The private equity (PE) landscape in 2025 is marked by cautious optimism, creative liquidity solutions, and intensified competition. Bain & Company’s Global Private Equity Report 2025 highlights key trends shaping the industry, from rebounding dealmaking to the growing influence of generative AI.

Here’s what you need to know.

1. A Partial Recovery Takes Shape

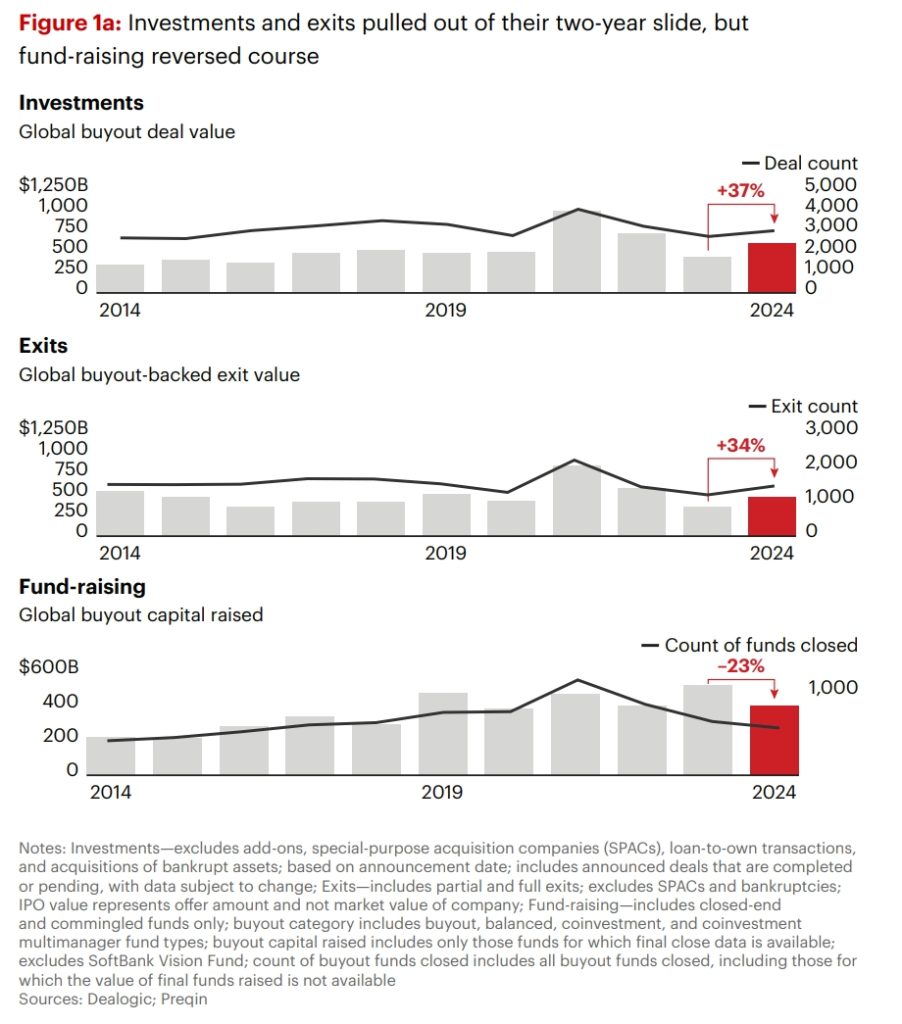

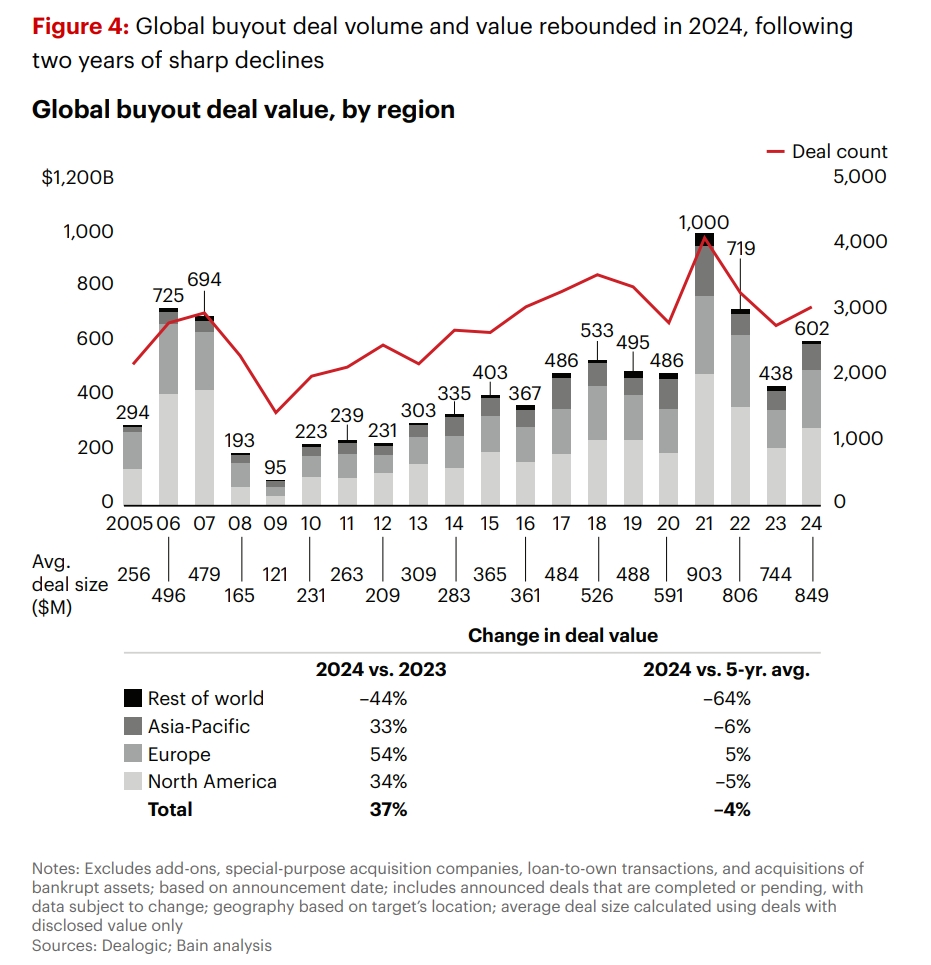

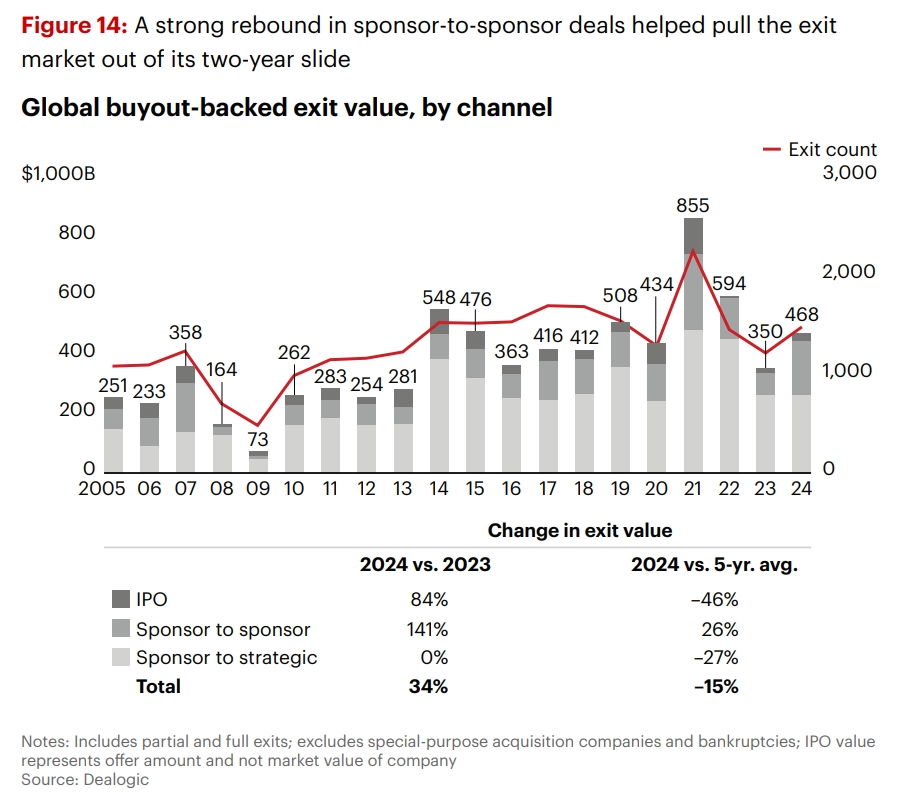

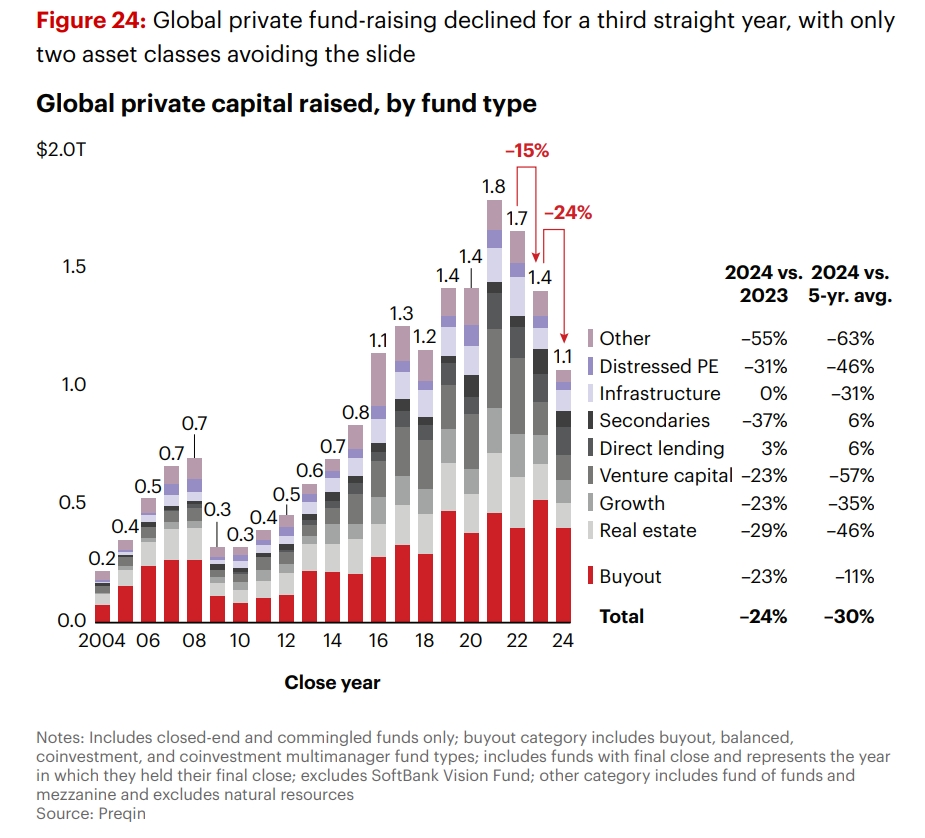

After two years of decline, PE dealmaking rebounded in 2024, with global buyout deal value rising 37% and exit value increasing 34%. However, fund-raising lagged, dropping 23%, as limited partners (LPs) grappled with prolonged asset holding periods and sluggish distributions.

Key Drivers:

- Macro Stability: Lower inflation and interest rates revived investor confidence.

