Global M&A Trends 2025 Summary:

The global M&A market in 2024 saw dealmakers adapting to continued headwinds, with deal value significantly below historical highs as a percentage of global GDP. However, 2024 marked a reversal of a two-year decline in deal volume and an increase in deal value compared to 2023. Looking ahead to 2025, Bain & Company is optimistic, anticipating M&A and divestitures to be crucial tools for companies. They can navigating technological disruption, a shifting global economy, and evolving profit pools. Key global trends for 2025 include a potential rebound driven by regulatory shifts, the increasing adoption of generative AI in the deal process, and strategic adjustments in various industries to address specific challenges and opportunities. Companies need to refine their M&A strategies, assess geographic footprints, and leverage technology for improved diligence and value realization.

1. Global M&A Market Trends in 2024: Adaptation Amidst Headwinds

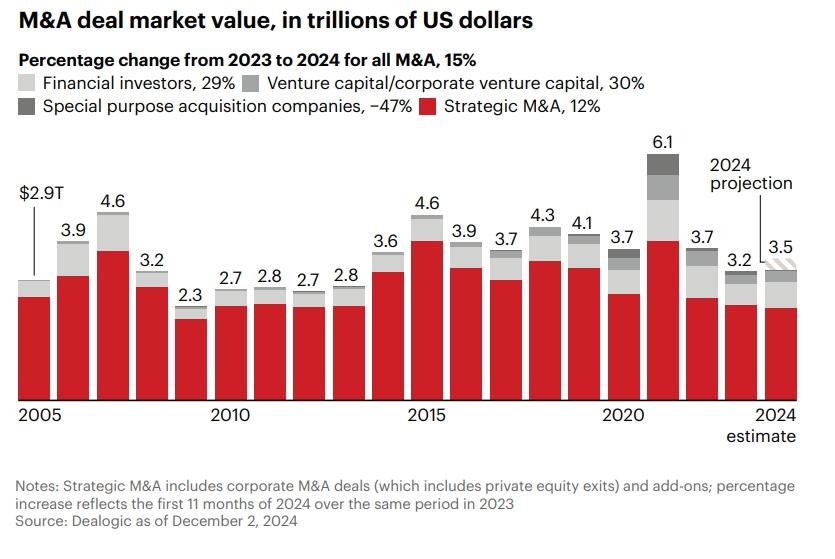

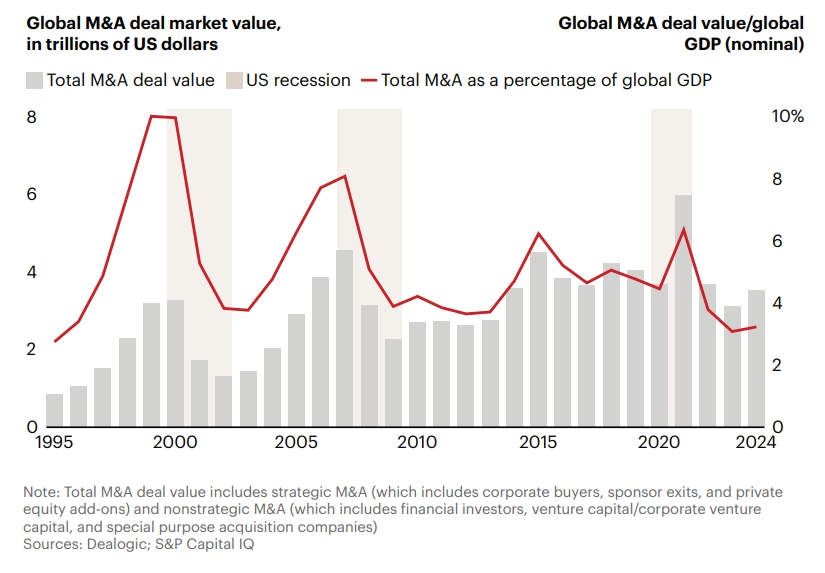

- Low Deal Value Relative to GDP: 2024 continued a three-year trend of global M&A deal value lingering at nearly 30-year lows as a percentage of nominal GDP. This indicates a cautious market environment.

- Reversal of Declining Volume and Value Increase: Despite the low relative value, 2024 saw a positive shift from the previous two years. Global M&A deal volume reversed its two-year decline, increasing by 7% year-to-date, while deal value was up by 15% year-to-date, on track to reach around $3.5 trillion.

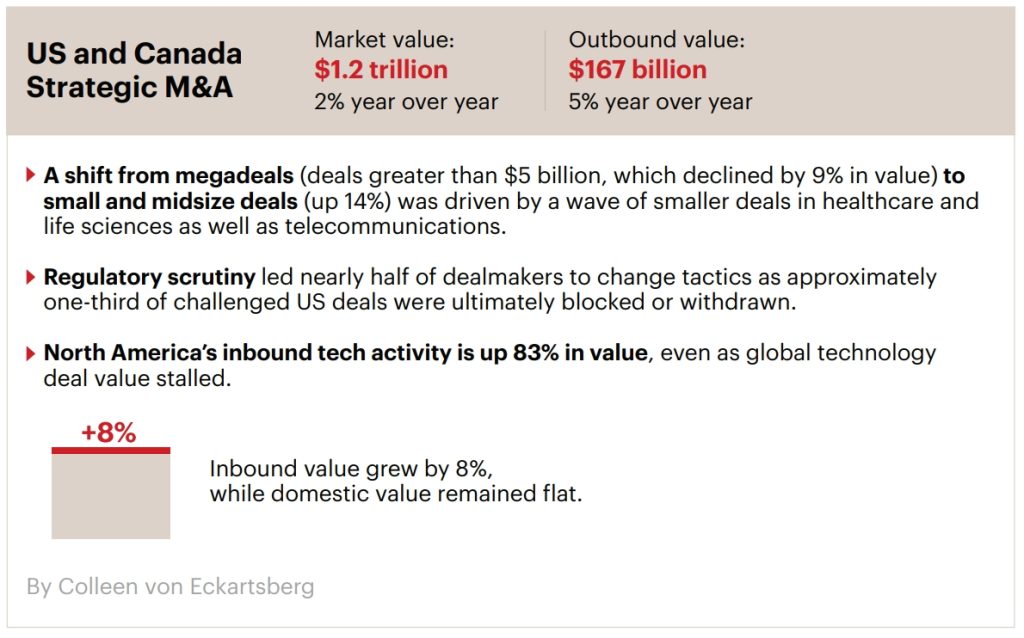

- Shift in Deal Size: There was a notable shift in the US and Canada market from megadeals (greater than $5 billion), which declined in value by 9%, to small and midsize deals, which were up 14%. This was driven by activity in healthcare and life sciences and telecommunications.

