“Global Private Markets Report 2025: Private Equity Emerging from the Fog” by McKinsey & Company, provides a comprehensive analysis of private markets in recent years and the vision ahead, focusing on the private equity (PE) and venture capital (VC) markets.

You can read and download the full report on McKinsey website or NeoForm’s LinkedIn page.

Below is a detailed summary of the key points:

Key Trends in Private Equity (PE):

Rebound in Dealmaking and Distributions:

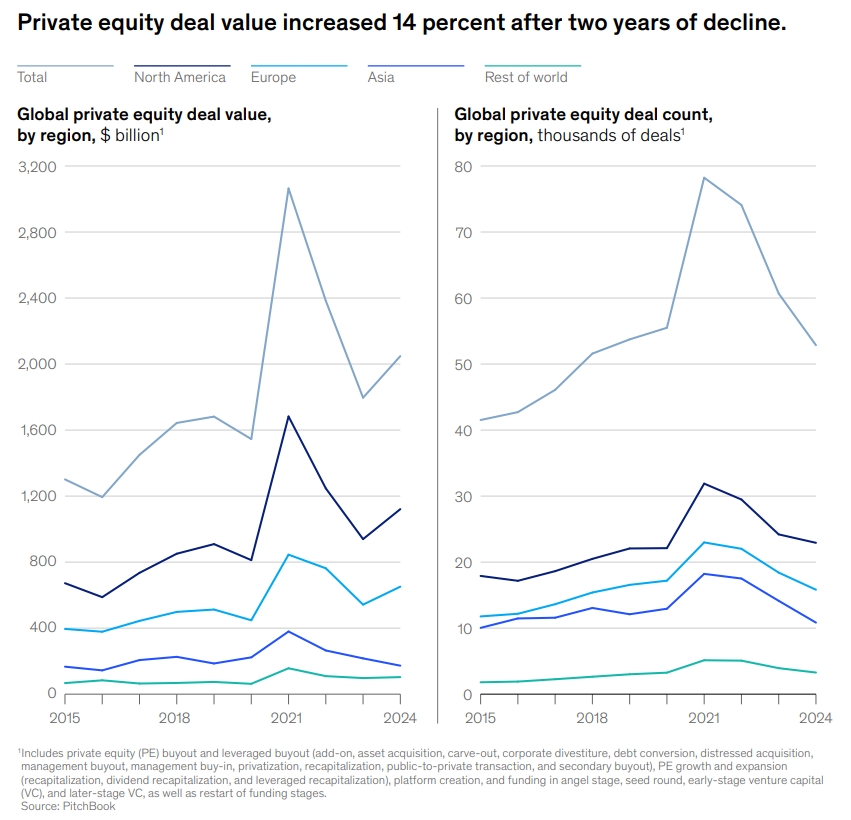

- After two years of decline, PE dealmaking rebounded in 2024, with a 14% increase in deal value, reaching $2 trillion. This was driven by a more favorable financing environment, with the cost of financing buyouts declining and loan values for PE-backed borrowers almost doubling.

- Distributions to limited partners (LPs) exceeded capital contributions for the first time since 2015, signaling a return of liquidity to LPs.

Large Buyouts and Sector Preferences:

- Large buyout transactions (above $500 million) saw significant growth, especially in North America and Europe, reflecting increased confidence among sponsors.

