Healthcare Private Equity in 2025: A Year of Megadeals and Strategic Shifts

The Bain & Company Global Healthcare Private Equity Report 2025 reveals a dynamic landscape marked by surging deal values, evolving investment strategies, and shifting regional opportunities. Despite macroeconomic challenges, private equity (PE) firms are capitalizing on innovation, carve-outs, and emerging markets to drive returns.

Here’s a breakdown of the key trends shaping healthcare private equity this year:

Healthcare Private Equity Market 2024: Year in Review and Outlook

2024 was a strong but selective year for healthcare PE, with biopharma and healthcare IT leading growth while traditional provider deals lagged. Looking ahead, mid-market innovation, carve-outs, and Asia-Pacific diversification will be critical for success.

For investors:

Focus on sector specialization, operational value creation, and early due diligence to navigate this evolving market.

1. 2024: A Strong Year for Healthcare PE Despite Macro Challenges

Record-Breaking Deal Activity

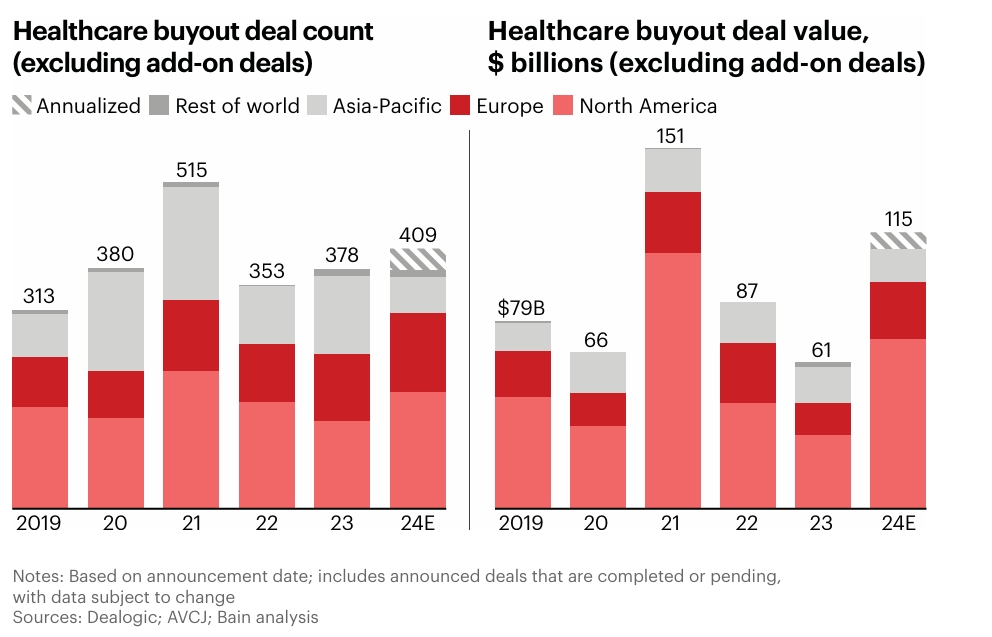

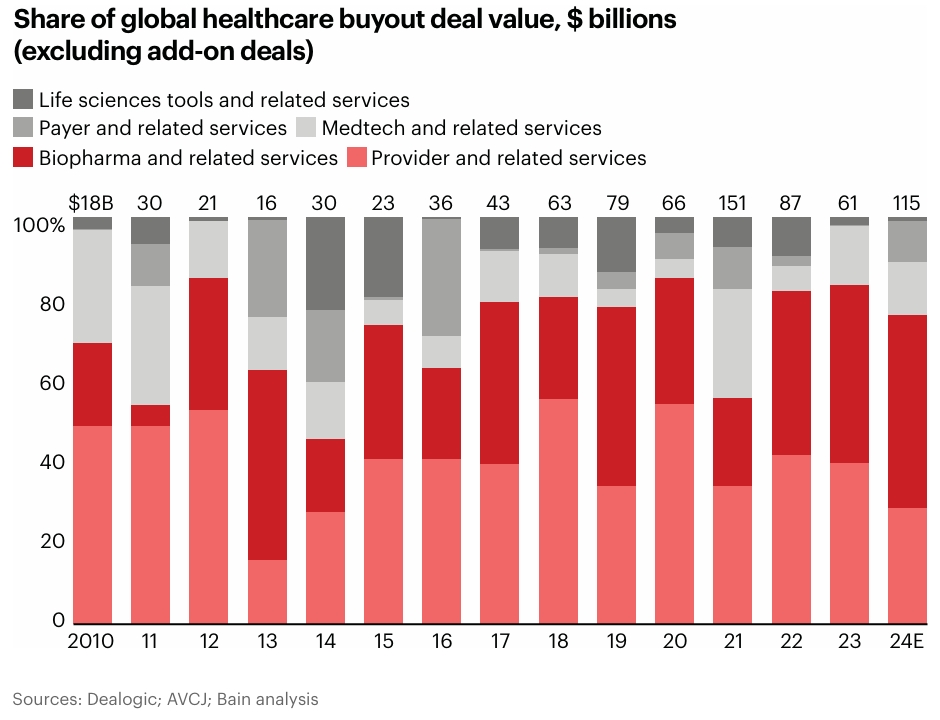

- Global healthcare PE deal value reached $115 billion, making it the second-highest year on record (just below the 2021 peak).

- Megadeals dominated, with five transactions exceeding $5 billion (compared to just two in 2023).

- Notable deals:

- Novo Holdings’ $16.5B acquisition of Catalent (to boost GLP-1 manufacturing).

- Sanofi’s $17.3B carve-out of its consumer health business (Opella).

