Productivity Growth

For NeoForm’s audience of financial transformers and private market leaders, the report’s final section is the most critical. It poses questions that will shape the future of productivity growth. For those looking to deploy capital or advise portfolio companies, these are the strategic battlegrounds.

1. Can We Revamp Investment in a New Macro Environment?

This is the core imperative. For advanced economies, reversing the slowdown means reversing the investment decline. The higher inflation and interest rates of today, while painful, could paradoxically be a positive sign. They may indicate we are leaving behind an era of “secular stagnation” and weak demand. Higher real wages can motivate capital investment. We are seeing early signs of this in the US, with a boom in manufacturing construction (think battery plants and semiconductor fabs) and massive R&D spending by tech giants racing for AI supremacy.

- NeoForm Insight: For private equity and infrastructure funds, this signals a shift in opportunity. The focus moves from financial engineering and multiple expansion toward operational improvement and funding real asset creation. Due diligence must now place an even greater emphasis on a target company’s capital expenditure plans and their potential to drive organic growth.

2. Can We Harness the Promise of Technology?

The report is cautiously optimistic about AI and digitization. It notes that previous MGI research estimated digitization could add 0.5 to 1.0 percentage point to annual productivity growth. Generative AI could add another 0.5 points or more. The key is that these are not automatic gains. They require complementary investment in processes, skills, and new business models.

- NeoForm Insight: This is where financial transformation becomes a competitive weapon. Finance functions must move beyond reporting to become the architects of value creation, helping operating partners identify, fund, and track the ROI of technology investments across a portfolio.

3. Can We Overcome the Demographic Drag?

Aging populations in advanced economies and China are a significant headwind. An older workforce can be less dynamic and slower to adapt. This creates a powerful incentive for productivity growth investment in automation and AI to compensate for fewer workers.

- NeoForm Insight: For portfolio companies, labor scarcity is a permanent reality. Business cases for automation and labor-saving technologies become significantly more attractive. Companies that fail to invest in this area will find themselves structurally uncompetitive.

4. Can We Drive Productivity in Services?

As manufacturing automates and employs fewer people, economies become more service-intensive. This is a challenge because service-sector productivity (think healthcare, hospitality, education) has historically been harder to improve. However, the fast-lane emerging economies proved it is possible. The same logic applies to advanced economies.

- NeoForm Insight: This is a massive, under-tapped opportunity for private capital. Investing in the digitization and process re-engineering of fragmented, traditional service industries (e.g., business services, logistics, healthcare providers) is a direct route to creating value. It requires deep operational expertise, not just financial leverage.

5. Can We Maintain High Global Cooperation?

The fragmentation of global trade is a major threat to productivity. Global value chains allowed for specialization and the rapid diffusion of ideas. A retreat from globalization could choke off this vital source of growth. However, reconfiguration also creates winners, with surges in greenfield investment seen recently in India and parts of Africa.

- NeoForm Insight: Supply chain resilience is now a board-level topic. Investment strategies must account for geopolitical risk. This could mean investing in nearshoring capacity, dual-sourcing strategies, or building digital infrastructure that enables trade in services across borders.

6. Can We Re-energize Productively?

The energy transition is a double-edged sword. In the short term, high energy costs and investments in unprofitable green tech can weigh on productivity. In the long term, however, investment in clean energy and efficiency can be a major productivity boon, lowering operating costs and creating new, high-value industries.

- NeoForm Insight: This is perhaps the largest capital reallocation in history. It creates enormous opportunities in renewables, grid modernization, electrification of transport, and the mining of critical minerals. Private markets are uniquely positioned to fund this transition with patient, long-term capital, provided the regulatory environment is stable and supportive.

Conclusion: Investment in Productivity Growth

The McKinsey Global Institute’s report delivers a clear and urgent message: the era of effortless productivity gains is over. The free lunches provided by Moore’s Law and unfettered globalization have been largely consumed. The path forward requires deliberate, sustained, and strategic productivity growth investment.

This is not a threat, but a call to action. In a world where top-line growth is hard to come by, productivity is the ultimate source of value creation. It is the multiplier that turns a good business into a great one.

The winners of the next quarter-century will not be those who simply wait for growth to return. They will be the ones who actively build it—by funding new infrastructure, deploying transformative technology, professionalizing service industries, and backing the energy transition. They will be the investors who understand that in a capital-constrained world, the most productive allocation of that capital is not just a financial exercise, but the foundation of shared prosperity.

🔗 Links for More:

For a deeper analysis of the data and regional insights, download the full report from McKinsey website or NeoForm LinkedIn page.

📌 About NeoForm:

At NeoForm Business Partners, we help private equity firms and their portfolio companies navigate complexity, build value, and achieve extraordinary results through financial transformation.

Visit our blog for more insights on M&A, private equity, private debt and private markets.

🔗 Related Readings:

- The Future of Investing: Private Markets and Credit in 2025

- The Next Big Arenas of Competition: 18 Super High Growth Sectors Shaping the Future Economy

- The Great Trade Rearrangement: McKinsey Insights for Global Supply Chain

- How Global Economic Profit Reached an All-Time High

- Turning Sustainability into Growth: The Pragmatist’s Playbook for Visionary CEOs by Bain

Need tailored solutions? Explore NEO Services or contact our partners to learn how our expertise can help you to elevate and execute your private equity strategies from value creation planning to exit readiness.