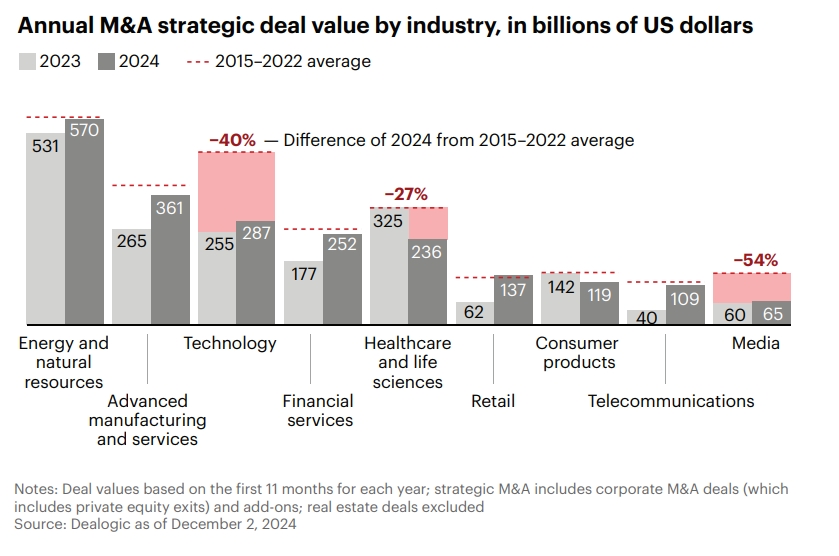

- Industries Under Pressure: Longtime M&A stalwarts like technology and healthcare and life sciences remained significantly below their activity levels during the lower interest rate era. This is attributed to their focus on scope deals for growth, which are impacted by the current market conditions.

2. Global M&A Market Outlook for 2025: Potential for a Rebound

- Optimism for the Year Ahead: Bain & Company expresses optimism for 2025, viewing M&A and divestitures as essential tools for navigating disruption and shifting profit pools.

- Building Pipeline of Supply: A significant pipeline of assets is being prepared for sale by both corporates and private equity firms, contingent on market recovery and rising valuations.

- Potential for Regulatory Tailwinds: Signs of hope for increased M&A activity are emerging from regulatory environments globally. New administrations in the EU and US are more open to M&A. Examples include:

- EU considering more openness to intraregional consolidation.

- US Trump administration likely adopting a more lenient antitrust posture, focusing on remedies and settlements over litigation.

- UK Competition and Market Authority favoring behavioral remedies and revising its merger assessment process.

- India clarifying merger guidelines and aiming to reduce approval timelines in 2024.

- The “New Game” of M&A: As the market regains footing, companies that can adapt to a new environment characterized by changed rules of the game will define success.

3. Adapting for Successful M&A in 2025:

- Pressure Testing M&A Strategy: Companies need to revisit and revise their M&A strategy, ensuring a clear link between overall strategy and the M&A roadmap. The feasibility of finding appropriate assets at the right price needs to be assessed.

- Affirming Geographic Footprint: Proactive evaluation of the appropriate response to plausible scenarios related to national industrial policy and tariffs is crucial. This involves determining:

- the ideal asset footprint,

- geographies to focus on or exit,

- and where direct control or alternative transactions (like joint ventures) are needed.

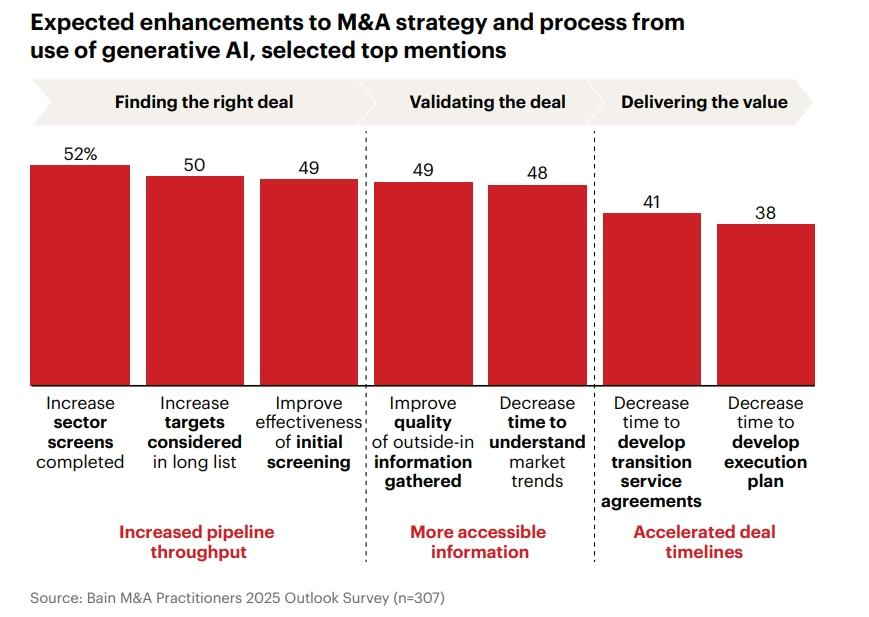

- Leveraging Generative AI: Generative AI is a significant tool for improving the M&A process, particularly in diligence and value realization.

