Asset-Based Finance: The $6+ Trillion Private Credit Opportunity Hidden in Plain Sight

In the evolving landscape of private credit, one segment has grown with staggering speed and scale, yet often flies under the radar: Asset-Based Finance (ABF). While direct lending has dominated headlines, ABF has quietly become a multi-trillion-dollar engine of the global economy, offering institutional investors a compelling blend of attractive yields, diversification, and resilience.

At NeoForm, we believe understanding this powerful sub-asset class is crucial for building robust, future-proof portfolios. Drawing from a recent in-depth primer by KKR, let’s explore why ABF is an opportunity too big to ignore.

What Exactly is Asset-Based Finance (ABF)?

At its core, ABF is a form of credit investing where loans are secured by large, diversified pools of assets. This is a fundamental shift from traditional corporate lending.

Think of it this way: instead of lending based on a company’s future cash flows, you’re lending against the tangible value of existing assets. These assets fall into two main categories:

- Financial Assets: Pools of auto loans, consumer loans, accounts receivable, and residential mortgages.

- Hard Assets: Physical objects like airplanes, industrial equipment, and single-family rental homes.

- Contractual Assets: Cash-flow generating rights like music intellectual property (IP) and healthcare royalties.

In short, ABF provides the essential credit that allows businesses to finance equipment, consumers to buy cars and homes, and innovators to monetize their creations. It’s the hidden infrastructure of our modern economy.

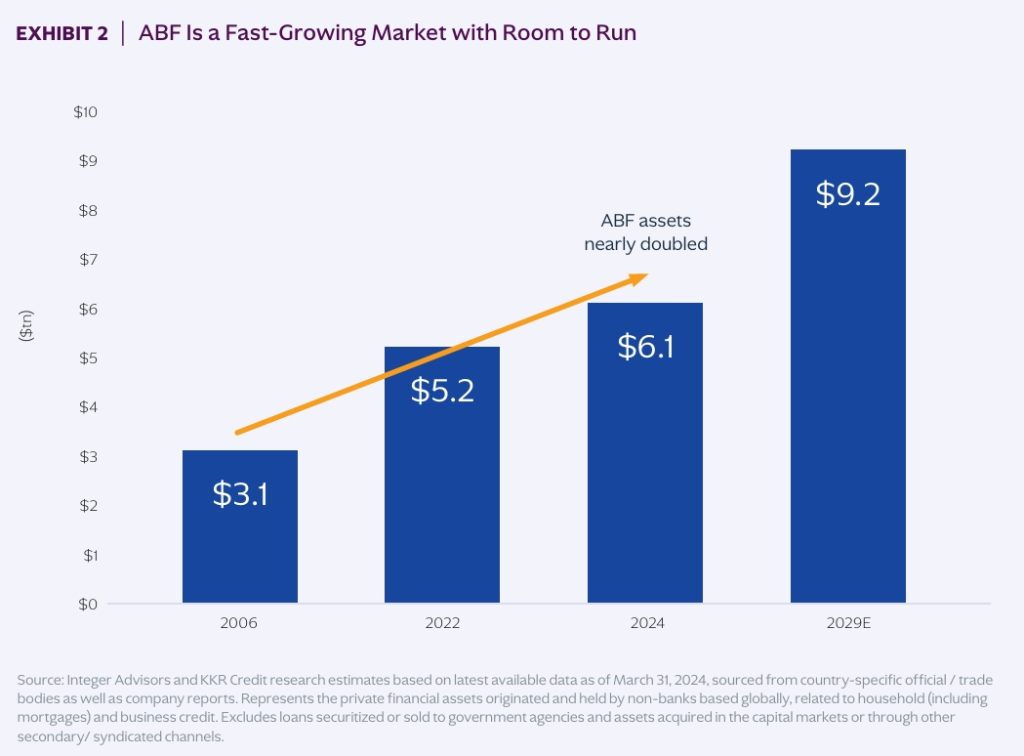

The ABF Market: Massive, Growing, and Underserved

The scale of the private global ABF market is breathtaking. Currently valued at over $6.1 trillion, it has nearly doubled since its pre-Global Financial Crisis peak. Even more impressive? KKR estimates it could reach $9.2 trillion by 2029—a figure larger than today’s syndicated loan, high yield bond, and direct lending markets combined.

