The 2026 Healthcare Private Equity Landscape: Record Growth, Strategic Shifts, and the Future of Value Creation

The global healthcare private equity (PE) market isn’t just recovering—it’s redefining its limits. According to Bain & Company’s Global Healthcare Private Equity Report 2026, 2025 was a landmark year of resurgence and record-breaking growth. It is setting a powerful stage for the strategic evolution of the sector. For transformational finance partners like NeoForm, navigating this dynamic landscape requires a deep understanding of where capital is flowing, how value is being engineered, and what separates the winning investments from the rest.

Bain’s report reveals a sector brimming with confidence, fueled by massive dry powder and a mature portfolio of assets ready for exit. But beyond the impressive headline numbers—over $190 billion in estimated deal value—lies a more nuanced story of regional shifts, sector-specific strategies, and a fundamental evolution in the playbook for value creation.

2025 Summary: A Year of Resilient Growth for Healthcare Private Equity

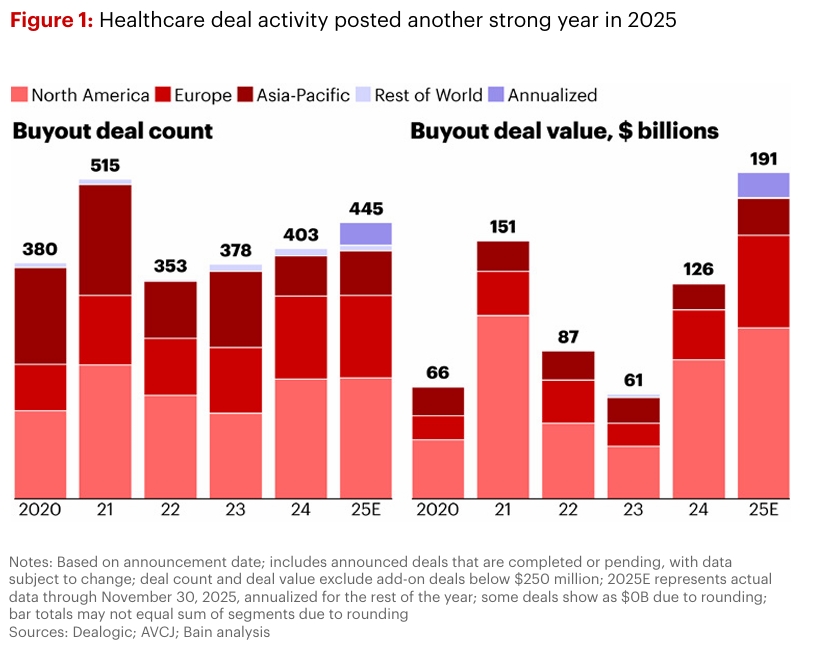

Despite a temporary pause in Q2 2025 linked to macroeconomic and tariff uncertainties, global healthcare PE activity soared to an all-time high. Key highlights include:

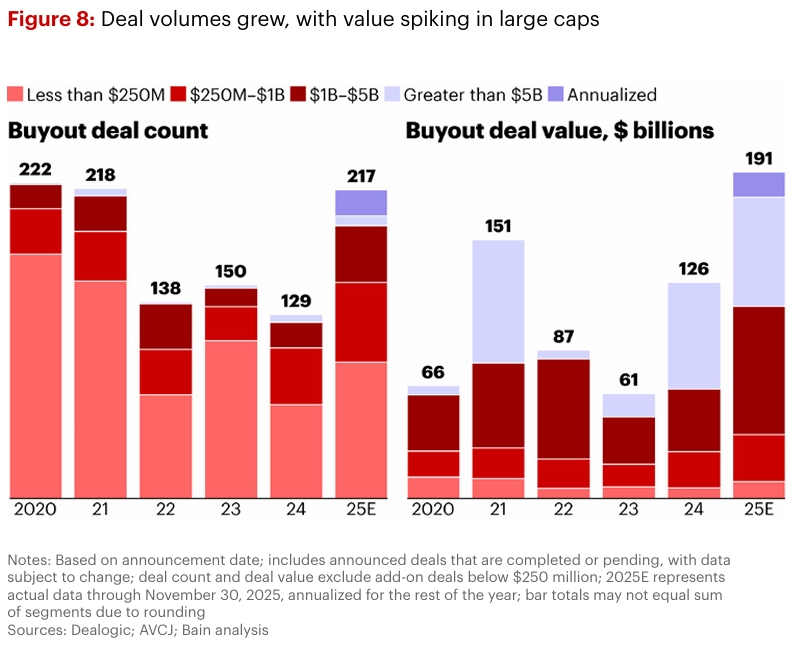

- Record Deal Value: Disclosed deal value surpassed an estimated $191 billion, eclipsing the previous 2021 high.