- Notable deals:

- North America remained the largest market (65% of deal value), followed by Europe (22%) and Asia-Pacific (12%).

Regional Highlights

- North America & Europe surged, offsetting a 49% decline in Asia-Pacific deal volume (mainly due to China’s slowdown).

- Europe saw record-high deal volume, surpassing its 2021 peak, led by biopharma and medtech.

2. Sector Breakdown: Biopharma & Healthcare IT Lead, Provider Struggles

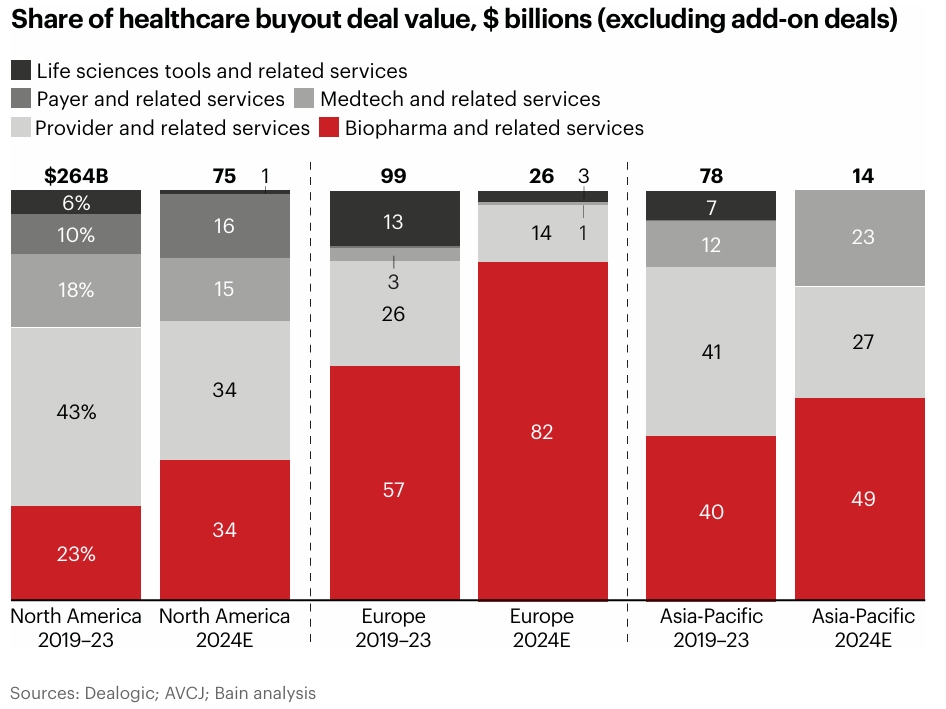

Biopharma & Life Sciences (43% of Deal Value)

- Key drivers:

- Clinical trial IT infrastructure (e.g., GI Partners’ investment in eClinical Solutions).

- Manufacturing expansion (e.g., Catalent acquisition for GLP-1 drug production).

- Challenges:

- Bid-ask spread issues (sellers’ high price expectations vs. buyers’ caution).

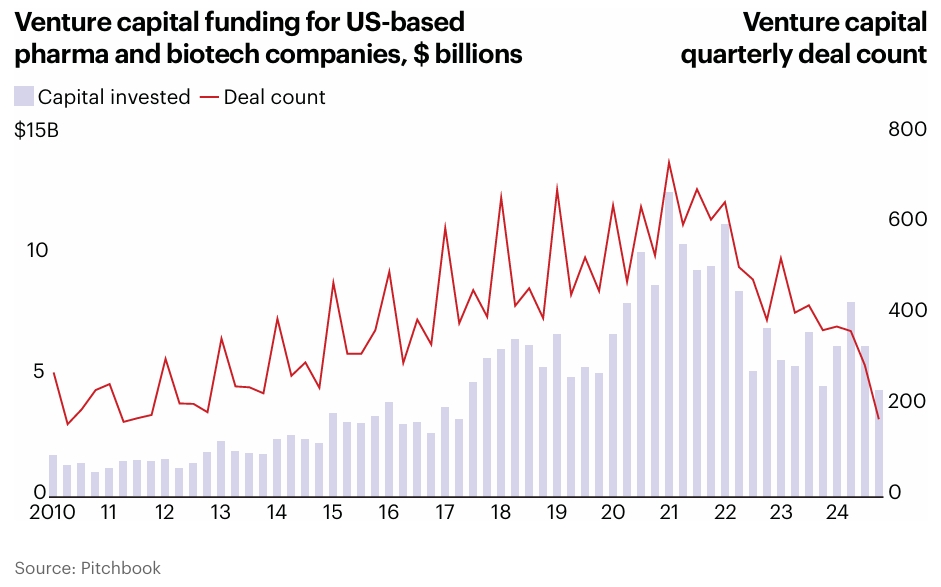

- Declining biotech VC funding (impacting R&D spending).

Healthcare IT Rebounds

- Deal activity rebounded after a 2023 slump, driven by:

- Providers’ need for efficiency (e.g., TPG’s acquisition of Surescripts).

- Payers investing in advanced analytics (e.g., Cotiviti’s $11B recapitalization).

- Biopharma’s push for digital trial optimization (e.g., EQT’s acquisition of CluePoints).

- Generative AI is a growing focus, but few pure AI deals have materialized yet.

Provider Sector Hits a Decade Low

- Share of deal value fell to its lowest in 10 years, particularly in Asia-Pacific.

- Europe’s provider deals were limited due to regulatory fragmentation and operational complexity.