- Quote: “early adopters relying on generative AI for deeper diligence will spend only about one day summarizing the data, instead of one week, so they will have more time to analyze how to extract maximum value from the deal.”

- Quote: “Companies relying on generative AI will be able to identify more detailed cost and revenue synergy opportunities as well as vastly improve their ability to write the draft plan to achieve them.”

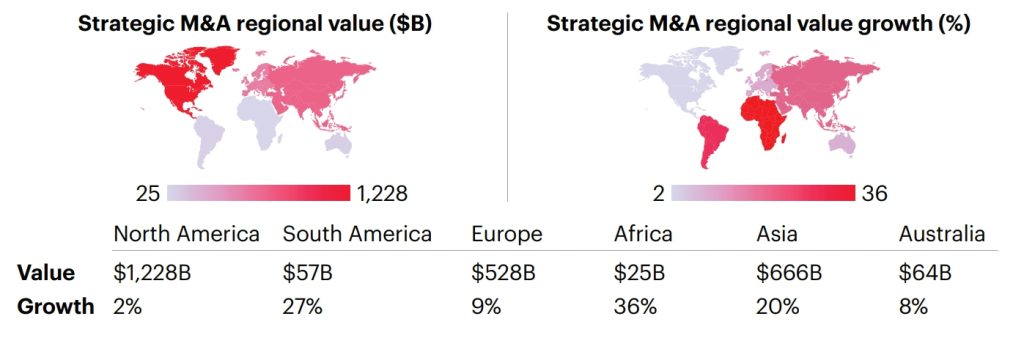

4. Regional M&A Market Highlights (2024):

US and Canada: Market value up 2%, driven by small and midsize deals. Regulatory scrutiny led to nearly half of dealmakers changing tactics, with approximately one-third of challenged deals blocked or withdrawn. Inbound tech activity increased significantly (83% in value).

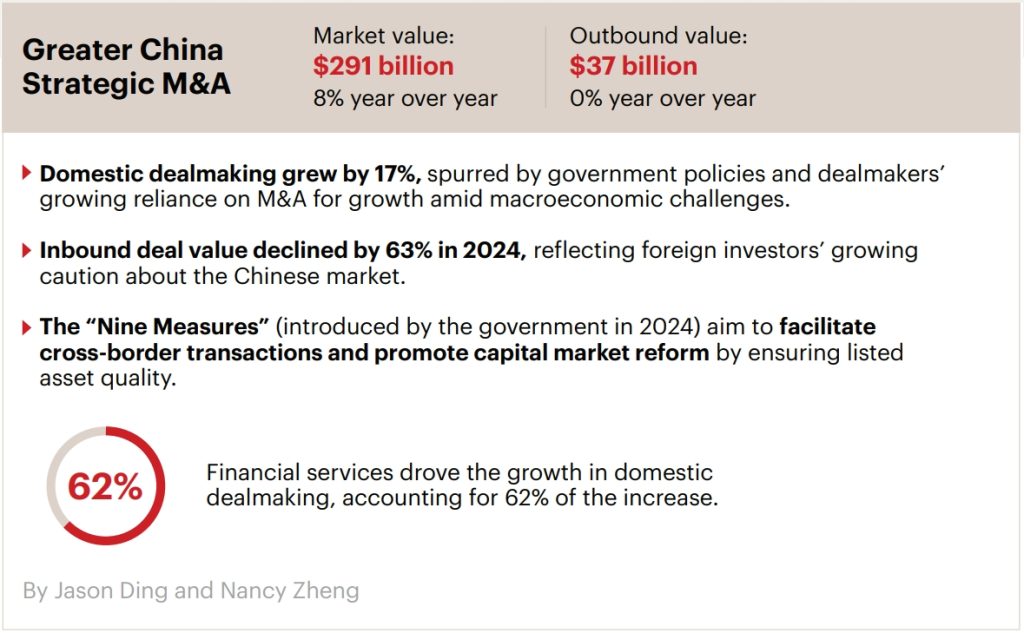

Greater China: Market value up 8%. Domestic dealmaking grew by 17%, fueled by government policies and reliance on M&A for growth. Inbound deal value declined sharply (-63%), reflecting foreign investor caution. Government policies like the “Nine Measures” are encouraging M&A.

Japan: Outbound value up 129%. Strong international appetite for Japanese assets is expected to continue. Government policies are encouraging M&A.

India: Market value down 16%. Domestic dealmaking powered activity, with scale deals in construction and building products and scope deals in pharmaceuticals, consumer products, and consumer tech. A maturing public market is fostering dealmaking.

Italy: Market value up 171%. Consolidation is expected in financial services. Nearly half of outbound deal value is in advanced manufacturing and services.