- Robust Volume: Investors announced ~445 buyouts, the second-highest annual total on record.

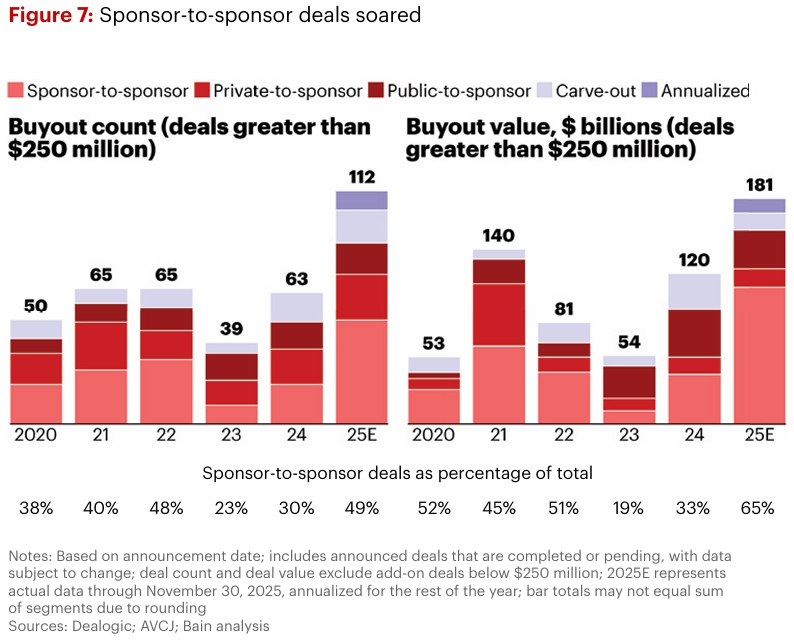

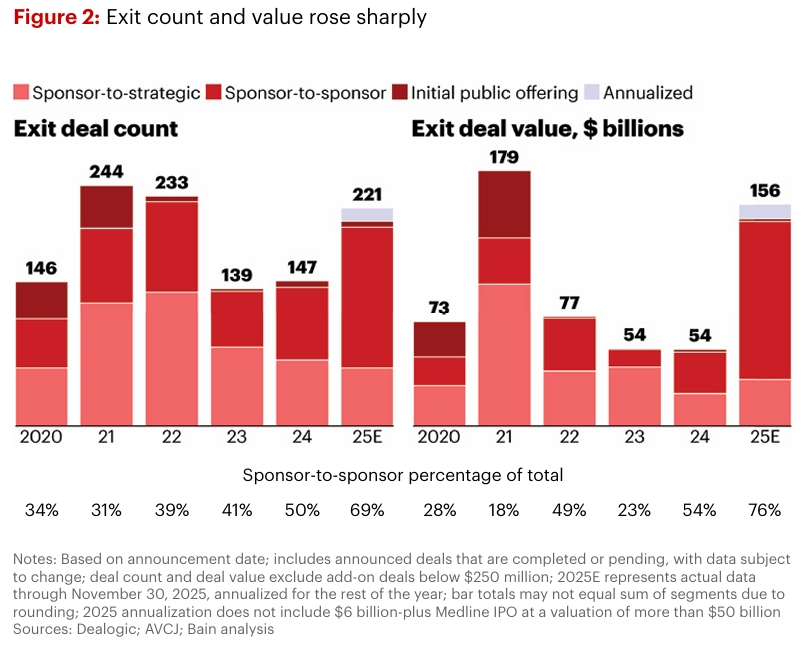

- Exit Resurgence: Exit value leaped from $54 billion in 2024 to an expected $156 billion in 2025, driven by a surge in large sponsor-to-sponsor transactions.

