In the world of mergers and acquisitions (M&A), determining the final equity value of a business is a critical yet complex process. The ICAEW Corporate Finance Faculty’s best-practice guideline, Completion Mechanisms: Determining the Final Equity Value in Transactions, provides invaluable insights into how buyers and sellers navigate equity value adjustments to ensure fair and efficient deal outcomes.

At NeoForm Business Partners, we specialize in M&A advisory, helping businesses optimize their transactions. In this comprehensive guide, we break down the key concepts from the ICAEW report, offering actionable insights for dealmakers, CFOs, and investors.

List of Topics

- Introduction to Equity Value Adjustments

- Enterprise Value vs. Equity Value: Key Differences

- The Enterprise Value to Equity Value Bridge

- Cash-Free and Debt-Free Adjustments

- Normalized Working Capital Adjustments

- Completion Mechanisms: Completion Accounts vs. Locked Box

- Hybrid Mechanisms and Other Adjustments

- Accounting Warranties and Indemnities

- Closing Thoughts: Ensuring Fair and Efficient Transactions

1. Introduction to Equity Value Adjustments

When a buyer and seller agree on a headline price (enterprise value) for a business, the final consideration paid (equity value) often differs significantly due to adjustments for cash, debt, and working capital.

Why does this matter?

- Cash adjustments ensure the seller benefits from surplus cash left in the business.

- Debt adjustments prevent the buyer from inheriting undisclosed liabilities.

- Working capital adjustments account for fluctuations in operational liquidity.

Without standardized rules, disputes can arise, leading to delays, increased costs, or even failed deals. This guide explores best practices to mitigate such risks to reach final equity value in M&A deals.

2. Enterprise Value vs. Equity Value: Key Differences

Enterprise Value (EV)

- Represents the total value of a business, independent of its capital structure.

- Typically calculated as:

EV= Normalized EBITDA × Multiple EV

(e.g., £50m EBITDA × 10x multiple = £500m EV).

- The actual amount paid to shareholders after adjusting for:

- Cash (added to EV)

- Debt (subtracted from EV)

- Working capital surplus/shortfall (adjusted accordingly).

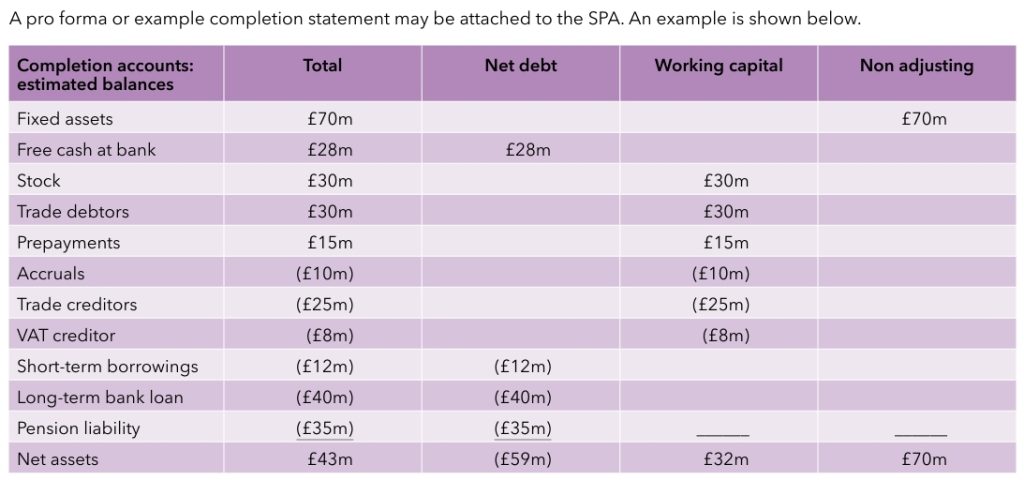

Example:

| Enterprise Value to Equity Value Bridge | |

| Enterprise Value (£50m × 10) | £500m |

| Plus: Cash | £20m |

| Less: Debt | (£80m) |

| Plus: Actual Working Capital | £60m |

| Less: Normal Working Capital | (£70m) |

| Working Capital Adjustment | (£10m) |

| Final Equity Value | £430m |

3. Cash-Free and Debt-Free Adjustments of Equity Value in M&A

Cash Adjustments: Free vs. Trapped Cash

- Free Cash: Readily available funds (e.g., surplus cash in bank accounts).