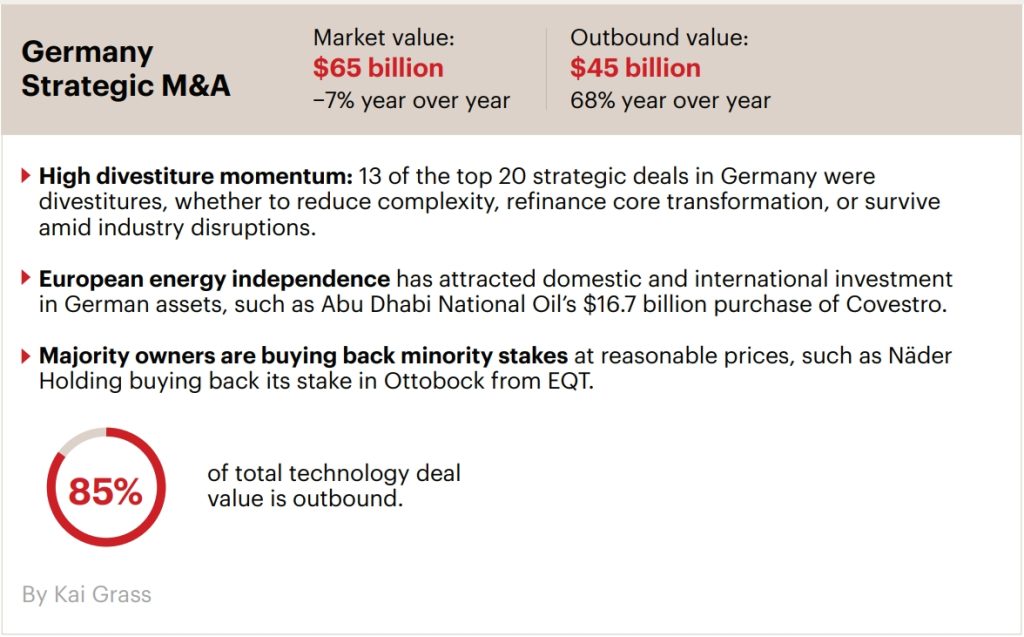

Germany: Market value down 7%. High divestiture momentum, with 13 of the top 20 strategic deals being divestitures. European energy independence is attracting investment.

France: Market value down 10%. Nearly half of strategic deal value is outbound and may increase as French acquirers seek international growth.

Brazil: Market value down 34%. Domestic companies are fueling the market. Energy deals represent half of the market’s strategic deal value, often focused on energy transition. International investors remain cautious.

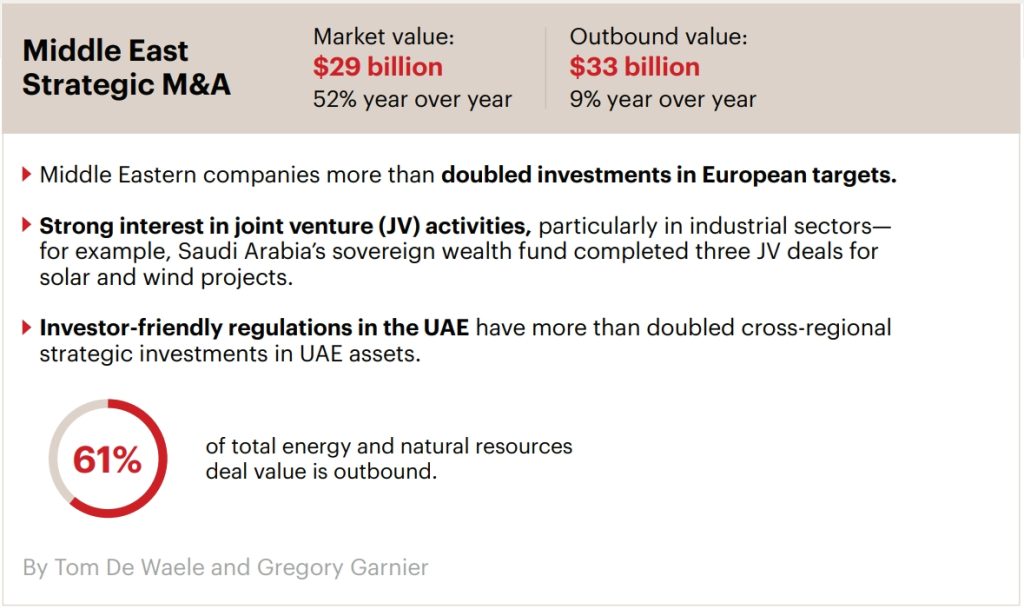

Middle East: Market value up 52%.

5. Industry-Specific M&A Insights:

Consumer Industries

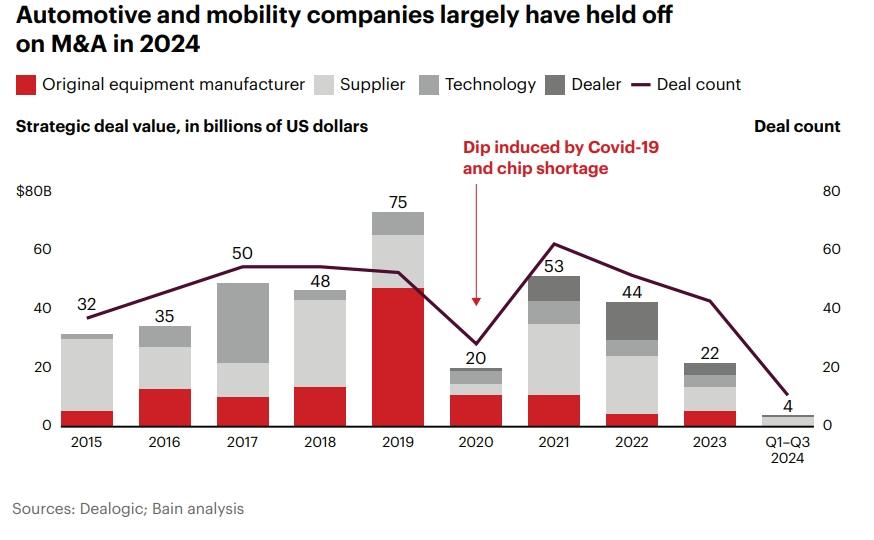

Automotive and Mobility: High uncertainty around EV ramp-up and the dual burden of investing in EVs while maintaining the internal combustion engine business are limiting M&A. More companies are exploring joint ventures and alliances as lower-investment alternatives.