Why is ABF growing so fast? The retreat of traditional banks is the primary catalyst. Post-GFC regulations, higher capital requirements, and widespread bank consolidation have created a massive lending void. As banks pull back, private, non-bank lenders like KKR are stepping in to meet the relentless demand for credit.

This trend accelerates during market dislocations. During the 2022 inflation spike and the 2023 regional banking crisis, private lenders saw their market share grow as their flexible capital became even more valuable to borrowers.

Why ABF Belongs in a Balanced Portfolio

For investors, ABF isn’t just about growth—it’s about strategic portfolio enhancement. Here’s how it adds value:

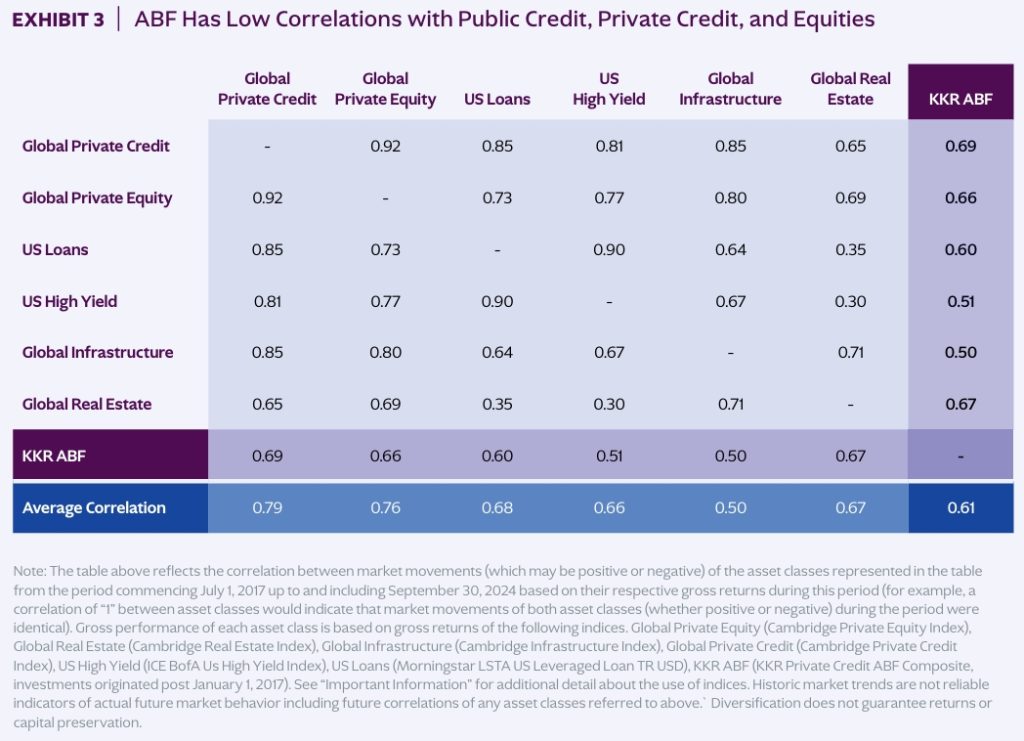

1. Superior Diversification

ABF offers one of the lowest average correlations to other major asset classes, including public fixed income, private equity, and even direct lending. This is because its performance is tied to the underlying assets (e.g., car loan repayments, aircraft leases) rather than corporate earnings cycles. Adding ABF genuinely diversifies your credit risk.

2. Built-In Inflation Protection

The value of the collateral backing ABF loans—particularly hard assets like equipment and real estate—tends to rise with consumer prices. This provides a natural hedge that is highly valuable in today’s economic environment.

3. Attractive, Stable Yields

The vast majority of ABF investments are fixed-rate, complementing the predominantly floating-rate nature of direct lending. This creates a balanced private credit portfolio that can perform across different interest rate cycles.