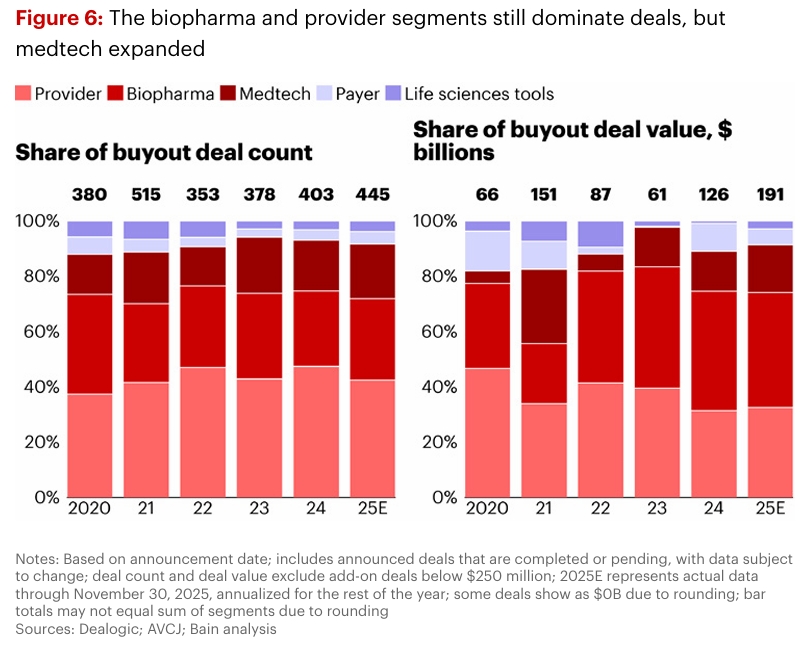

- Sector Anchors: Biopharma and Provider services remained the largest segments. While Medtech emerged as a powerful new growth engine, nearly doubling its deal value.

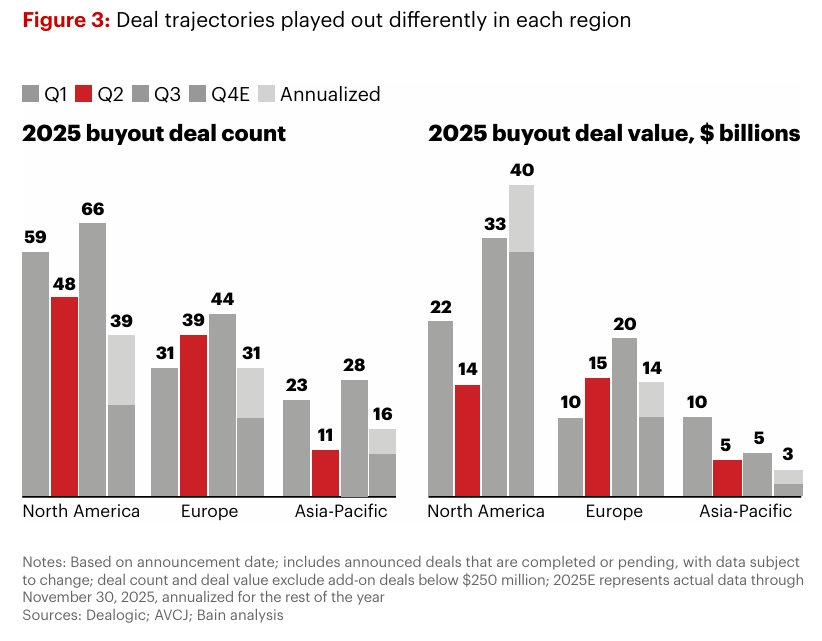

- Regional Rebound: Europe led with sustained strength. While North America and Asia-Pacific recovered from a Q2 slowdown to post healthy annual gains.

This activity underscores a market characterized by both durability and evolution. Investors are deploying capital with greater selectivity. They are focusing on assets where operational improvement, technological enablement, and strategic positioning can unlock outsized returns in an increasingly competitive environment.

Part 1: Deep Dive into the 2025 Market Resurgence of Healthcare PE

The Regional Picture: Diverging Trajectories, Unified Growth

The global story in 2025 was one of interconnected yet distinct regional narratives.