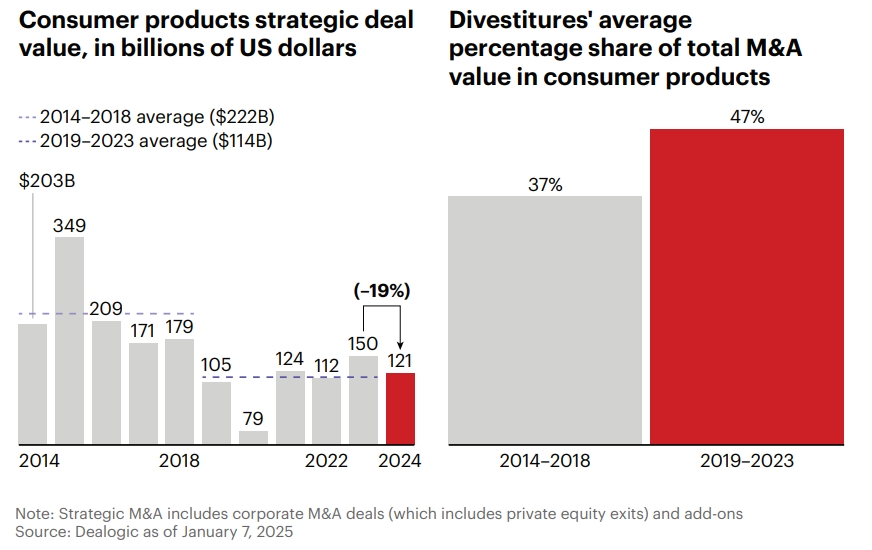

Consumer Products: Deal value dropped in 2024, but companies are increasingly using separations and divestitures (“carving out to grow”) to gain focus and simplify business models. 60% of surveyed executives expect to sell assets in the next three years. Key considerations for divestitures include stakeholder support and tax implications. For buyers of carve-outs, understanding the exact perimeter and addressing standing issues through cutting-edge diligence is crucial.

Quote: “Consumer products companies are separating to unleash growth by providing more focus and simpler business models.”

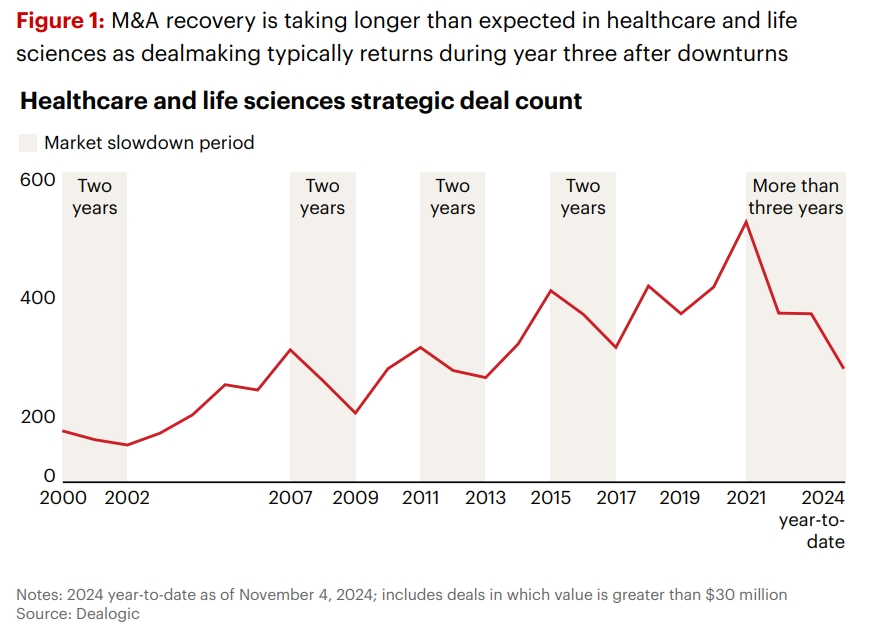

Healthcare and Life Sciences: Deal volume remained low in 2024, with value dropping by 28%. Historically active companies continued buying to double down on high-growth areas, and scope deals remain a focus. Companies making at least one deal a year showed significantly higher total shareholder returns than inactive acquirers. The emergence of GLP-1 treatments presents both opportunities and uncertainties for M&A. Building muscles for scope deals, using generative AI to accelerate the deal process, and adapting to evolving government regulations are critical.

Quote: “Historically active companies continued buying to double down on high-growth areas, and scope deals continue to be a focus for healthcare and life sciences.”

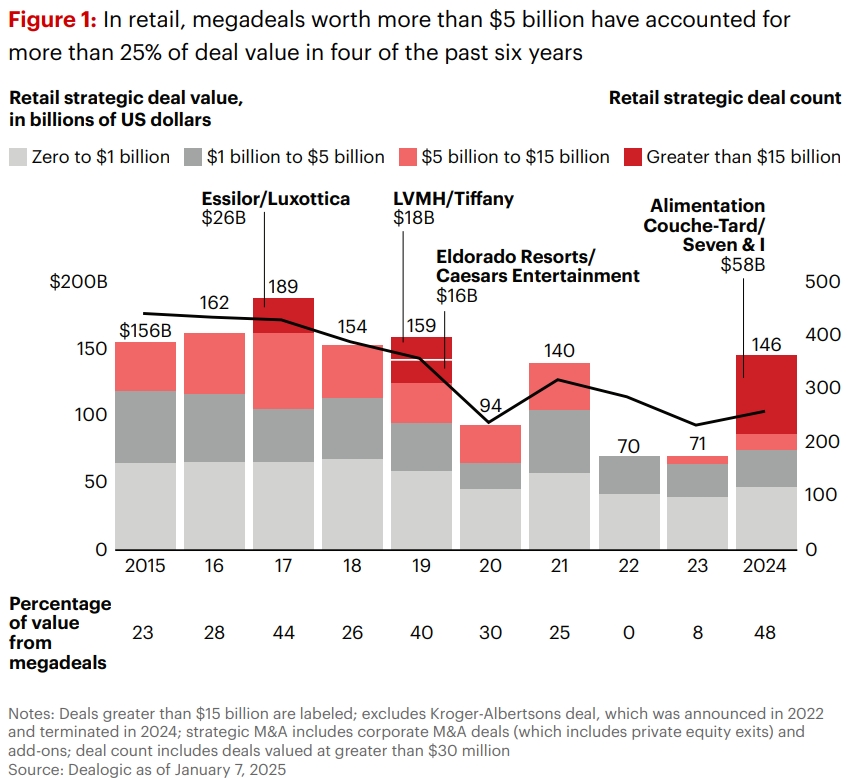

Retail: Retail M&A rebounded in 2024 after a two-year lull, with megadeals dominating headlines. Scale remains paramount. Midsize tuck-ins and scope deals are also being used to acquire capabilities and expand beyond traditional retail. Bain anticipates Cross-border and cross-sector deals. Retailers are increasingly using M&A and partnerships to build AI capabilities.