3. Key Trends Reshaping the Market

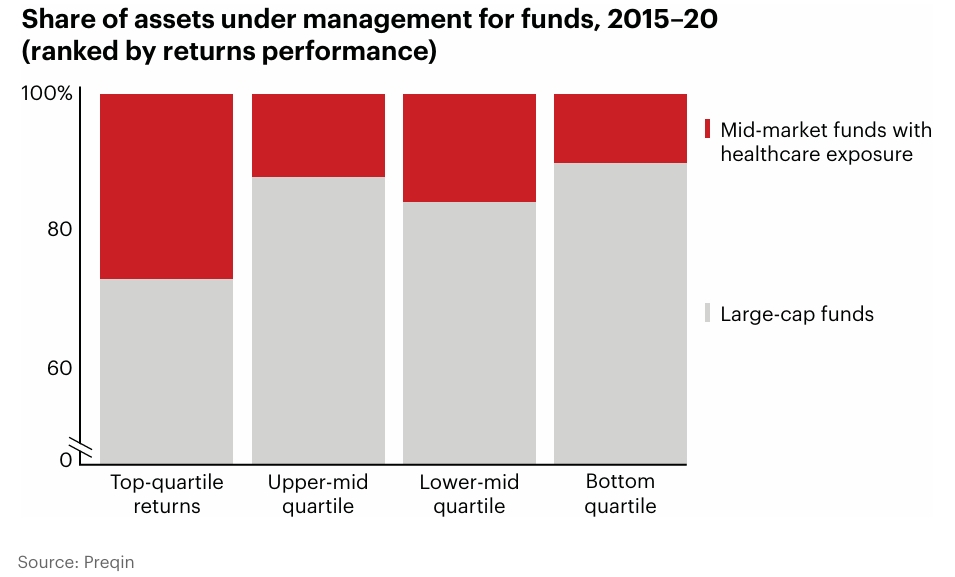

1. Mid-Market Funds Outperform

- Smaller funds ($500M–$4B AUM) delivered higher returns than large-cap peers.

- Shift from traditional provider deals to healthcare IT & biopharma services.

2. Carve-Outs Gain Traction

- Public companies divested non-core assets to streamline operations (e.g., Sanofi’s Opella sale).

- PE firms see carve-outs as high-value opportunities, with IRRs ~20% higher than typical buyouts.

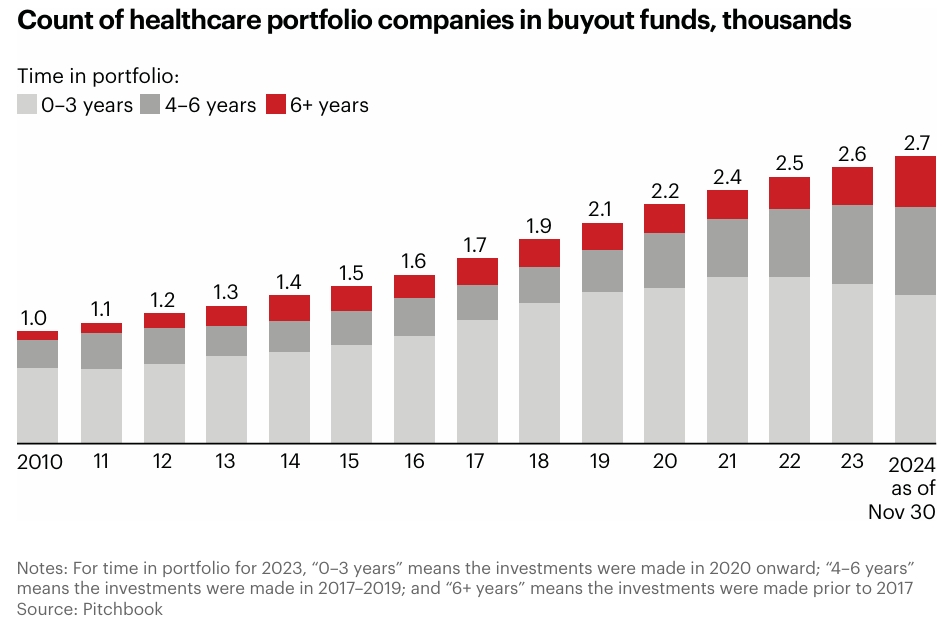

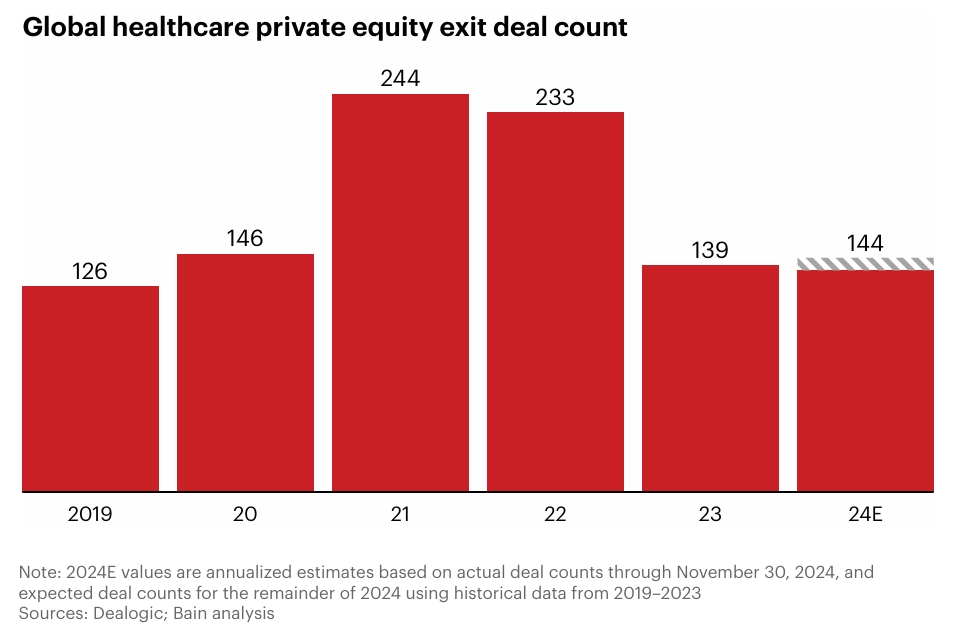

3. Exit Challenges Persist

- Exit volumes dropped 41% from 2021 peaks due to:

- High interest rates reducing multiple expansion.