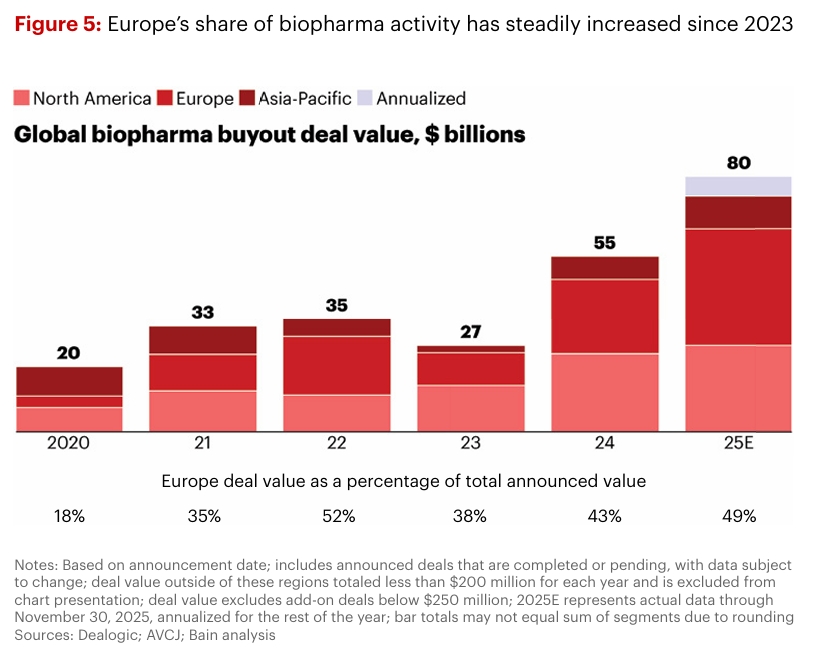

Europe: Fueled by Biopharma Scale

Europe’s dealmaking intensity sharpened significantly, with estimated deal value doubling to ~$59 billion. The region was driven by a reemergence of large-cap activity in biopharma, home to the top five deals accounting for 65% of the region’s total value. The significant rebound in exits, such as the sale of STADA Arzneimittel AG, highlights a robust and liquid market for high-quality assets.

North America: Large Transactions Propel Performance

After a Q2 pullback due to policy uncertainty, North America’s market was propelled by an uptick in mega-deals (>$1 billion). Twenty-six such transactions crossed this threshold in 2025, with over 70% being sponsor-to-sponsor sales. This indicates a mature market where PE firms are actively trading mature, scaled assets among themselves, seeking the next phase of value creation.

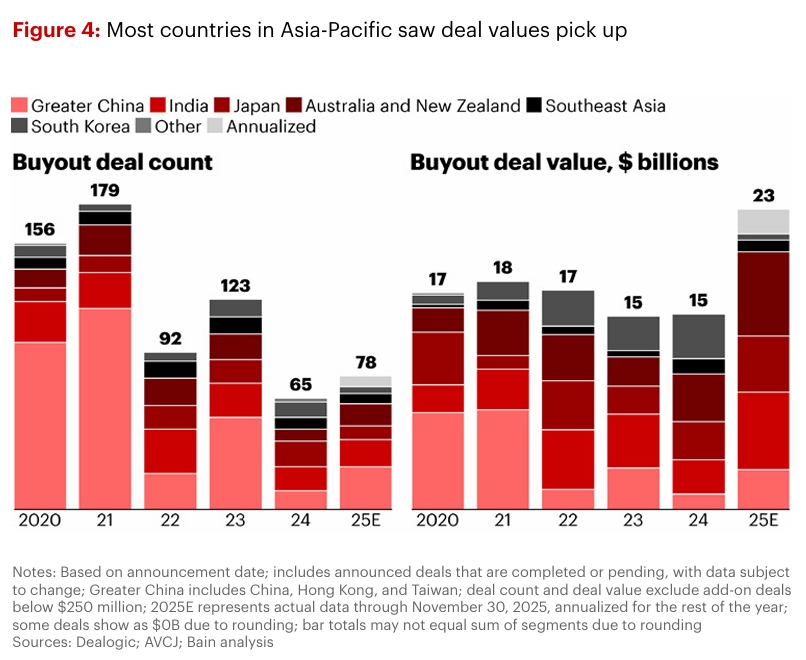

Asia-Pacific: Broad-Based Strength and Depth

APAC set a record deal value, exceeding 2021’s high by over 30%. Growth was notably broad-based across countries (with Greater China, Japan, and India standing out) and sectors. While biopharma and provider services dominated, medtech and healthcare IT saw accelerating interest. The doubling of provider/hospital deal value signals deepening investment in core care delivery infrastructure across the region.

Sector Spotlight: Where Capital Is Concentrated

In healthcare private equity report 2026, bain analyzes most active sectors in healthcare industry:

1. Biopharma: The Commanding Leader

Biopharma reaffirmed its pole position, with deal value rising to an estimated $80 billion. It consistently accounts for roughly 30% of annual deal volume. Europe was the primary engine of this growth. Investors continue to favor resilient sub-sectors like Contract Development and Manufacturing Organizations (CDMOs), while also scaling opportunities in generics, consumer health, and animal health—areas seen as less exposed to payer pressure.