Infrastructure Industries

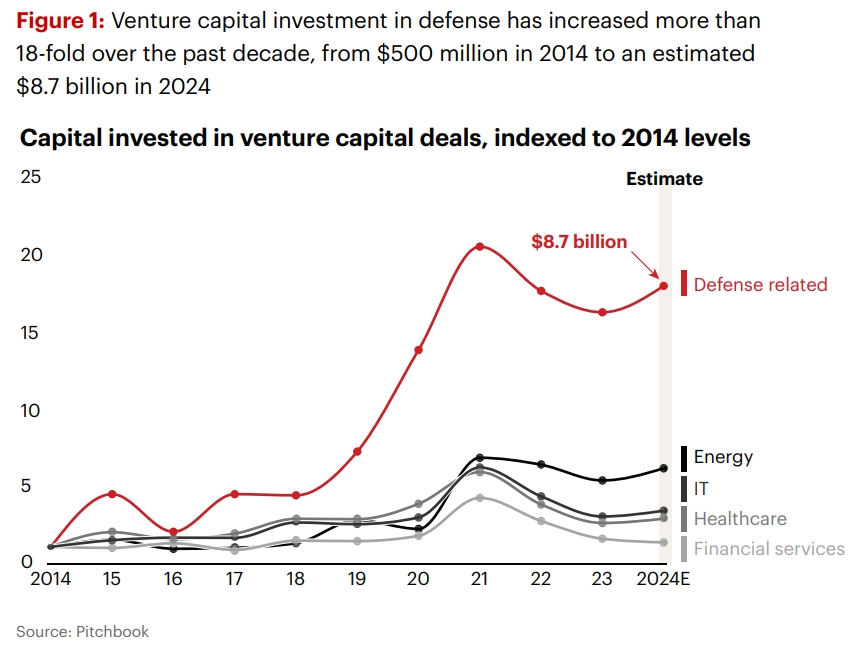

Aerospace & Defense: Surge in venture capital funding is enabling disrupters. Incumbents need to pursue acquisitions for capabilities and talent, ensuring integration doesn’t stifle innovation.

Quote: “A surge in venture capital funding is positioning new entrants to take share from legacy defense companies. Winning incumbents will pursue M&A in a variety of formats to gain the technical and operating model innovations necessary to stay competitive.”

Energy and Natural Resources: 2024 was a record year for deals in this sector (over $400 billion), driven by consolidation in oil and gas and portfolio reshaping in chemicals. The focus is on achieving deal value faster. Generative and traditional AI are being used for synergy estimates and identifying value levers. Pre-close integration planning and capabilities transfer (reverse synergies) are increasingly important. Defining a cultural thesis and mitigating cultural obstacles early are also emphasized.

Quote: “The energy sector engaged in more than $400 billion in deals, a three-year record.”

Quote: “Acquirers are increasingly using generative AI to enable more robust and more reliable deal synergy estimates.”

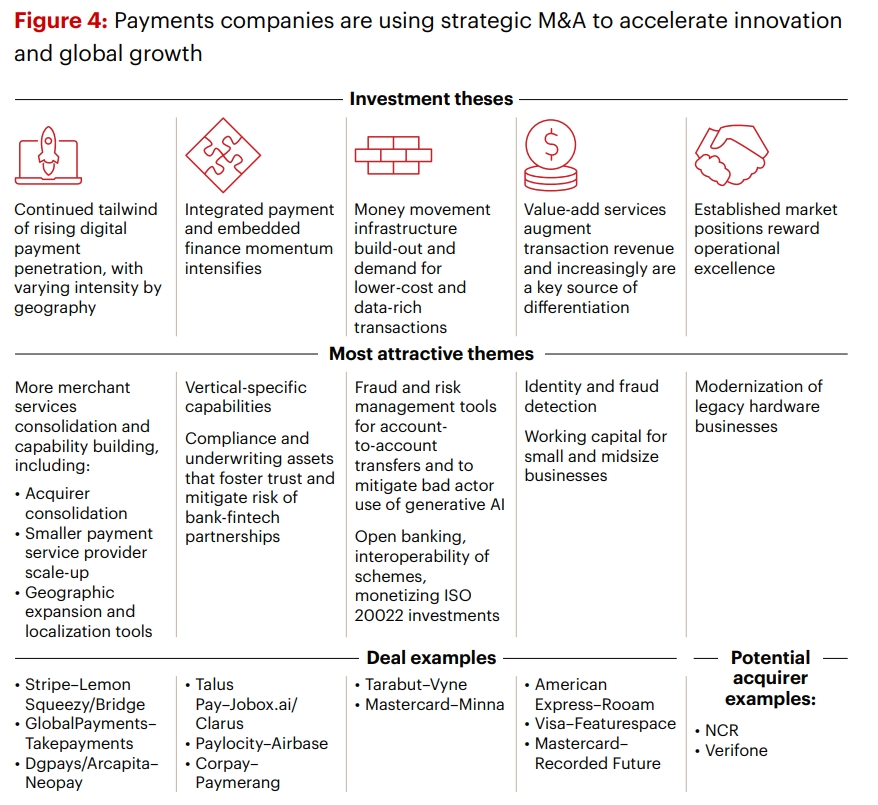

Financial Services: The sector is “coming back to life” in 2024, with an 11-month total deal value across financial services 72% higher than the same period in 2023, largely driven by cards and payments. Banking M&A rebounded, focused on scale transactions to share costs and boost profits. Insurers slowed down overall deal activity but used divestitures for portfolio reshaping. Payments incumbents are using M&A to ride the payments digitization wave, with deals focused on capability building, geographic expansion, and augmenting transaction revenue with value-add services. Bain advises proactive and preemptive approaches to M&A.