- Bid-ask misalignment (sellers want 2021 valuations; buyers are cautious).

- Sellers must now prove value creation with data-backed equity stories.

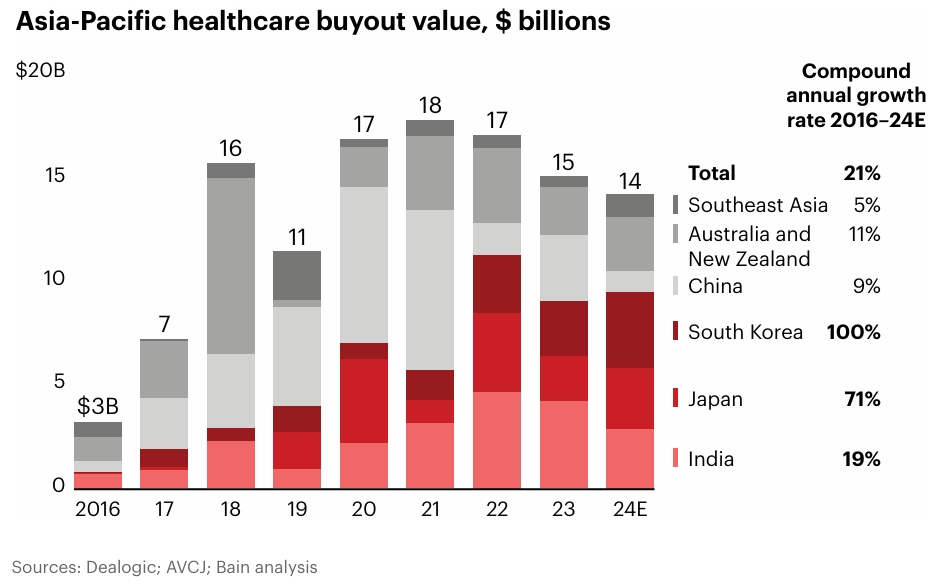

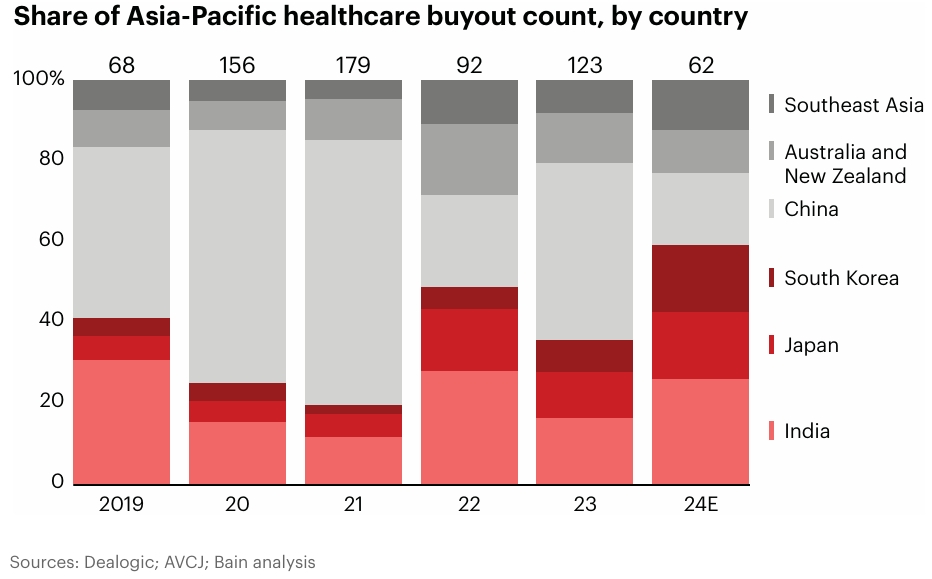

4. Asia-Pacific’s Shifting Landscape

- China’s slowdown redirected investments to India, Japan, and South Korea.

- India emerged as the largest market by volume (26% of Asia-Pacific deals), driven by hospital chains and CDMOs.

4. Outlook for 2025 & Beyond

Opportunities

- Biopharma rebound if biotech funding improves.

- More carve-outs as corporates continue portfolio optimization.

- Healthcare IT & AI adoption accelerating across payers, providers, and life sciences.

Risks

- Macroeconomic uncertainty (interest rates, inflation).

- Regulatory changes (e.g., US election impact on healthcare policy).

- Sponsor-to-sponsor deal recovery remains slow.

Why Mid-Market Healthcare Private Equity Firms Are Outperforming

Mid-market healthcare PE firms thrive by:

✅ Pivoting to resilient sub-sectors (IT, services, biopharma).

✅ Combining sector expertise with operational rigor.

✅ Adapting value-creation strategies beyond simple add-ons.

For Investors: Allocate to mid-market funds for higher returns and downside protection in volatile markets.

For GPs: Double down on differentiated expertise and pre-deal value planning to sustain outperformance.

1. Mid-Market Funds Outperform Large-Cap Peers

Stronger Returns & Consistent Deal Activity

- Top-quartile mid-market healthcare funds significantly outperformed large-cap funds.