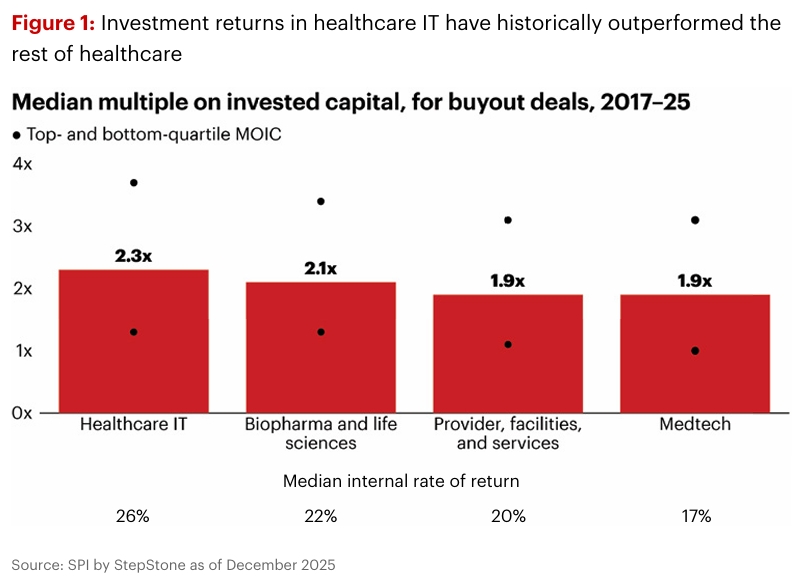

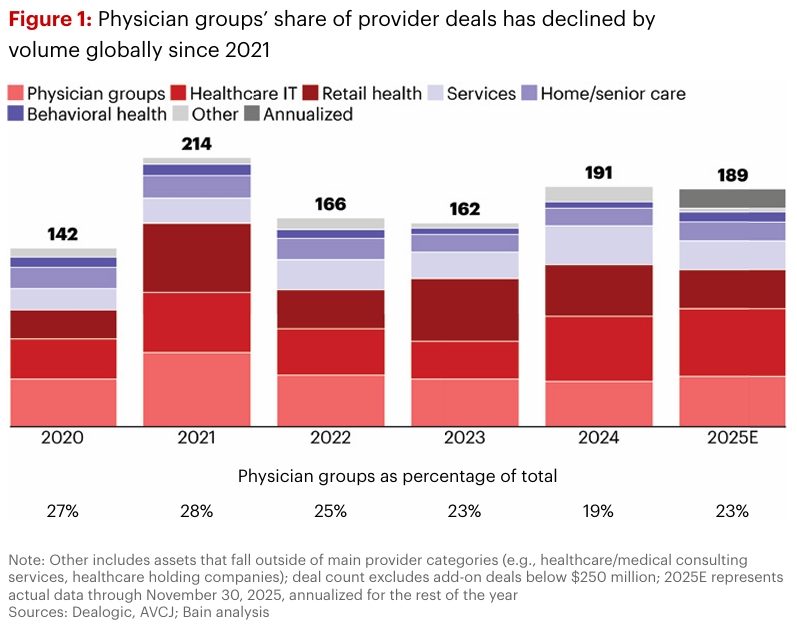

2. Provider & Services: IT-Driven Transformation

Deal value in the provider segment jumped 57% to ~$62 billion. The standout story within this category was Healthcare IT, where deal value doubled to an estimated $32 billion. Investors are sharpening their focus on technology-enabled assets that drive analytics, workforce optimization, and platform solutions. The trend underscores a shift from pure “beds and buildings” to investments that digitize and optimize care delivery.

3. Medtech: The New Growth Engine

Medtech is having a moment. Deal value nearly doubled year-over-year to ~$33 billion, marking its arrival as a major force. Investors are applying proven PE playbooks—focusing on revenue growth, margin expansion, and multiple expansion—to often large-scale assets originating from public markets (via take-privates or carve-outs). The headline $18.3 billion take-private of Hologic by Blackstone and TPG exemplified this trend, accounting for over half the year’s medtech buyout value.

The Exit Landscape: Liquidity Returns with Force

The dramatic rebound in exits, especially in sponsor-to-sponsor deals, is a critical takeaway. This surge is driven by two factors:

- Dry Powder Deployment: Funds have capital to deploy for scaled, proven assets.