- Trapped Cash: Restricted funds (e.g., deposits, overseas cash with tax restrictions).

Key Considerations:

- Should cash-like items (e.g., tax losses, refundable deposits) be included?

- Buyers prefer excluding trapped cash, while sellers argue for maximum inclusion.

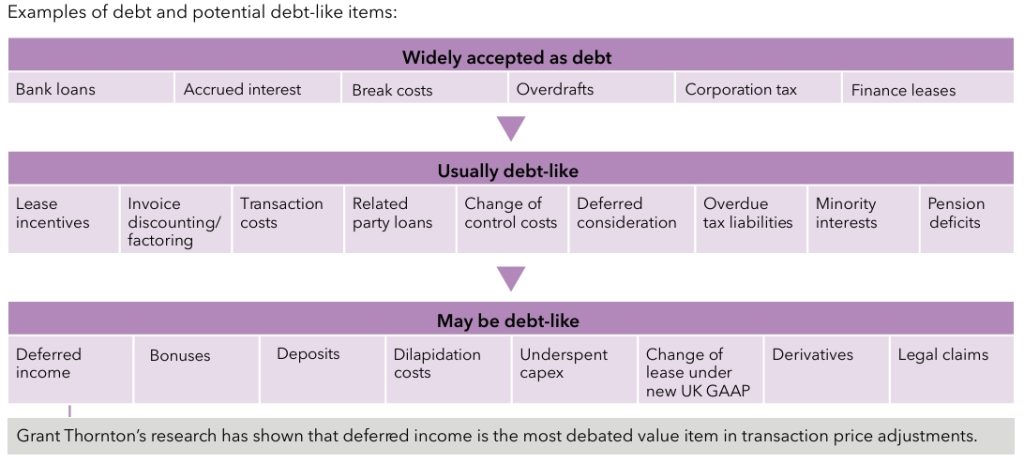

Debt Adjustments: What Counts as Debt?

- Traditional Debt: Bank loans, overdrafts, finance leases.

- Debt-Like Items: Liabilities not factored into EBITDA (e.g., deferred income, pension deficits).

Common Disputes:

- Deferred income (e.g., subscription-based businesses) is often contentious—should it be treated as debt or working capital?