ABF vs. Direct Lending: A Crucial Distinction

While both are pillars of private credit, ABF and direct lending are fundamentally different. Combining them in a portfolio is a complementary strategy.

| Direct Lending | Asset-Based Finance (ABF) |

|---|---|

| Repayment Source: A company’s future operating cash flows. | Repayment Source: Cash flows from the underlying financial/hard assets. |

| Focus: Corporate creditworthiness. | Focus: Quality and diversification of the asset pool. |

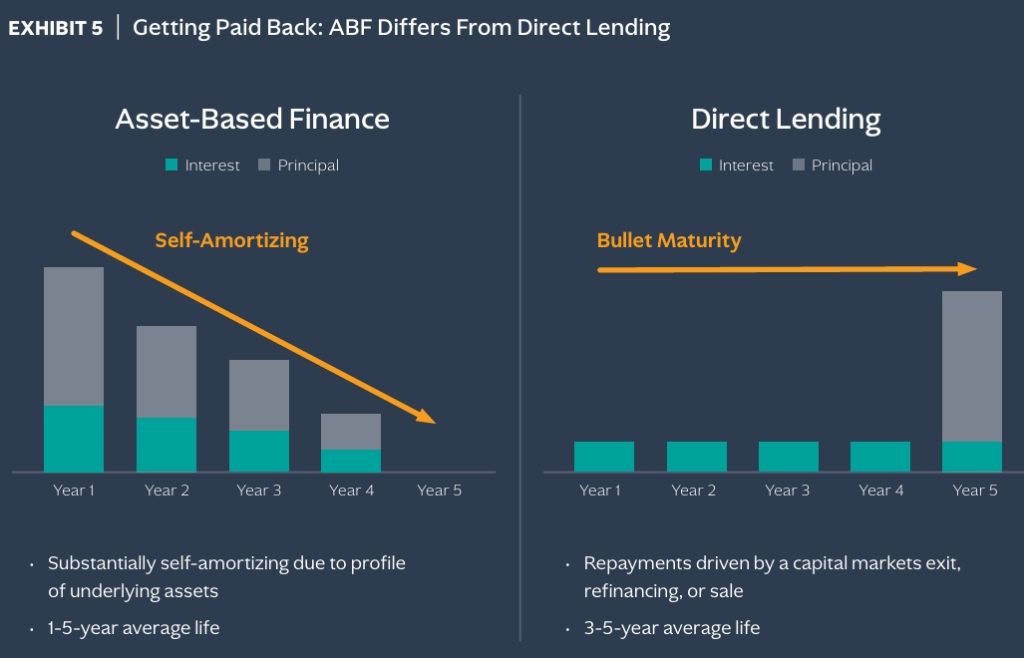

| Structure: Typically “bullet” maturity with interest-only payments and a large principal repayment at the end. | Structure: Self-amortizing, with front-loaded principal and interest payments, similar to a mortgage. |

This “self-amortizing” nature of ABF is a key benefit, providing investors with a steady return of capital throughout the investment’s life, reducing risk and enhancing liquidity profiles.

How Leading Managers Approach the ABF Market

Success in ABF requires scale, sophistication, and the ability to underwrite a wide range of complex assets. Leading firms “cast a wide net” across four key sub-sectors:

- Consumer & Mortgages: Financing prime auto loans, mortgages, and other consumer debt.

- Hard Assets: Supporting aircraft leasing, railcars, and single-family rentals.

- Commercial Finance: Providing equipment leases and lending against receivables for SMEs and large corporations.

- Contractual Cash Flows: Investing in royalty streams from music IP and healthcare.

This multi-pronged approach allows managers to find the most attractive, bespoke opportunities and build resilient, diversified ABF portfolios.

Conclusion: The Future of Credit is Asset-Based

Asset-Based Finance in private credit market is where direct lending was a decade ago: on the cusp of widespread adoption and recognition. As banks continue to retreat and the demand for flexible credit grows, ABF is poised to become a cornerstone of institutional portfolios.

It offers a rare combination: exposure to the vast, essential lending activities of the global economy, coupled with the benefits of diversification, inflation protection, and attractive, stable yields.

🔗 Links for More:

Read the full article on KKR website or NeoForm LinkedIn page.

📌 About NeoForm:

At NeoForm Business Partners, we specialize in identifying and accessing these transformative investment opportunities.

Visit our blog for more insights on private credit, equity and markets.

🔗 Related Readings:

- Credit Market Outlook 2025: Rising Private Credit and Asia-Pacific

- McKinsey Global Private Markets Report 2025

- The Future of Investing: Private Markets and Credit in 2025

- Midyear Private Equity Report 2025 by Bain

- Private Equity Market Trends in 2025: A Year of Recovery and Strategic Shifts

Looking to deepen your allocation to private markets? Explore how NeoForm Services can help you build a smarter, more resilient portfolio. Contact us today.