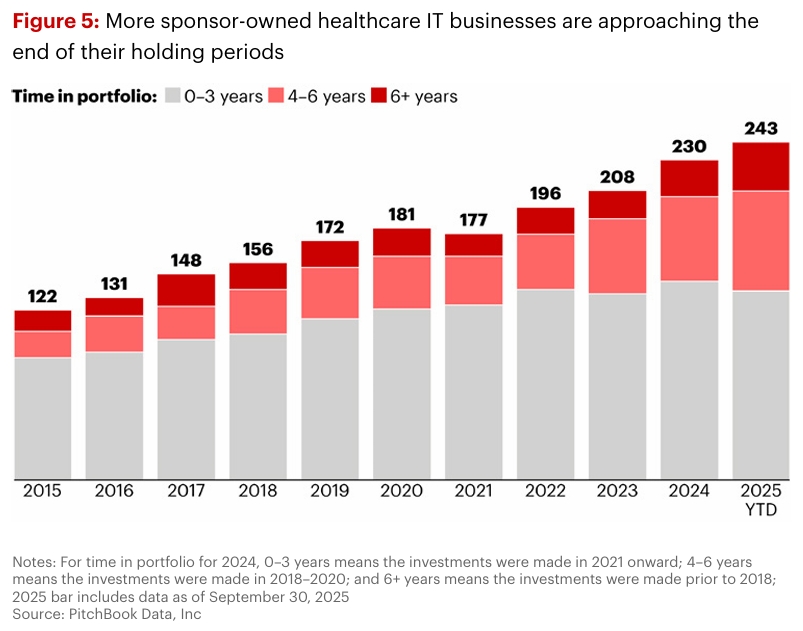

- Fund Life Cycles: A growing cohort of sponsor-owned assets are reaching the end of typical holding periods.

This dynamic creates a virtuous cycle of liquidity, enabling firms to return capital to Limited Partners (LPs) and reinvest in new platforms. The rise of public-to-private deals and carve-outs further diversifies the exit and entry pathways, offering flexibility in a complex market.

Part 2: What Differentiates Winning Healthcare IT Investments

Within the booming provider segment, Healthcare IT (HCIT) stands apart as a perennial high-performer. However, high valuation multiples and competitive auctions mean that success is no longer guaranteed by simply riding sector tailwinds.

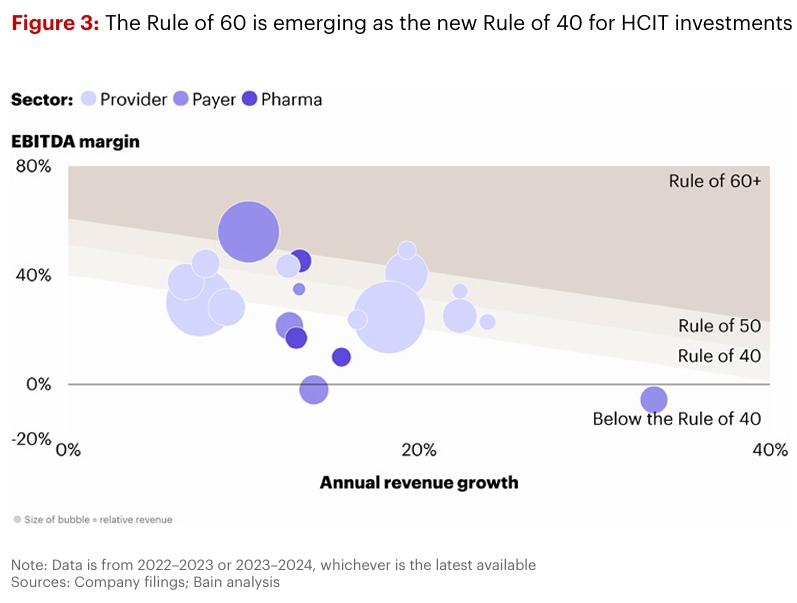

The New Benchmark: The “Rule of 60”

Historically, software companies aimed for the “Rule of 40” (revenue growth % + EBITDA margin % > 40). In top-performing HCIT, the bar has been raised to the “Rule of 60”. Achieving this requires a disciplined, proactive approach to value creation from day one.

The Modern HCIT Value Creation Playbook

Winning investors are underwriting deals with specific, actionable value-generation strategies already in the base-case scenario. Key levers include:

- Generative AI as a Dual-Edged Sword: AI is no longer speculative. It’s a core tool for driving revenue (through new products) and reducing costs (by streamlining back-end processes). However, it also presents a defensive imperative; incumbents must integrate AI or risk displacement by AI-native disruptors.

- Sophisticated Pricing & Packaging: Moving beyond simple price hikes to developing comprehensive programs that drive upsell through feature bundling and value-based pricing models.

- Strategic M&A for Synergy: Using acquisitions not just for add-on tuck-ins, but for building synergistic platforms that create defensible moats and accelerate growth.