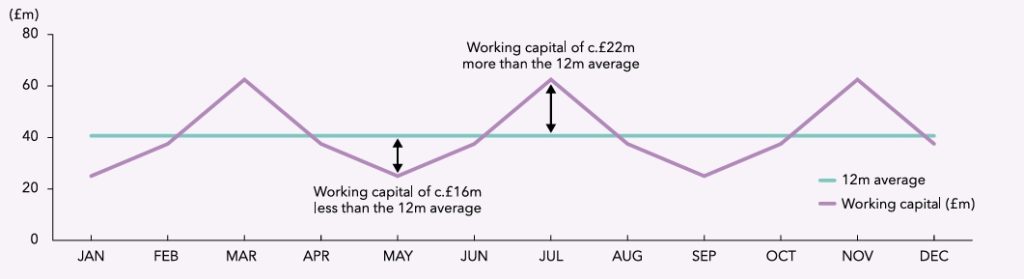

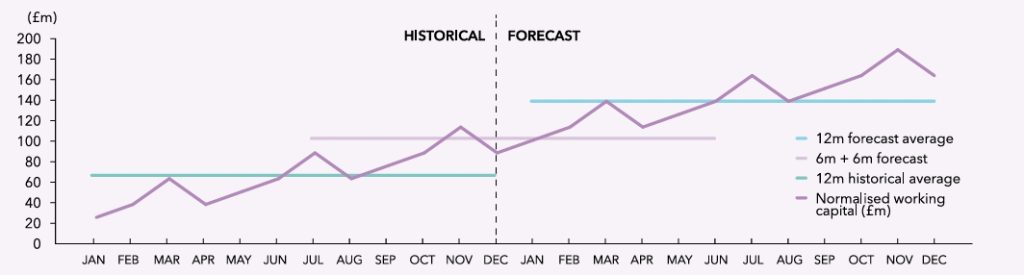

4. Normalized Working Capital Adjustments of Equity Value in M&A

Why Adjust Working Capital?

- Prevents sellers from artificially reducing working capital before completion.

- Ensures the buyer inherits a business with sustainable liquidity.

Defining “Normal” Working Capital

- Calculated as an average over a reference period (e.g., 12 months).

- Seasonal businesses may require tailored adjustments.

Example:

- If normal working capital = £40m but actual at completion = £24m, the buyer deducts £16m from equity value.

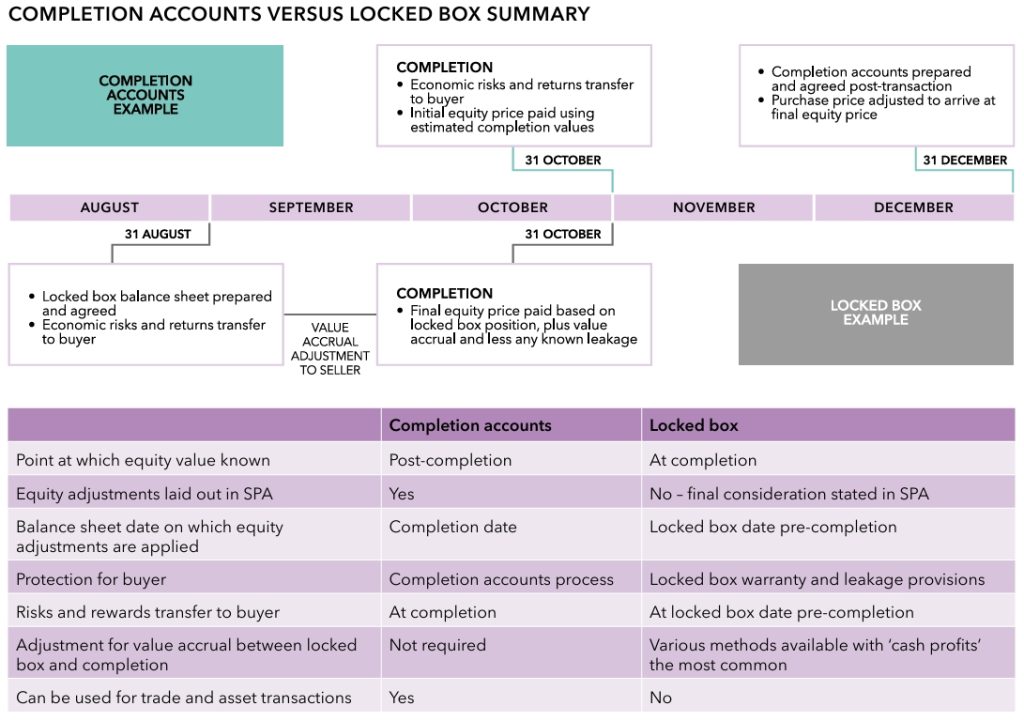

5. Completion Mechanisms: Completion Accounts vs. Locked Box

Completion Accounts

- Process:

- Initial payment based on estimated completion values.

- Post-completion, final accounts determine the true-up adjustment.

- Pros:

- Accurate reflection of the business’s financial position at completion.

- Cons:

- Time-consuming, prone to disputes (10% result in expert determinations).

Locked Box Mechanism

- Process:

- Equity value is fixed based on a pre-agreed balance sheet (the “locked box” date).