- Deal volume remained steady despite broader market slowdowns (e.g., Webster Equity Partners’ successful exit from Retina Consultants of America).

- Fundraising surged by ~40% from 2019–21 to 2022–24, reaching $59B, signaling strong LP confidence.

Key Takeaway: Mid-market firms combine agility, sector expertise, and innovative strategies to generate higher returns.

2. Shifting Investment Focus: From Providers to Derivatives & Biopharma

Decline in Traditional Provider Deals

- Historically, 55% of mid-market deals targeted providers (e.g., physician groups, hospitals).

- Post-2022, provider deals dropped due to labor shortages, reimbursement pressures, and operational challenges.

Rise of “Derivative” Investments

Mid-market firms pivoted to high-growth adjacencies, including:

- Healthcare IT: Revenue cycle management (RCM), patient engagement platforms (e.g., Altaris’ acquisition of Sharecare).

- Provider Services: Staffing (e.g., Knox Lane’s buyout of All Star Healthcare Solutions), lab services, supply chain tech.

- Biopharma & Medtech: Contract research organizations (CROs), compliance/testing tools, clinical trial IT (e.g., WindRose’s acquisition of SubjectWell).

Why It Worked: These segments offer recession-resistant cash flows and address pressing industry pain points (e.g., hospital cost pressures).

3. Biopharma & Medtech: A Growing Opportunity

Niche Expertise Drives Deals

- Mid-market firms avoided bid-ask spread issues by targeting founder-owned businesses and specialized assets.

- Investments shifted from pure biopharma products to enabling services:

- Clinical trial IT (e.g., GI Partners’ acquisition of eClinical Solutions).

- Commercialization support (e.g., CDMOs, regulatory compliance tools).

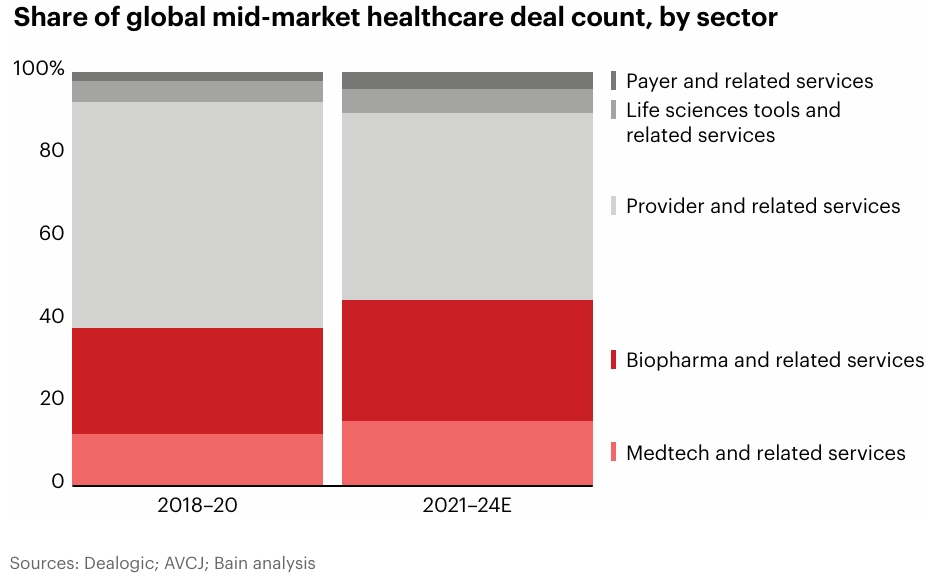

Data Point: By 2024, IT and services made up 61% of mid-market biopharma deals, up from 47% in 2018.

4. Evolving Value-Creation Strategies

Moving Beyond “Buy-and-Build“

While tuck-in acquisitions still matter, mid-market firms now emphasize:

- Operational Synergies

- Centralizing back-office functions (e.g., billing, procurement) for physician practices.

- Expanding ancillary services (e.g., ambulatory surgery centers for cardiology groups).

- Tech & AI Integration

- Deploying generative AI to reduce “tech debt” in healthcare IT platforms.

- Value-Based Care (VBC) Pilots

- Experimenting with risk-sharing models, though success varies by specialty.

Sector-Specific Playbooks

- CROs/CDMOs: Added new capabilities (e.g., advanced materials, injection molding).

- Healthcare IT: Scaled product suites (e.g., adding analytics to RCM platforms).

5. Future Challenges & Competitive Edges

Risks Ahead

- Macro pressures (higher interest rates, LP liquidity demands).

- Increased competition as more funds target niche healthcare segments.

How Mid-Market Firms Can Stay Ahead

- Deepen Sector Expertise

- Hire specialists (e.g., clinicians, regulatory experts) for biopharma/medtech deals.

- Prioritize Pre-Exit Value Creation

- Document EBITDA growth levers early to justify valuations.

- Leverage AI & Data

- Use predictive analytics to identify untapped synergies in portfolio companies.

Carve-Outs in Healthcare Private Equity: Unlocking Value in a Competitive Market

- 2025 deal flow will remain strong as corporates continue portfolio pruning.

- Asia-Pacific carve-outs rising: Multinationals spin off local units (e.g., UCB Pharma’s China divestiture).

Investor Takeaways

✅ Target corporate sellers with “non-core” labels – these often have untapped potential.

✅ Budget 20–30% more for separation costs than traditional buyouts.

✅ Pre-negotiate TSAs to minimize post-close operational friction.