- Go-to-Market Expansion: Implementing data-driven upsell and cross-sell strategies to maximize revenue from existing client relationships.

For financial leaders and partners, partnering with HCIT platforms means moving beyond financial engineering to operational partnership. They need embedding expertise in pricing strategy, AI integration roadmaps, and M&A synergy realization to help portfolio companies hit this new “Rule of 60” standard.

Part 3: New Models of Value Creation for Physician Groups

Investment in physician groups, particularly in the US, has evolved past the simple “buy-and-build” roll-up model. While deal volume has moderated from 2021 peaks, the strategy has matured, demanding greater operational sophistication.

From Confederation to Integrated Platform

The winning model now involves transforming loose affiliations of practices into scaled, integrated platforms. The goal is to create a supportive “center” that provides clinicians with the tools, technology, and administrative relief needed to thrive, thereby improving retention and care quality.

Five Pillars of Modern Physician Group Value Creation:

- Enhance the Clinician Experience: Define a compelling value proposition for doctors, reducing burnout and making the platform an employer of choice.

- Optimize Core Operations: Leverage technology to improve patient engagement, referral management, and overall practice productivity.

- Expand Care Delivery Models: Move into alternative payment models (value-based care) and strategically add ancillary services (imaging, labs, surgery centers).

- Execute Disciplined Growth: Develop a repeatable playbook for geographic and service-line expansion, with a clear plan for integration.

- Reinforce with AI & Analytics: Deploy AI-enabled tools to optimize revenue cycle management, front/back-office operations, and clinical decision support.

Selective Opportunities in a Mature Market

Despite headwinds, pockets of high potential remain for investors with deep sector knowledge:

- Specialty Pharmaceuticals: Managing the cost and complexity of high-price drugs in specialties like oncology, neurology, and urology.

- Value-Based Care Pioneering: Specialties like orthopedics and cardiology are ripe for bundled payment models.

- Strategic Ancillary Expansion: Owning or aligning with diagnostic and ancillary services in dermatology or gastroenterology.

- Fragmentation Play: Continuing consolidation in still-fragmented specialties like nephrology and neurology.

The physician group opportunity today rewards operational excellence and clinical alignment as much as financial leverage and scale.