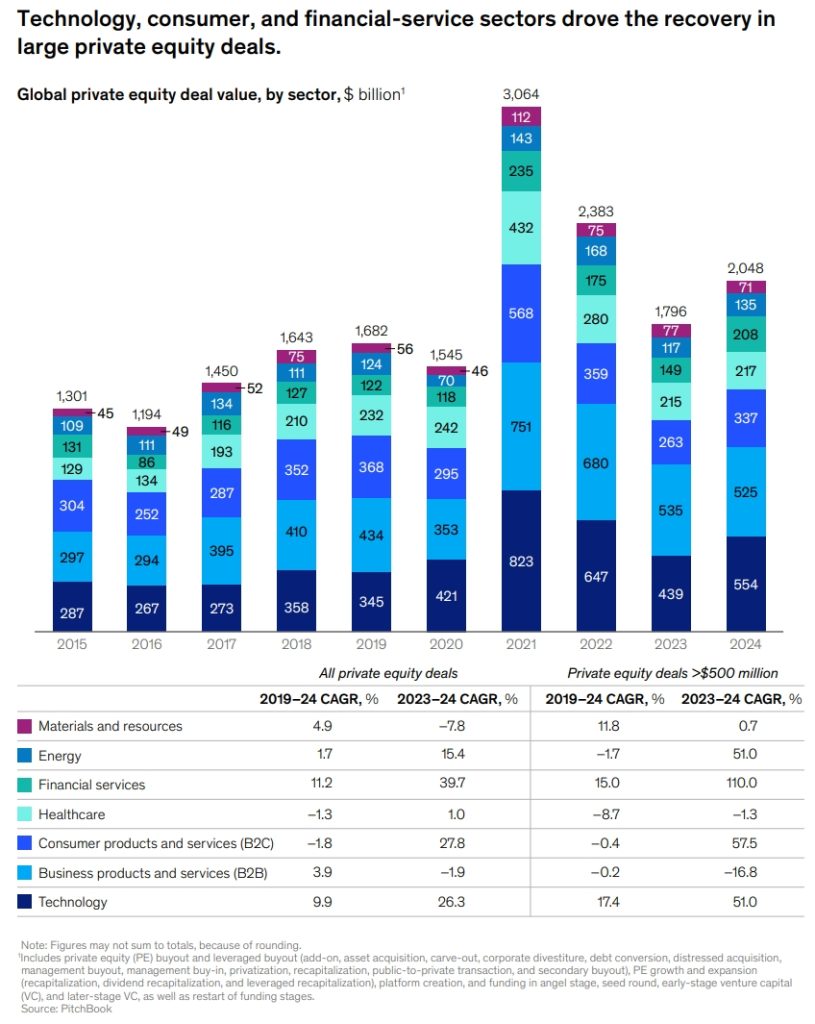

- Technology, consumer, and financial services sectors drove the recovery in large PE deals, while healthcare continued to underperform post-COVID-19.

Public-to-Private (P2P) Transactions:

- P2P transactions, particularly in Europe, gained traction as sponsors sought to take undervalued public companies private. These deals accounted for 11% of global PE deal value in 2024, up from 9% in 2023.

Exit Activity and Holding Periods:

- PE-backed exit value increased by 7.6% in 2024, but the backlog of assets awaiting exit grew, with average holding periods extending to 6.7 years, above the long-term average of 5.7 years.

- Sponsor-to-sponsor exits increased, but IPOs remained challenging, with PE-backed IPOs declining by 7% in value and 20% in count.