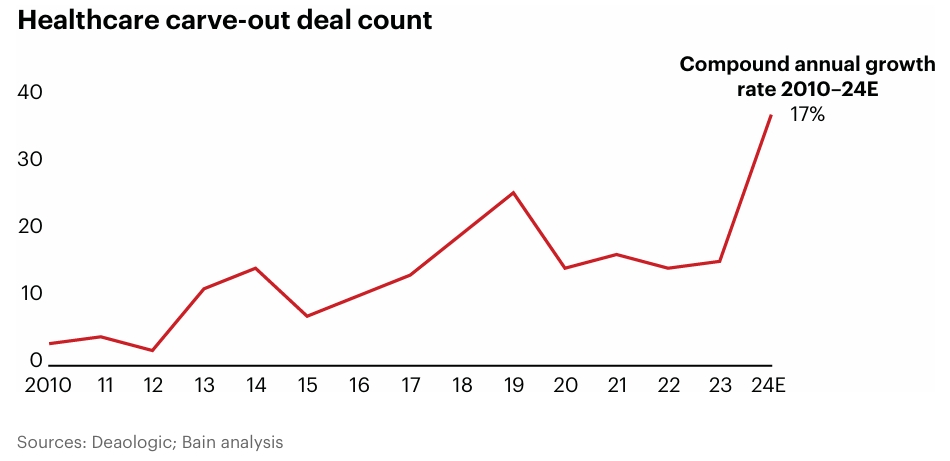

1. The Rise of Healthcare Carve-Outs

Market Dynamics Driving Growth

- 17% CAGR in carve-outs since 2010, with a notable rebound in 2024 after a 2023 dip.

- Declining sponsor-to-sponsor deals (-30% since 2022) pushed PE firms toward corporate divestitures.

- Public companies under pressure to streamline operations and boost shareholder returns.

Key Drivers:

- Strategic refocusing: Large healthcare corporates (e.g., Sanofi, Baxter) divested non-core assets to improve growth metrics.

- PE appetite for undervalued assets: Carve-outs often come with built-in operational upside.

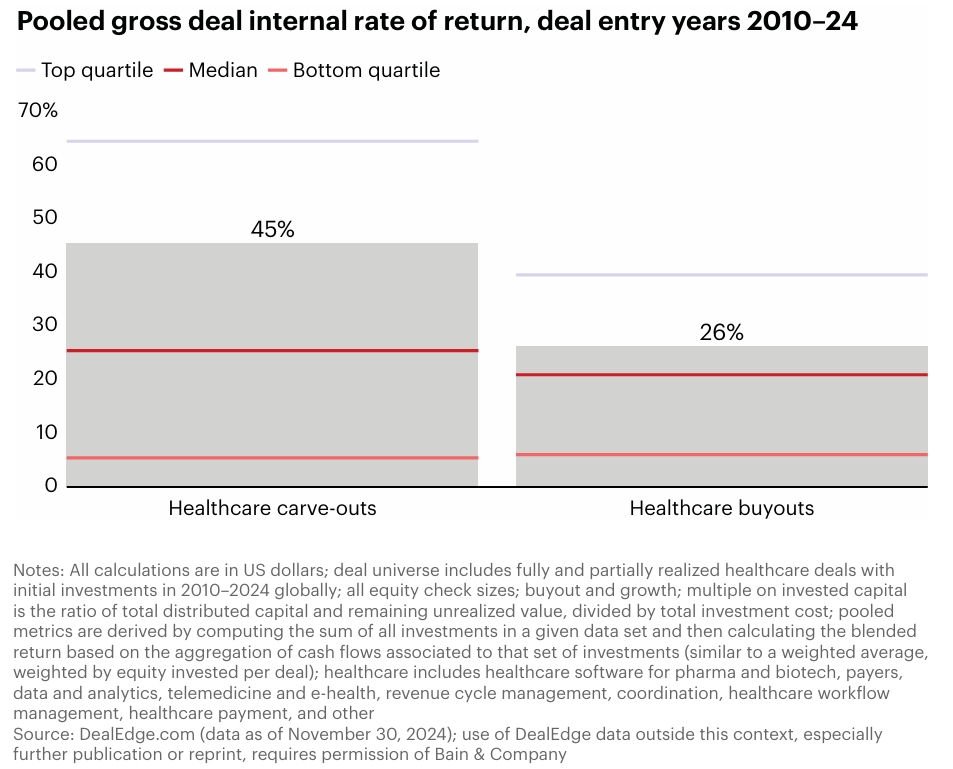

2. Why Carve-Outs Deliver Superior Returns

Performance Benchmarks

- Top-quartile carve-outs generate ~20% higher IRR than traditional buyouts.

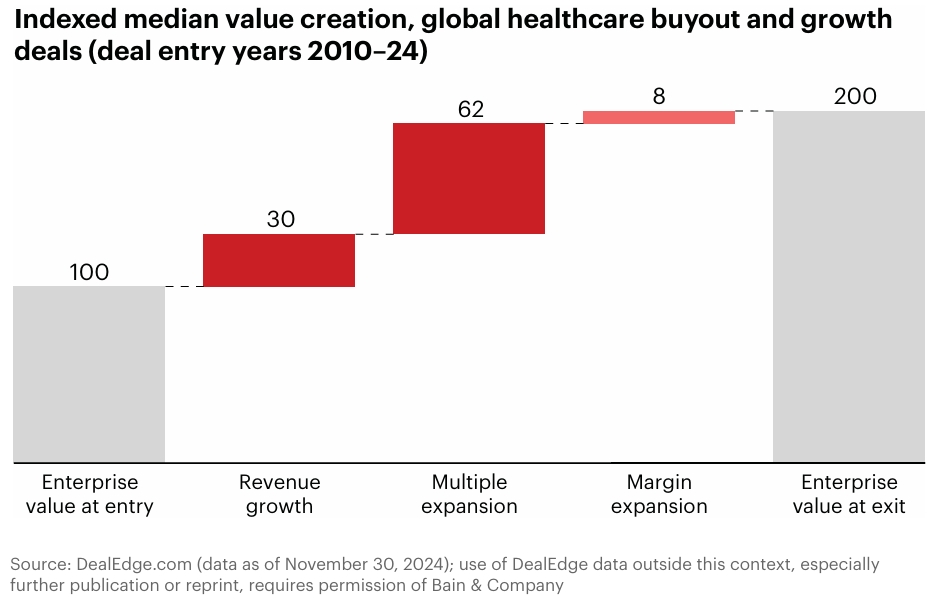

- Value creation levers:

- Revenue growth (62% of value): Removing “corporate drag” unlocks commercial potential.

- Multiple expansion (30%): Standalone entities command higher valuations.

Case Studies: Successful Carve-Outs

- KKR’s IVIRMA Global + Eugin Group (Fresenius SE)

- Fertility sector consolidation: Combined entity created a global leader in IVF.

- Synergies: Centralized R&D and expanded into new markets.

- Carlyle’s Vantive (Baxter Kidney Care Unit)

- Shift to peritoneal dialysis: Carlyle’s expertise accelerated digital transformation.

- Debt reduction for Baxter: Freed capital for core business reinvestment.

3. The Carve-Out Advantage for Sellers & Buyers

For Corporate Sellers

- TSR boost: Revenue growth drives 7–9x more shareholder value than margin improvements in medtech/pharma (see Figure 4).

- Portfolio rationalization: Sanofi’s $17.3B Opella divestiture allowed focus on innovative drugs.

For PE Buyers

- Hidden value potential: Carved-out units often suffer from:

- Underinvestment (e.g., outdated sales territories).

- Complexity (e.g., bloated SKUs, shared resource inefficiencies).

- Control premiums: Unlike minority stakes, full ownership enables rapid transformation.

4. Execution Challenges & Mitigation Strategies

Unique Complexities

- Day 1 readiness: Transitional service agreements (TSAs) delay operational control.

- Information asymmetry: Sellers know more about the asset than buyers.

- Talent retention risks: Key employees may flee during separation.

Bain’s 4-Point Playbook for Success

- Integrated Diligence

- Commercial + operational due diligence combined.

- Example: Map all shared services (IT, HR) to avoid post-close surprises.

- Separation Management Office (SMO)

- Dedicated team to oversee:

- IT systems migration (e.g., ERP separation).

- Customer/supplier contract transfers.

- Dedicated team to oversee:

- Talent Retention Plans

- Retention bonuses for critical staff.

- Fast-track leadership appointments.

- 100-Day Value-Creation Roadmap

- Quick wins: SKU rationalization, salesforce redesign.

- Long-term bets: Digital transformation (e.g., AI in medtech manufacturing).

5. Sector-Specific Opportunities

Biopharma/Medtech

- Equipment manufacturers: Ardian’s acquisition of Masco Group (biopharma water systems).

- CDMOs: Onshoring tailwinds in Europe.

Provider & Healthcare IT

- Revenue cycle management: CD&R’s purchase of R1 RCM.

- Clinical trial IT: Arsenal Capital’s Endpoint Clinical buy.

Maximizing Exit Value in Healthcare Private Equity: A Strategic Imperative

Key Takeaways For Sellers

- Begin exit preparation 2+ years in advance

- Shift from “multiple storytelling” to provable value creation

- Address 3-5 key diligence risks before going to market

For Buyers

- Price in operational improvements during bidding

- Secure management continuity early

- Model multiple scenarios for interest rate impacts

For LPs

- Reward funds with strong EVM capabilities

- Pressure GPs on hold period discipline

1. The Current Exit Landscape: A Market in Stalemate

Alarming Decline in Exit Activity

- Exit volumes down 41% from 2021 peak (see Figure 1)

- Average hold times reached record highs in 2024 (see Figure 2)

- Sponsor-to-sponsor deals declined most sharply, while strategic acquisitions gained share

Root Causes of the Slowdown

- Bid-Ask Spread Mismatch

- Sellers anchored to 2021 valuation multiples

- Buyers demanding discounts for higher financing costs

- Macroeconomic Headwinds

- Elevated interest rates (US 10-year at 4-5%) suppressing multiple expansion

- Reduced biotech VC funding impacting biopharma exits

- LP Liquidity Pressure

- Aging portfolios creating urgency for distributions

- $2.7T in unrealized PE value globally needing exit paths

2. The New Value Creation Imperative

The End of Multiple Expansion Reliance

- Historically, 46% of returns came from multiple expansion

- In current environment, operational improvements must drive 80%+ of returns

Four Pillars of Exit Value Maximization (EVM)

- Proven Value Creation Track Record

- Documented causal links between initiatives and EBITDA growth

- Example: Healthcare IT firm showing 30% attach rate for new AI module

- Articulated Future Runway

- Clear 3-5 year plan with quantified upside

- Example: Medtech platform outlining $50M synergy pipeline from tuck-ins

- De-Risked Commercial Story

- Customer case studies validating growth initiatives

- Example: Payer analytics firm with 12-month pilot results from 3 major insurers

- Operational Readiness

- Clean data room with auditable performance metrics

- Management team retention plan post-exit

3. The Seller’s Playbook: Preparing for Exit

12-24 Month Preparation Timeline

- Phase 1 (T-24 months): Conduct “reverse diligence” on asset performance

- Phase 2 (T-12 months): Develop equity story and address “deal killers”