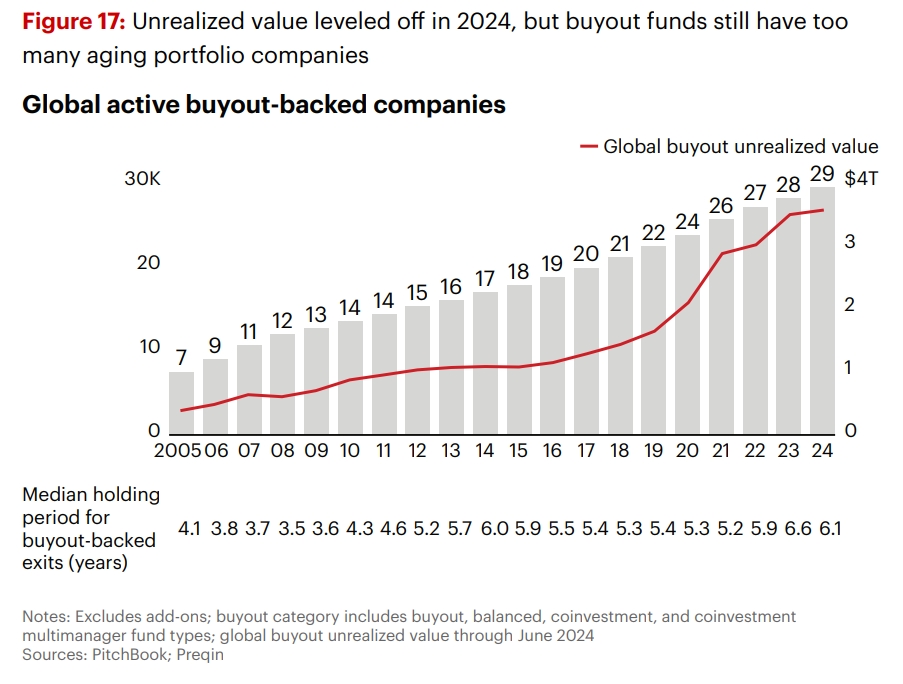

- Dry Powder Pressure: With $1.2 trillion in unspent capital, GPs are under pressure to deploy aging funds.

- Public-to-Private Surge: Large take-private deals, like Vista Equity Partners’ $8.4 billion acquisition of Smartsheet, dominated the high end of the market.

Yet, challenges persist. Fund-raising remains a “haves vs. have-nots” game, with top-quartile funds growing 53% larger in successor funds, while others struggle to meet targets.

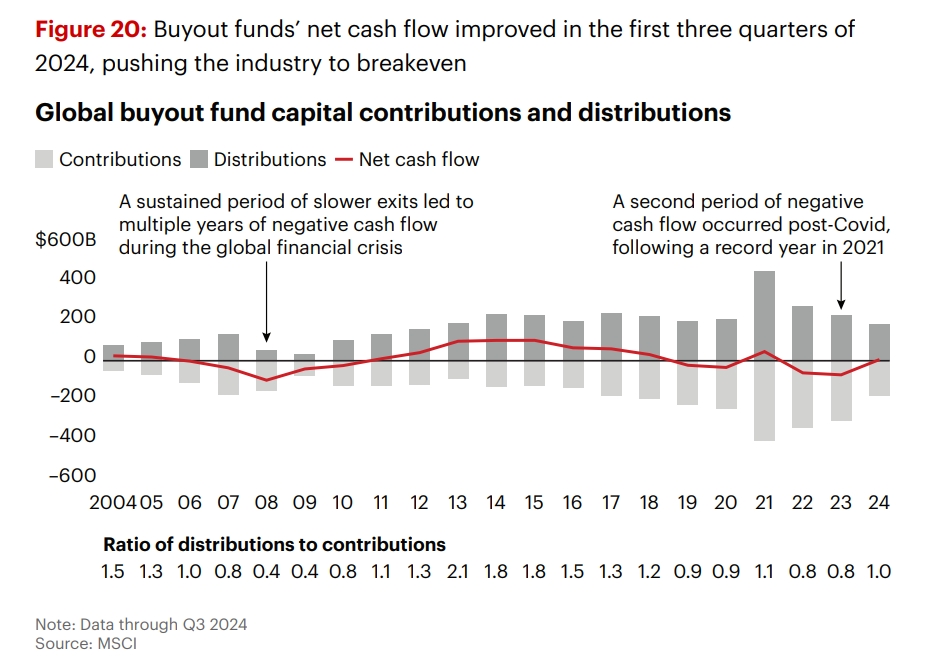

2. The Liquidity Crunch and Creative Solutions

Exits rebounded but failed to keep pace with the industry’s growth. Distributions as a percentage of net asset value (NAV) hit a decade-low of 11%, forcing GPs to explore alternative liquidity mechanisms:

- Minority Stakes: $71 billion in partial monetizations in 2024.

- Continuation Funds: Secondary funds raised $102 billion, enabling GPs to extend hold periods.

- NAV Loans: Expected to double to $300 billion by 2026.

The message is clear: Traditional exit channels are insufficient, and innovation is critical to returning capital to LPs.

3. Generative AI: The New Value-Creation Frontier

PE firms are racing to harness generative AI, with 20% of portfolio companies already operationalizing use cases. Leaders like Vista Equity Partners and Apollo Global Management are setting the pace:

- Vista mandates AI goals for all portfolio companies, driving productivity (e.g., 30% faster coding).