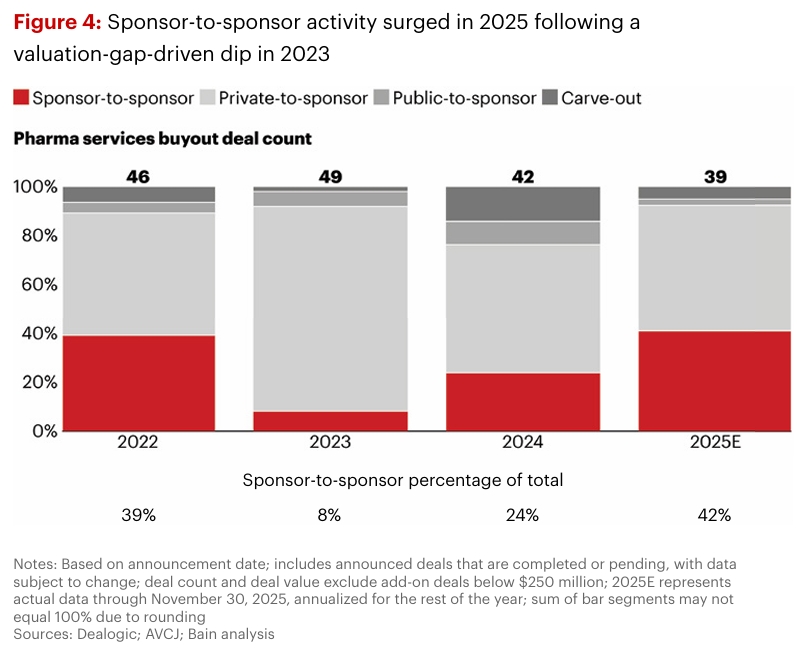

Part 4: Playing the Long Game in Pharma Services

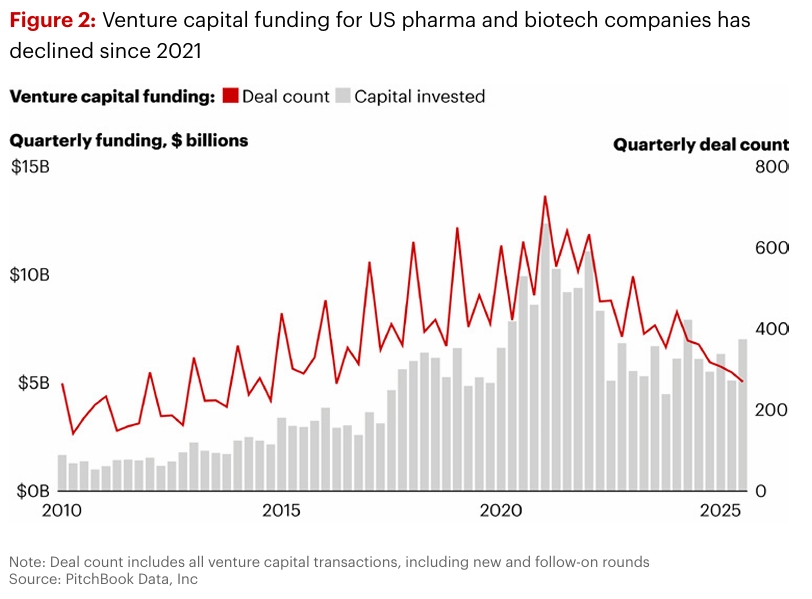

The pharma services sector (CROs, CDMOs) faces a more complex environment after years of robust growth. While long-term tailwinds remain, recent headwinds—biotech funding normalization, policy uncertainty, and valuation gaps—require a more selective, value-focused approach.

Navigating Current Headwinds

Investors are adapting through several key strategies:

- The Barbell Approach: Targeting either (a) scaled, premium “gem” assets with clear differentiation, or (b) sub-scale platforms with significant potential for operational improvement.

- Seeking Insulation: Prioritizing businesses with revenue visibility (long-duration programs), customer exposure to large pharma (vs. volatile biotech), and limited exposure to cross-border policy shocks.

- Structured Value Creation Playbooks: Developing rigorous, scenario-tested plans focused on top-line growth, AI-driven efficiency, and strategic M&A to gain investment committee conviction in a shaky macro climate.

The record $5 billion+ investment in PCI Pharma Services and strategic acquisitions like Thermo Fisher’s purchase of Clario demonstrate that for the right assets—those with scale, quality, and operational upside—capital and strategic interest remain fervent.

Conclusion and Outlook: Strategic Imperatives for 2026 and Beyond

Bain’s healthcare private equity report concludes with a cautiously optimistic outlook for 2026. It set against several key questions that will shape the market:

- Sustainability: Can Europe maintain its momentum, and will North America see sustained performance across all quarters?

- Tech Evolution: What’s the next act for Healthcare IT and Generative AI? Will pharma IT accelerate?

- Biopharma Cycle: With macro pressures potentially easing, will biopharma M&A open up, reshaping the global ecosystem?

- Value Creation Mastery: How will investors refine their playbooks to deliver outsized returns in a more competitive, selective environment?

For Business Partners and the investors we work with, the implications are clear:

- Value Creation is King. Success hinges on having a detailed, operational plan from diligence to exit, especially in hot sectors like HCIT and Medtech.

- Operational Partnership is Essential. Translating financial strategy into on-the-ground operational improvement in areas like pricing, AI integration, and clinician engagement is the new differentiator.

- Selectivity and Insight are Critical. In a market of both record volumes and clear headwinds (as in pharma services), deep sector insight to identify “gem” assets and resilient business models is paramount.

- Prepare for Liquidity. With exit pipelines building and portfolios aging, having assets “exit-ready” with a clear story of operational transformation will be crucial to capturing value.

The 2026 healthcare private equity landscape is one of immense opportunity tempered by increased complexity. The firms that will thrive are those that combine financial acumen with transformative operational expertise, turning strategic acquisitions into engines of sustainable growth and innovation. The record has been set, and the race for the future of healthcare investment is on.

🔗 Links for More:

For a deeper analysis of the data and regional insights, download the full “Global Healthcare Private Equity Report 2026” from Bain website or NeoForm LinkedIn page.

📌 About NeoForm:

At NeoForm Business Partners, we help private equity firms and their portfolio companies navigate complexity, build value, and achieve extraordinary results through financial transformation.

Visit our blog for more insights on M&A, private equity, private debt and private markets.

🔗 Related Readings:

- Midyear Private Equity Report 2025 by Bain

- McKinsey Global Private Markets Report 2025

- Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment

- Healthcare Private Equity Trends in 2025 from Bain Report

- The Future of Investing: Private Markets and Credit in 2025

Need tailored solutions? Explore NEO Services or contact our partners to learn how our expertise can help you to elevate and execute your private equity strategies from value creation planning to exit readiness.