- Phase 3 (T-6 months): Execute quick-win initiatives to demonstrate momentum

Critical EVM Tactics

- Commercial Due Diligence 2.0

- Map customer concentration risks

- Validate TAM expansion claims

- Operational Benchmarking

- Compare metrics to public comps

- Identify 100-300 bps of margin upside

- Talent Assessment

- Retain key personnel with stay bonuses

- Fill capability gaps pre-market

4. The Buyer’s Advantage: Value Creation Diligence

Pre-Close Preparation Framework

- Day 1 Readiness Plan

- Detailed 100-day roadmap

- Dedicated integration team

- Synergy Identification

- Cost: Shared services consolidation

- Revenue: Cross-selling opportunities

- Technology Blueprint

- IT separation costs

- AI deployment roadmap

Competitive Differentiators

- Baked-in value creation can justify higher bids

- Early management alignment reduces post-close friction

5. Sector-Specific Considerations

Biopharma Services

- Highlight clinical trial backlog

- Demonstrate R&D productivity gains

Provider Platforms

- Show same-store growth metrics

- Document payor contract improvements

Healthcare IT

- Prove product roadmap viability

- Quantify customer retention rates

6. Looking Ahead: The Path to Exit Recovery

Cautious Optimism for 2025

- Fed rate cuts may ease financing pressures

- Bid-ask gaps narrowing as seller expectations adjust

Critical Watch Factors

- Biotech funding environment

- Election impacts on healthcare policy

- Asia-Pacific deal flow recovery

Asia-Pacific Healthcare Private Equity: Emerging Opportunities in a Shifting Landscape

1. Asia-Pacific Healthcare PE: Market Overview

Deal Activity in 2024

- Deal value grew at 21% CAGR since 2016, reaching $20B in 2024.

- Volume declined 49% YoY, primarily due to:

- China’s slowdown (44% drop in deal count).

- Increased competition from strategic buyers (e.g., hospital chains, pharma consolidators).

Geographic Shifts

| Market | 2024 Highlights | Key Drivers |

|---|---|---|

| India | 26% of APAC deal volume | Rising middle class, $320B healthcare spend by 2028 |

| Japan | 20% CAGR since 2019 | Aging population, corporate governance reforms |

| South Korea | 26% of deal value (up 8pp) | Medtech innovation, regulatory easing |

| China | Strategic carve-outs dominate | Multinationals exiting non-core assets |

2. Country Deep Dives: Where Capital Is Flowing

India: The New Regional Leader

- Largest market by volume (26% share), resilient vs. APAC’s 49% decline.

- Top Sectors:

- Providers: Hospital chains (e.g., Blackstone’s Care Hospitals), clinics.

- Biopharma: CDMOs, generics (e.g., Advent’s $1.6B exit of BSV Group).

- Exit Multiples: Strong IPO/strategic sale activity (e.g., KKR’s $839M Healthium deal).

Japan: Aging Population Fuels Growth

- Key Trends:

- Senior care demand: 30% of population >65 years old (e.g., J-STAR’s Caregiver Japan buyout).

- Biopharma innovation: Partnerships with conglomerates (e.g., Takeda spin-offs).

- Governance Reforms: “Market checks” now required for M&A, creating carve-out opportunities.

South Korea: Medtech Hotspot

- Deal value surged to 26% of APAC total (vs. 18% in 2023).

- Notable Deals:

- Aesthetic devices: Archimed’s take-private of Jeisys Medical.

- Pharma distribution: MBK Partners’ acquisition of Geo-Young.

China: Strategic Carve-Outs Dominate

- Multinational exits: UCB Pharma’s neurology divestiture to Mubadala/CBC Group.

- Domestic focus: Local players consolidating hospitals and CROs.

3. Sector Trends: Where Investors Are Placing Bets

Biopharma & Related Services (40% of Deals)

- India: CDMOs/generics scaling for global markets.

- Japan: Pharma outsourcing (e.g., preclinical R&D firms).

Providers & Clinics (35% of Deals)

- India: Multi-specialty hospitals, digital health (e.g., Apollo 24/7).

- Australia: Aged care infrastructure assets coming to market.

Medtech (25% of Deals)

- South Korea: Aesthetic/dental devices with global demand.

- Japan: Robotics for senior care.

4. Future Outlook: Risks & Opportunities

Growth Catalysts

- India’s healthcare spend projected to grow 12% annually through 2028.

- Japan’s corporate reforms unlocking more PE-friendly deals.

- South Korea’s medtech export boom attracting global buyers.

Key Risks

- China’s economic recovery: Slower rebound could prolong capital reallocation.

- Regulatory hurdles: Foreign investment rules in sensitive sectors (e.g., Indian hospitals).

Investor Takeaways

✅ Diversify beyond China into India/Japan/South Korea.

✅ Target carve-outs of multinational subsidiaries.

✅ Focus on export-ready medtech in South Korea.

🔗 Links for More:

Download and read the full report on Bain website or from NeoForm LinkedIn page.

📌 About NeoForm:

NeoForm Business Partners helps investors and private equity firms to optimize their portfolio and invest in value creation business transformations through cutting-edge financial tools and frameworks. Visit our blog for more insights.

Want more insights on private equity markets? Explore Neo Services or contact our partners for tailored investment strategies.

🔗 Related Readings:

2 Comments

Midyear Private Equity Report 2025 by Bain - NeoForm Business Partners

[…] Healthcare Private Equity Trends in 2025 from Bain Report […]

McKinsey Technology Trends 2025: What Is Crucial to Align Your Business - NeoForm Business Partners

[…] Healthcare Private Equity Trends in 2025 from Bain Report […]

Comments are closed.