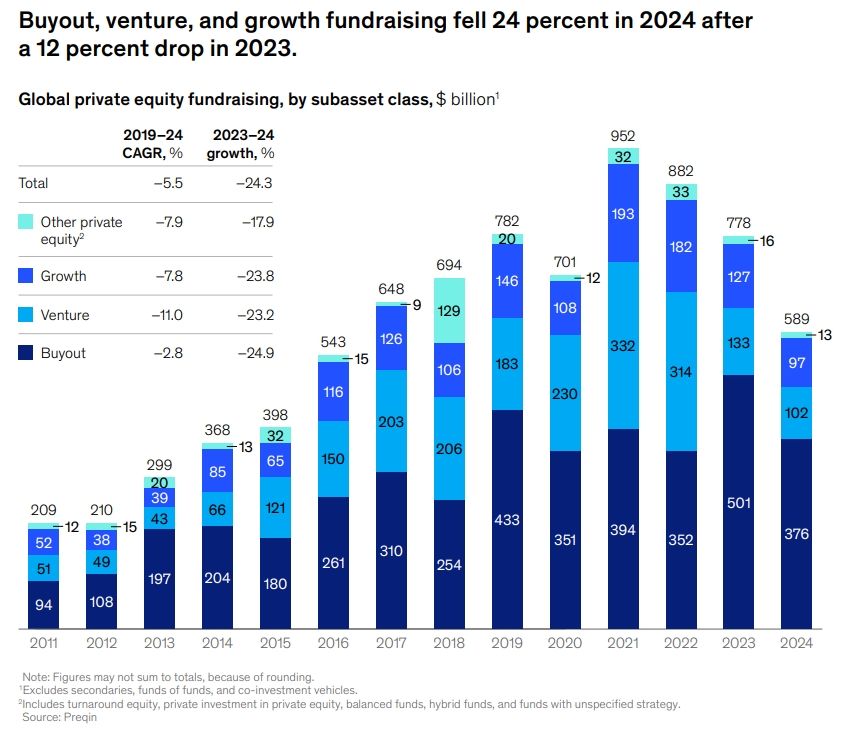

Fundraising Challenges:

- Fundraising declined for the third consecutive year, dropping by 24% in 2024. Midmarket funds (1billion to 5 billion) were more resilient, while larger funds faced difficulties.

- LPs are increasing their target allocations to PE (from 6.3% in 2020 to 8.3% in 2024), but fundraising is becoming harder due to lumpy distributions and increased competition for LP commitments.

Value Creation and Operational Focus:

- With rising entry multiples and longer holding periods, PE operators are increasingly focusing on value creation through revenue growth and EBITDA margin expansion, rather than relying on multiple expansion and leverage.

- Add-on M&A (acquisitions by PE-backed companies) accounted for 40% of total PE deal value in 2024, highlighting its importance in driving returns.

Key Trends in Venture Capital (VC)

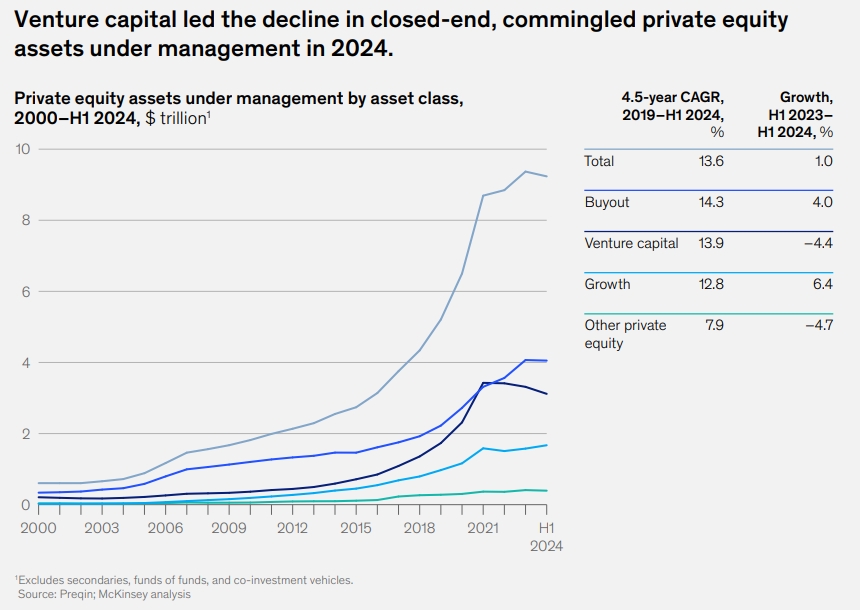

Continued Decline in Fundraising and Deal Activity:

- VC fundraising declined by 58% in 2023 and continued to struggle in 2024, with deal activity remaining far more challenged than in buyouts. Deal value in VC grew by only 6.7% in 2024, compared to 15.5% in buyouts.