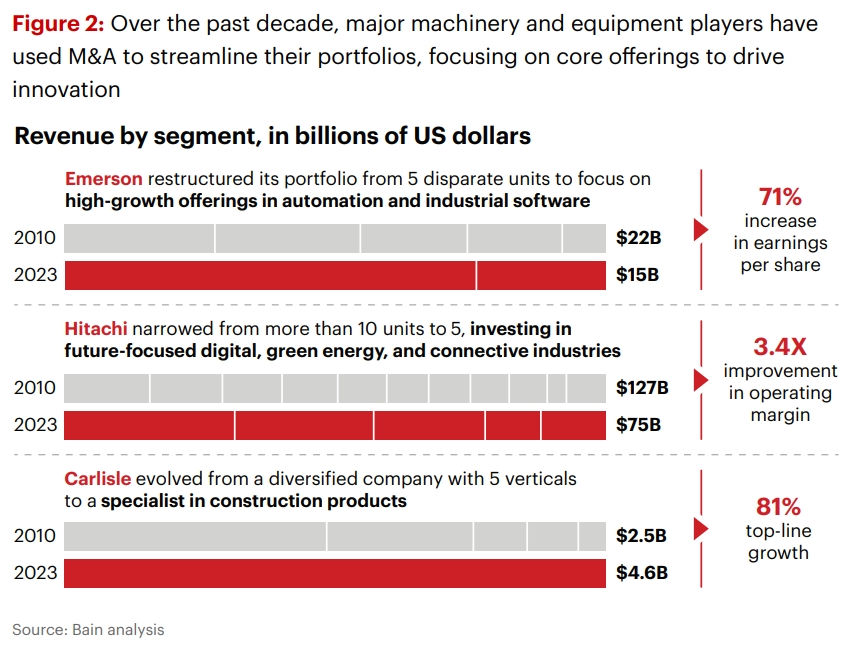

Machinery and Equipment: The industry is in need of consolidation. Successful companies are using M&A to transform, strengthen portfolios, and achieve sustainable leadership, not just immediate financial gains. Examples of successful transformations through M&A and divestitures include Emerson, Hitachi, and Carlisle. Rigorous portfolio reassessment and strategic coherence are key.

Technology and Media Industries

Building Products and Technology: Smart companies are using M&A to acquire new capabilities related to faster, more sustainable, and cost-effective construction and shifting profit pools. Five top capability imperatives are route to market, building automation, sustainability, industrialized construction, and technology. While scale deals continue, scope and capability deals focused on expansion are the big story for 2025 and beyond. Companies uses Generative AI for diligence and identifying value creation opportunities.

Quote: “In the building products industry, the smart companies are looking down the road and devising ways to use M&A to buy the new capabilities that will define the industry’s future.”

Quote: “While scale deals follow a logic of consolidation, scope and capability deals follow a logic of expansion.”

Media and Entertainment: Deals focus is on owning the consumer, owning the IP, or owning nothing. Convergence of platforms is a key driver, with cross-sector deals increasing. Quality IP that can thrive across platforms remains highly valuable, leading to more IP-based acquisitions. Cross-sector deals require different and more detailed diligence.

Quote: “Over the decades, content has remained king. Consumers might be fragmenting across platforms, but quality IP that can thrive in the proliferation of places to find it remains the constant in this world of converging platforms.”

Technology: Higher interest rates and changes in valuation approaches have altered the rules for tech scope deals. Acquirers now need to pursue meaningful cost synergies alongside revenue synergy theses, requiring a mindset shift towards improving productivity.

Telecom: Deal value rebounded in 2024 as some companies increased scale and others divested assets. Companies are turning to M&A to add new capabilities and evolve for the future. The industry is seeing a shift towards more disaggregated, narrowly focused business models.

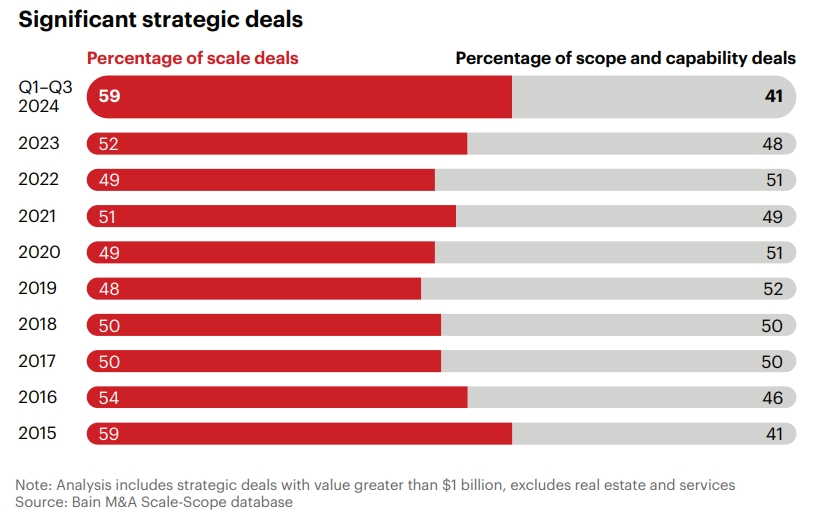

6. Defining Scale vs. Scope Deals:

- Scale Deals: Focus on consolidation to become stronger together. Aims to improve cost position, drive near-term earnings growth, and generate cash flows.

- Scope Deals: Focus on expansion.

- Buy the growth: Improve top-line growth by entering or expanding into faster-growing segments or acquiring faster-growing businesses.