- No post-completion adjustments (reduces disputes).

- Key Features:

- Leakage Protection: Prevents sellers from extracting value between the locked box date and completion.

- Value Accrual: Adjusts for profits earned during the interim period (e.g., via “cash profits” method).

Comparison:

| Feature | Completion Accounts | Locked Box |

| Equity Value Known | Post-completion | At signing |

| Dispute Risk | High | Low |

| Best For | Complex deals | Competitive auctions |

6. Hybrid Mechanisms and Other Adjustments

Hybrid Approaches

- Combine elements of completion accounts and locked box to reach final equity value in M&A (e.g., using a locked box with a post-completion true-up for specific items).

Other Adjustments

- Retentions/Escrow: Funds held back to cover potential adjustments.

- Earnouts: Deferred payments tied to future performance (requires clear accounting policies to avoid disputes).

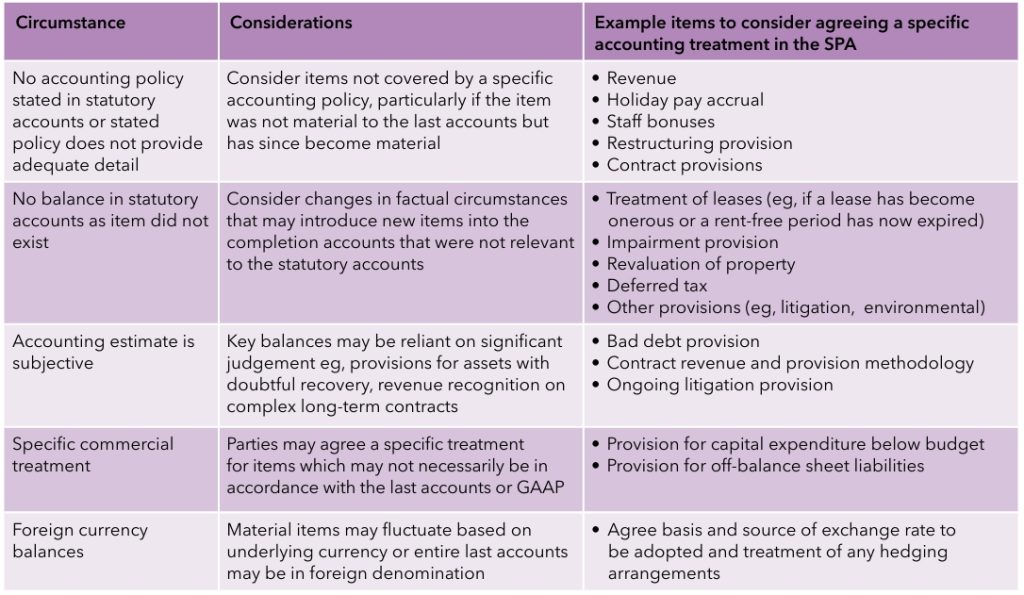

7. Accounting Warranties and Indemnities

Buyers seek warranties to protect against:

- Misstated financials.

- Undisclosed liabilities (e.g., tax, pensions).

- Material adverse changes post-signing.

Best Practices:

- Define accounting policies upfront.

- Disclose all known risks during due diligence.

8. Closing Thoughts: Ensuring Fair and Efficient Transactions

To reach final equity value in M&A, the ICAEW guidelines emphasize:

- Clarity: Agree on equity value adjustments early to avoid disputes.

- Flexibility: Choose the right mechanism (completion accounts vs. locked box) based on deal dynamics.

- Expertise: Engage M&A advisors to navigate complex adjustments.

Download and read full guide on ICAEW website or NeoForm LinkedIn page.

At NeoForm, we help businesses optimize their M&A transactions with data-driven insights and strategic advisory. Whether you’re a buyer or seller, understanding these mechanisms is crucial for a successful deal.

Need expert guidance on your next transaction? Contact NeoForm today.