- Apollo’s Center of Excellence advises portfolio firms on AI adoption, yielding 40% cost reductions in content production.

Key Takeaway: AI is no longer optional—it’s a strategic imperative for operational efficiency and competitive edge.

4. Software Investing: The Margin Growth Challenge

Software deals have long relied on revenue growth and multiple expansion, but margin improvement has lagged. Bain’s analysis of 33 buyouts revealed:

- 94% projected margin growth, but actual delivery fell short.

- Top-quartile deals drove virtually all margin gains.

Solution: Integrated due diligence combining commercial, technical, and operational insights to underwrite profitable growth.

5. Carve-Outs: From Reliable Winners to High-Stakes Bets

Once a PE darling, carve-outs now deliver mixed results:

- Pre-2012: 3.0x MOIC (vs. 1.8x for other buyouts).

- Post-2012: 1.5x MOIC, barely matching broader market returns.

Winning Formula:

- Link separation plans to value-creation theses.

- Make tough decisions early (e.g., cost cuts, geographic rationalization).

- Install transformational leadership to drive change.

6. The Strategic Imperative: Scale, Fees, and Competition

Structural shifts are reshaping PE’s future:

- Fee Pressure: The “2 and 20” model is eroding, with net fees down ~50% since the global financial crisis.

- Retail and SWF Capital: Private wealth and sovereign wealth funds will drive 60% of AUM growth by 2033.

- Scale Matters: Larger firms dominate fund-raising and leverage capabilities (e.g., AI, data analytics).

- Strategic M&A: Deals like BlackRock’s $12.5 billion acquisition of Global Infrastructure Partners signal industry consolidation.

The Bottom Line: Differentiation is nonnegotiable. Firms must articulate a clear ambition—whether through scale, specialization, or innovation—to thrive.

Conclusion: Navigating the New PE Landscape

2025 is a year of measured recovery, but the rules of the game are changing. Success hinges on:

- Liquidity Creativity: Embrace secondaries, NAV loans, and minority stakes.

- AI Adoption: Embed generative AI into value-creation plans.

- Margin Focus: Prioritize profitability, not just growth, in software deals.

- Strategic Clarity: Define a differentiated path amid fee compression and competition.

For PE firms and investors alike, the message is clear: Adapt or risk falling behind.

NeoForm Business Partners helps private equity firms and portfolio companies navigate these shifts with tailored strategy and operational expertise. Contact us to learn more.

Source: Bain & Company, Global Private Equity Report 2025.

Download full report here or from NeoForm LinkedIn page.

9 Comments

The Future of Investing: Private Markets and Credit Opportunities in 2025 – Neoform Business Partners

[…] Private Equity: Better Valuations, Long-Term […]

Global M&A Trends 2025: Key Insights from Bain Report - NeoForm Business Partners

[…] Building Pipeline of Supply: A significant pipeline of assets is being prepared for sale by both corporates and private equity firms, contingent on market recovery and rising valuations. […]

Healthcare Private Equity Trends in 2025 from Bain Report - NeoForm Business Partners

[…] Private Equity Market Trends in 2025: A Year of Recovery and Strategic… […]

Mid-year M&A Report 2025 by Bain: How to Find Opportunity in Chaos | NeoForm - NeoForm Business Partners

[…] Private Equity Market Trends in 2025: A Year of Recovery and Strategic… […]

Asset-Based Finance: The $6+ Trillion Private Credit Opportunity You Can't Ignore - NeoForm Business Partners

[…] Private Equity Market Trends in 2025: A Year of Recovery and Strategic Shifts […]

McKinsey Technology Trends 2025: What Is Crucial to Align Your Business - NeoForm Business Partners

[…] Private Equity Market Trends in 2025: A Year of Recovery and Strategic… […]

Turning Sustainability into Growth: The Pragmatist's Playbook for Visionary CEOs by Bain - NeoForm Business Partners

[…] Private Equity Market Trends in 2025: A Year of Recovery and Strategic Shifts […]

How Private Markets Are Redefining Corporate & Investment Banking - BCG 2025 - NeoForm Business Partners

[…] Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment […]

Global Banking Review 2025: McKinsey Insights on Winning Strategies - NeoForm Business Partners

[…] Private Equity 2025: AI, India & Exit Momentum Reshape Global Investment […]

Comments are closed.