- Buy the capability: Bring new capabilities for product or service innovation (especially digital) to strengthen competitive advantage or redefine the business through cross-sector deals.

Conclusion:

The Bain & Company Global M&A Report 2025 indicates a cautious but potentially rebounding M&A market. While 2024 saw adaptation to lingering headwinds, the outlook for 2025 is more optimistic, driven by anticipated regulatory shifts and the necessity for companies to use M&A to navigate technological and economic changes. Successful dealmakers will be those who proactively align M&A strategy with overall corporate strategy, strategically assess their geographic presence, and effectively leverage emerging technologies like generative AI for enhanced deal execution and value creation. The report also provides valuable industry-specific insights, highlighting tailored approaches to M&A based on sector dynamics and challenges.

Download full report here.

At NeoForm, we help businesses navigate these shifts with agile strategies and AI-powered insights. Ready to leverage M&A for growth? Let’s connect!

Glossary of Key Terms

Add-ons: Acquisitions made by a private equity firm that are added to an existing portfolio company.

Antitrust Posture: The stance taken by government regulators regarding the enforcement of laws designed to prevent monopolies and promote competition in the market.

Carve-out: The separation of a business unit or division from a larger parent company, often with the intention of selling it as a standalone entity.

Consolidation: The process by which smaller companies are absorbed into larger ones, leading to fewer, larger entities in an industry.

Diligence: The process of investigating a potential acquisition target to assess its financial health, operations, legal standing, and other relevant factors.

Divestiture: The sale or disposal of an asset, business unit, or division by a company.

Domestic Dealmaking: Merger and acquisition activity where both the acquiring and target companies originate within the same country or market.

Functional Entanglement: The complexity and difficulty in separating shared functions, systems, or operations when divesting a part of a business.

Inbound Deal Value: The total value of mergers and acquisitions in which a company originating outside a specific market acquires a local company within that market.

Integration: The process of combining the operations, systems, and cultures of two or more companies after a merger or acquisition.

Joint Venture (JV): A business arrangement in which two or more parties agree to pool their resources for the purpose of accomplishing a specific task.

Liquidity: The ease with which an asset can be converted into cash without affecting its market price.

M&A: Mergers and Acquisitions, the consolidation of companies or assets.

Megadeals: Mergers and acquisitions with a value typically exceeding a certain threshold, often in the billions of dollars.

Noncore Assets: Business units or assets that are not considered central to a company’s main business strategy.

Outbound Deal Value: The total value of mergers and acquisitions in which a local company within a specific market acquires a company originating outside that market.

Parenting Advantage: The benefits that a parent company can bring to its acquired or subsidiary businesses, such as access to capital, expertise, or networks.

Perimeter (of a deal): The defined scope of a carve-out acquisition, including the specific assets, liabilities, employees, and contracts being transferred.

Profit Pools: The total profits earned at different points along an industry’s value chain.

Pro Forma P&L: A projected profit and loss statement that shows the financial results of a company or business unit under a hypothetical scenario, such as after a divestiture or acquisition.

Regulatory Scrutiny: The examination and review of business activities, such as mergers and acquisitions, by government agencies to ensure compliance with laws and regulations.

Rollups: A strategy where a company acquires multiple smaller companies in the same industry to consolidate them into a larger entity.

Scope Deals: Mergers and acquisitions that expand a company’s business into adjacent geographies, product categories, or capabilities.

Scale Deals: Mergers and acquisitions focused on consolidating within a company’s existing market or industry to achieve greater size and efficiency.

Special Purpose Acquisition Companies (SPACs): Shell companies created to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.

Stranded Costs: Costs that remain with a company after a divestiture, related to assets or functions that previously supported the divested business.

Total Shareholder Return (TSR): A measure of the total return to shareholders, including stock price appreciation and dividends.

Transaction Structure: The legal and financial framework of a merger or acquisition deal.

TSAs (Transition Service Agreements): Agreements between a buyer and seller in a carve-out deal where the seller provides certain services (e.g., IT, HR) to the divested business for a limited period after the transaction closes.

Tuck-ins: Smaller acquisitions that are integrated into an existing business unit.

Underwrite (a deal): To assess the potential risks and returns of a merger or acquisition to determine its financial viability.

Vertical Integration: The combination in one company of two or more stages of production normally operated by separate companies.

Working Capital: The difference between a company’s current assets and its current liabilities, a measure of its short-term financial health.Bottom of Form

9 Comments

McKinsey Global Private Markets Report 2025 - NeoForm Business Partners

[…] Carve-Out Readiness: Prep non-core units for separate sales […]

Value Transformation in Private Equity - NeoForm Business Partners

[…] Global M&A Trends 2025: Key Insights from Bain Report […]

Mid-year M&A Report 2025 by Bain: How to Find Opportunity in Chaos | NeoForm - NeoForm Business Partners

[…] Global M&A Trends 2025: Key Insights from Bain Report […]

How Private Equity Funds Can Use M&A to Create Outsize Returns - NeoForm Business Partners

[…] Global M&A Trends 2025: Key Insights from Bain Report […]

McKinsey Technology Trends 2025: What Is Crucial to Align Your Business - NeoForm Business Partners

[…] Global M&A Trends 2025: Key Insights from Bain Report […]

Letting Go to Grow: Divestitures as Growth Strategy - NeoForm Business Partners

[…] Global M&A Trends 2025: Key Insights from Bain Report […]

The Great Trade Rearrangement: McKinsey Insights for Global Supply Chain - NeoForm Business Partners

[…] Global M&A Trends 2025: Key Insights from Bain Report […]

M&A Market in 2025: Is a Rebound on the Horizon? Insights from BCG Report - NeoForm Business Partners

[…] Global M&A Trends 2025: Key Insights from Bain Report […]

Global M&A Trends 2025: BCG Insights for Navigating Uncertainty - NeoForm Business Partners

[…] Global M&A Trends 2025: Key Insights from Bain Report […]

Comments are closed.