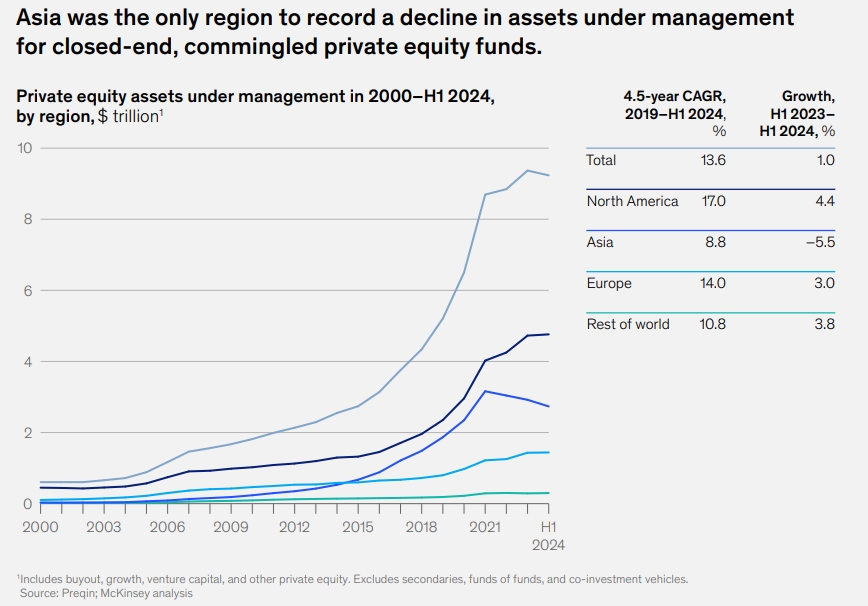

- Asia, which comprises more than half of VC’s total assets under management (AUM), saw a significant decline in fundraising and performance, contributing to the overall slowdown in VC.

Performance and IRR:

- VC performance improved marginally in 2024, with an IRR of 1.9% through September 30, 2024, compared to a negative IRR of 2.5% in the previous 12 months. However, this still lagged behind buyouts, which had an IRR of 4.5%.

Challenges in the Start-up Environment:

- The VC sector continues to face challenges due to a difficult start-up environment globally, with declining deal counts and slower growth in deal value. The decline in Asia, particularly China, has been a significant factor.

Global Trends and Forecasts

Resilience and Innovation in PE:

- Despite challenges, the PE industry is emerging more resilient and innovative. GPs are unlocking alternative sources of capital, such as separately managed accounts, co-investments, and partnerships, and are increasingly targeting high-net-worth individuals through more accessible fund structures.

Liquidity Solutions and Secondary Markets:

- The secondary market has become a critical source of liquidity for LPs, with secondaries transaction value rising 45% to an all-time high of $162 billion in 2024. LP-led deals and GP-led secondaries, including continuation vehicles, have gained prominence.

Long-Term Performance and LP Conviction:

- Over the long term, PE has outperformed public markets, particularly the S&P 500, which has reinforced LPs’ conviction in the asset class. Buyout multiples have remained lower than public multiples, reflecting the illiquidity premium of private markets.

Geopolitical and Macroeconomic Challenges:

- The industry must navigate increasing geopolitical uncertainty, higher interest rates, and the lingering effects of the 2021–22 dealmaking boom. Refinancing portfolio companies in a higher-rate environment remains a key challenge.

Conclusion:

The private equity industry is emerging from a period of uncertainty with renewed confidence, driven by a rebound in dealmaking, increased distributions, and a focus on value creation. While challenges remain, particularly in fundraising and exits, the industry is adapting through innovation and resilience. Venture capital, however, continues to face headwinds, with declining fundraising and deal activity, especially in Asia. As the fog clears, the private markets are poised for a more stable and growth-oriented future, with PE leading the way.

5 Comments

The Future of Investing: Private Markets and Credit Opportunities in 2025 – Neoform Business Partners

[…] Private Credit: The “Golden Age” of […]

McKinsey Global Private Markets Report 2025 - NeoForm Business Partners

[…] 1. Private Equity: Emerging from the Fog […]

Healthcare Private Equity Trends in 2025 from Bain Report - NeoForm Business Partners

[…] Global Private Markets Report 2025: Private Equity Emerging from the Fog […]

Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment - NeoForm Business Partners

[…] Global Private Markets Report 2025: Private Equity Emerging from the Fog […]

Global Wealth Management Report 2025: Rethinking the Playbook - NeoForm Business Partners

[…] Global Private Markets Report 2025: Private Equity Emerging from the Fog […]

Comments are closed.